How Fund Companies Secure Spots on Asian Retail Distribution Platforms

Share

Share

Executive Summary

In an increasingly crowded marketplace, asset managers in Asia are constantly in search of creative ways to win the attention of fund distributors and secure placement on their platforms. For many fund providers, that challenge could become even more difficult if recent market volatility persists.

Methodology

Between March and June 2024, Coalition Greenwich conducted 165 interviews with some of the largest fund distributors in Asia. Senior gatekeepers were asked to provide detailed information on their business priorities, quantitative and qualitative evaluations of their investment managers, and qualitative assessments of those managers soliciting their business. Countries and regions where interviews were conducted in Asia include Hong Kong, Macau, Singapore, South Korea, Taiwan, Malaysia, and Thailand.

In an increasingly crowded marketplace, asset managers in Asia are constantly in search of creative ways to win the attention of fund distributors and secure placement on their platforms. For many fund providers, that challenge could become even more difficult if recent market volatility persists.

In times of volatility, gatekeepers for Asian distribution platforms tend to gravitate to large and well-known asset managers, awarding platform spots and support to fund companies with name brands and established track records that inspire confidence among investors. By way of example, it is exactly those traits of a powerful brand and proven history of delivering for clients that has helped Allianz Global Investors maintain its status as the Greenwich Quality Leader in Asian Intermediary Distribution across the ups and downs of the market cycle for the past five years, including 2024.

Standing Out in a Crowded Market

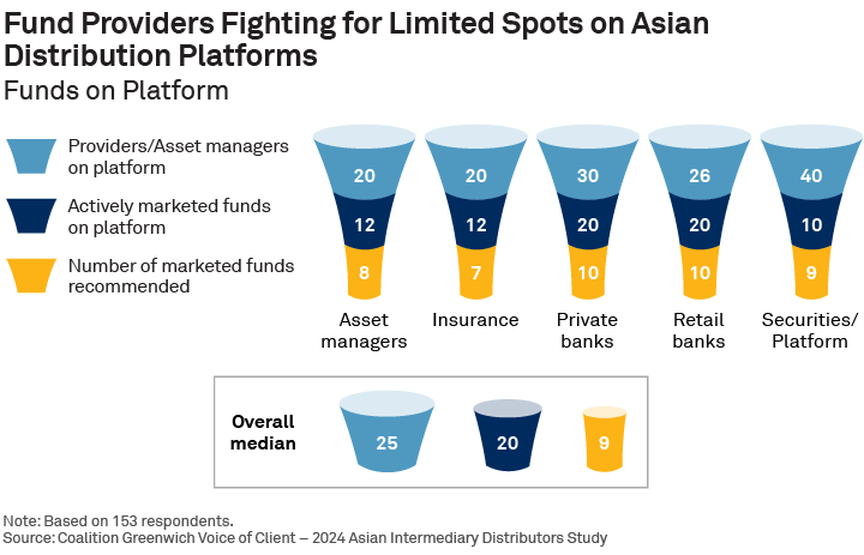

Maintaining a position at the top of this competitive marketplace is no small feat for any asset manager. Gatekeepers for Asian fund platforms are highly selective. The typical fund platform in Asia hosts products from only 25 fund providers, with that average fluctuating between 40 providers on the biggest securities platforms to just 20 on insurance and asset management platforms. Platforms are even more discerning when it comes to which funds they will proactively market. On average, platforms actively market only 20 funds and recommend only nine to their end investors from those marketed funds.

Brand helps fund providers stand out in this highly selective process. Across Asia, fund distributors routinely cite a strong brand as the No. 2 criterion driving the selection of funds for their platforms, behind only performance. For distributors, a strong brand means a fund provider has already proven its ability to deliver consistent, high-quality investment performance and service. That established reputation creates trust among distributors and end investors alike.

When markets are volatile, investors become less inclined to take on the added risk and due diligence burdens associated with investing in a less-familiar fund company. Knowing that, fund platforms also tend to favor fund providers with the strongest brands. After the August 5, 2024 market correction, we expect both fund platforms and retail investors in Asia to lean toward big, name-brand providers and funds—at least in the near term and until market volatility subsides somewhat.

Performance and Partnership Help Fund Providers Secure Placement

That’s not to say smaller firms and less well-known fund companies won’t be able to win platform spots and assets. To the contrary, investment performance is a great equalizer. It has a bigger impact on distributors’ fund selection than any other factor, including brand. So, providers who deliver attractive returns should have no trouble finding demand for their funds. Likewise, Coalition Greenwich data shows that fund providers can win over platform gatekeepers by demonstrating superior investment capabilities, a good fit between their products and the needs of both the distributor and platform investors, a well-defined investment process and philosophy, and/or competitive fees.

Fund providers of all sizes and brand strengths also have a growing opportunity to secure spots on fund platforms by proving themselves to be good partners to distributors. Distributors are looking to fund companies for market, product and performance information that:

- Helps the distributor assess and understand the performance of the individual fund,

- Helps the distributor understand and gain insight into the asset class and financial markets more broadly, and

- Can be shared with investors to help inform them about products and markets.

Over the past 12 months, the share of fund distributors citing this type of “information transparency” as a key factor in their selection of fund providers increased by six percentage points.

Reaching the Gatekeepers: Sales and Marketing Strategies for Fund Companies

Once a fund provider understands what it takes to make it onto a fund platform, the next question is how to capture the attention of platform gatekeepers and deliver your message. Although the internet and social media are revolutionizing the investment industry, our data suggest that, for now, an old-fashioned strategy works best. When asked how they learn about new managers and products, more than half of fund distributors cite industry events, making these IRL (in-real-life) gatherings the No. 1 source of information. As such, participation in both distributors’ in-house events and third-party events should be a central pillar of every fund company’s sales and market strategy.

Of course, given the efficiencies associated with online communications, fund companies should supplement their event schedules with a robust digital marketing and outreach campaign. Nearly 44% of fund distributors say they learn about new managers and products from webinars, up from just 39% last year. Likewise, the share citing social media as a source of information jumped to 33% from 28%. That’s in addition to the sizable shares of distributors who gather information about funds and fund providers through web searches and by perusing manager websites.

When developing sales and marketing strategies, it’s critical for fund companies to take into account regional variation across the vast and diverse Asian market. For example, not a single South Korean fund distributor said they get information on managers and products from industry events, and only 31% use webinars. Instead, half use web searches to research potential managers and products, and half rely on word of mouth and information from peers to inform their decision-making.

The Shrinking Role of ESG

ESG remains an important factor in the competition for placement on Asian fund platforms—but less important than it once was. Approximately 53% of fund distributors in Asia require fund providers to have a clearly articulated ESG policy and ESG-compliant products to be considered for their platforms. That share is about unchanged from last year but is down significantly from the high of 63% in 2022. Why has ESG lost traction? Fund distributors cite performance concerns and a lack of demand from end investors.

Asian Fund Platforms Project Strong Demand from Retail Investors

Asian fund providers and distributors have been enjoying the tailwinds of strong investor demand. When Coalition Greenwich interviewed fund distributors in the first half of this year, we found robust and increasing demand for a broad range of fund products and strategies.

Approximately three-quarters of fund distributors said they expect to see increased inflows from their retail investors into international/global equities and U.S. equities in the next 12 months.

Over the past year, with global equity market performance driven by the technology sector, investors on retail fund platforms poured assets into growth strategies and thematic strategies that provide exposure to specific performance drivers like artificial intelligence. Like investment companies around the world, fund distributors in Asia will be keeping a close eye not only on market direction, but also on concentration levels in global equity markets and the performance of the handful of tech firms that have driven returns in both U.S. equity markets and growth strategies more broadly.

Meanwhile, higher base rates in 2023 propelled yields to levels that made fixed income highly attractive to Asian retail investors. Fully 70% of fund distributors expect to see increased inflows into investment-grade bonds in the next year, and 55% expect increased flows into high-grade government bonds.

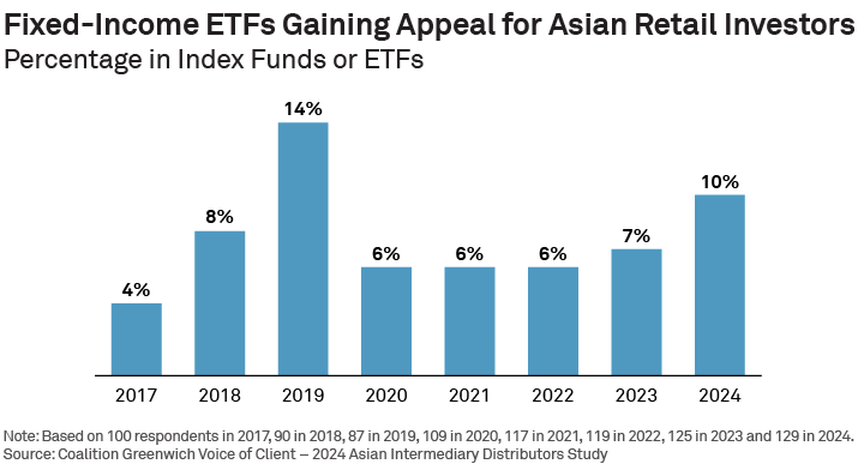

The appeal of bond yields in an environment of elevated rates appears to have helped fuel demand for fixed-income ETFs. As shown in in the chart below, only 7% of fixed-income assets on Asian fund platforms were invested in ETFs in 2023. In 2024, that share climbed to 10%, an increase likely attributable at least in part to demand from fee-conscious bond investors looking to minimize costs and maximize income.

Nearly half of Asian fund distributors expect to see significant positive inflows into multi-asset funds in the next year. Investors view these funds as a means to access regular income while balancing exposure to equities, fixed-income and other asset classes in a period of uncertainty about the direction of global markets and economies.

Gatekeepers on Asian fund platforms are also bullish on private assets. About 38% of study respondents expect to see strong positive inflows into private debt, and about a third expect significant inflows into private equity. (Roughly 1 in 5 platforms expect to see outflows in private debt, and about 15% expect outflows in private equity). Those expectations have been remarkably consistent through the three years Coalition Greenwich has been tracking this asset class.

Looking ahead, gatekeepers see the addition of new private debt managers as the biggest change to their platform rosters. Together, those trends strongly suggest that the shift of investor assets into private markets represents a long-term change in allocations, rather than any cyclical rotation.

Head of Asia-Pacific Parijat Banerjee, Ken Yap and Arifur Rahman advise investment management clients in Asia.

Methodology

Between March and June 2024, Coalition Greenwich conducted 165 interviews with some of the largest fund distributors in Asia. Senior gatekeepers were asked to provide detailed information on their business priorities, quantitative and qualitative evaluations of their investment managers, and qualitative assessments of those managers soliciting their business. Countries and regions where interviews were conducted in Asia include Hong Kong, Macau, Singapore, South Korea, Taiwan, Malaysia, and Thailand.