Japanese institutions: Slowing pace of manager hiring, shift into private markets

Share

Share

Executive Summary

Japanese institutional investors are dramatically cutting back on new asset manager hires and slowing the pace of their ongoing shift toward private assets in their portfolios.

Methodology

From April through October 2024, Crisil Coalition Greenwich conducted interviews with 254 of the largest corporate pension funds, public pension funds, financial institutions, and endowments and foundations in Japan. Total fund assets were ¥949 trillion. Senior fund professionals were asked to provide quantitative and qualitative evaluations of their investment managers, qualitative assessments of those managers soliciting their business, and detailed information on important market trends.

Japanese institutional investors are dramatically cutting back on new asset manager hires and slowing the pace of their ongoing shift toward private assets in their portfolios.

In last year’s report, we noted that traditional asset managers in Japan could be facing an increasingly challenging marketplace as asset owners slow expectations for manager hiring. In 2022, a volatile year for global financial markets, roughly half of Japanese institutional investors said they would be in the market for new asset managers in the coming year. In 2023, that share moderated, falling to 40%.

That slowdown continued in 2024 with only 28% of Japanese financial institutions and pensions funds indicating that they would be hiring a new asset manager in the next 12 months.

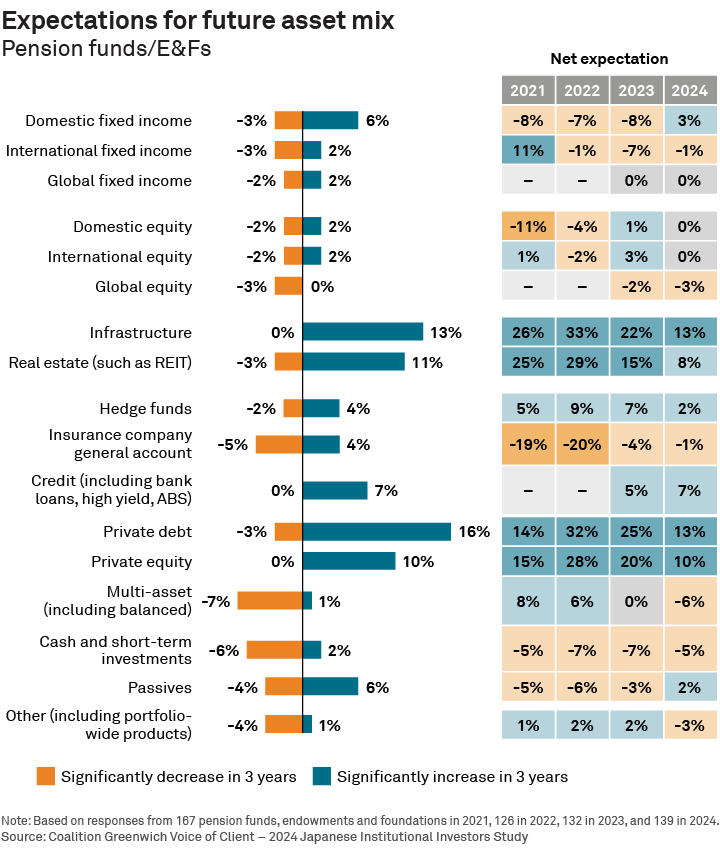

A slowing shift into private markets

In what could be a silver lining for traditional asset managers in Japan, it seems that at least part of the slowdown in manager hiring could be coming from private markets. Like investors around the world, financial institutions and pension funds in Japan have been making a big push into private assets. In 2023, nearly 40% of Japanese financial institutions and more than a quarter of pension funds were planning significant increases to private debt allocations over the coming three years. Japanese investors were also bullish about future allocation increases to alternative asset classes such as infrastructure and private equity.

Although institutional investors plan to continue increasing their exposure to private markets, they appear to be moderating the pace of that change. To get a better sense of how future allocation shifts might play out, it’s helpful to look separately at plans among pension funds, endowments and foundations on the one hand, and financial institutions on the other.

Among pension funds, endowments and foundations, the share of investors planning to significantly increase private debt allocations in the next three years dropped roughly 10 percentage points year over year to 16% in 2024. Private equity experienced an equal 10 percentage point drop to 10%. These findings suggest that, although Japanese pension funds, endowments and foundations remain committed to building up allocations to private assets, they intend to move more deliberately in the coming year.

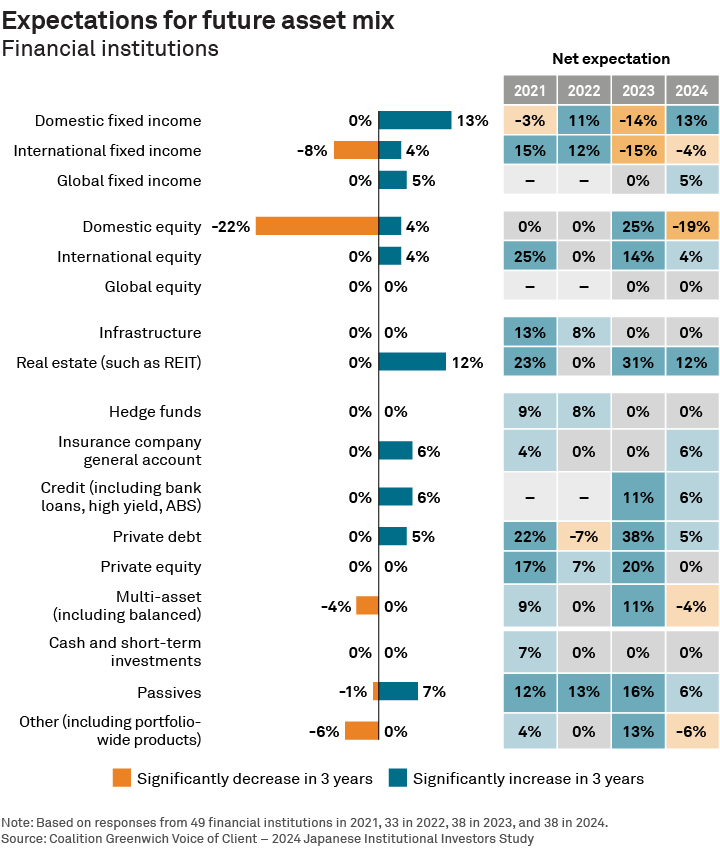

The change has been even more dramatic among Japan’s financial institutions, which appear to have embraced a more fundamental shift in near-term portfolio strategy. In 2023, financial institutions were planning a bold move into private debt, and, to a slightly lesser extent, private equity. These inflows were to come from meaningful net reductions in both domestic and international fixed income. In 2024, the share of financial institutions planning significant increases to private debt allocations dropped to 5%. Not a single financial institution participating in Crisil Coalition Greenwich research in 2024 expects to significantly increase allocations to private equity in the next three years.

Meanwhile, financial institutions are predicting notable shifts in allocations to traditional asset classes. Twenty-two percent of financial institutions expect to significantly reduce allocations to domestic equities in the coming year, while 13% are planning major increases to domestic fixed income.

A continued challenge for traditional managers

At the moment, it remains unclear what’s driving investors to slow the growth of private strategy allocations. Since investors are signaling that they remain committed to private markets over a long-term horizon, the current slowdown could simply reflect capacity constraints in a global private debt market that is still growing and maturing. It could also be a reflection of the many new internal challenges investors everywhere face in building up allocations to illiquid asset classes, and institutions’ need for a pause to implement past commitments. However, the magnitude of some of these changes could suggest a broader strategic shift in the face of tightening by the Bank of Japan and the increase in JGB yields to the highest levels seen in decades.

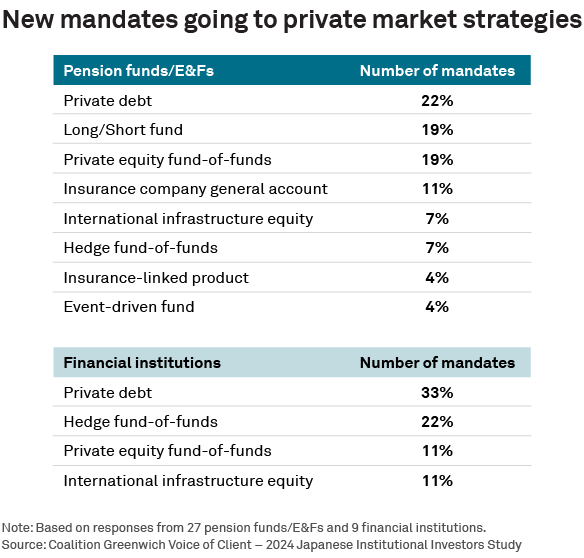

Despite expectations for a slowdown in the shift of assets to private markets, traditional asset managers competing for business in Japan will remain under pressure. As shown in previous tables, private strategies are making up a large share of new mandates that do emerge.

Diverging paths on ESG

About half of Japanese institutions consider environmental, social and governance (ESG) criteria when selecting an asset manager. The fact that this share remained roughly flat to even slightly lower over the past 12 months could reflect a loss of momentum for ESG in markets around the world.

In the United States, backlash against ESG is intensifying with the new Trump administration. Some of the largest asset managers in the U.S. are backing off prior climate change commitments, and some individual U.S. states have barred anyone investing public funds from considering ESG factors in their investment decisions. As a result of these policy changes and expectations of an even broader crackdown ahead, the share of asset owners in the U.S. that consider ESG when selecting asset managers has dropped to just 38%.

The situation is entirely different in Europe, where both governments and asset owners remain committed to ESG. More than 90% of asset owners in Europe consider ESG when selecting an asset manager. However, even in Europe, the ESG halo has been tarnished to some extent. In particular, controversy over “greenwashing” has prompted many financial institutions to drop the “ESG” moniker entirely in favor of terms like sustainable investing. Regardless of these cosmetic changes, the principles underlying ESG will remain firmly embedded in the European asset management industry.

In Japan, most asset owners think the influence of ESG will remain about the same in coming years, meaning that some asset owners will employ ESG criteria, and some will not. This divergence in approach among asset owners within Japan and across global regions represents a significant challenge for asset managers, who will have to navigate a complicated matrix of preferences among potential clients—and regulators—as they compete for mandates at home and around the world.

Parijat Banerjee, Seiji Ishii and Atsuyuki Kubota advise our investment management clients in Japan.

Methodology

From April through October 2024, Crisil Coalition Greenwich conducted interviews with 254 of the largest corporate pension funds, public pension funds, financial institutions, and endowments and foundations in Japan. Total fund assets were ¥949 trillion. Senior fund professionals were asked to provide quantitative and qualitative evaluations of their investment managers, qualitative assessments of those managers soliciting their business, and detailed information on important market trends.