Three trends signal direction of European asset management

Share

Share

Executive Summary

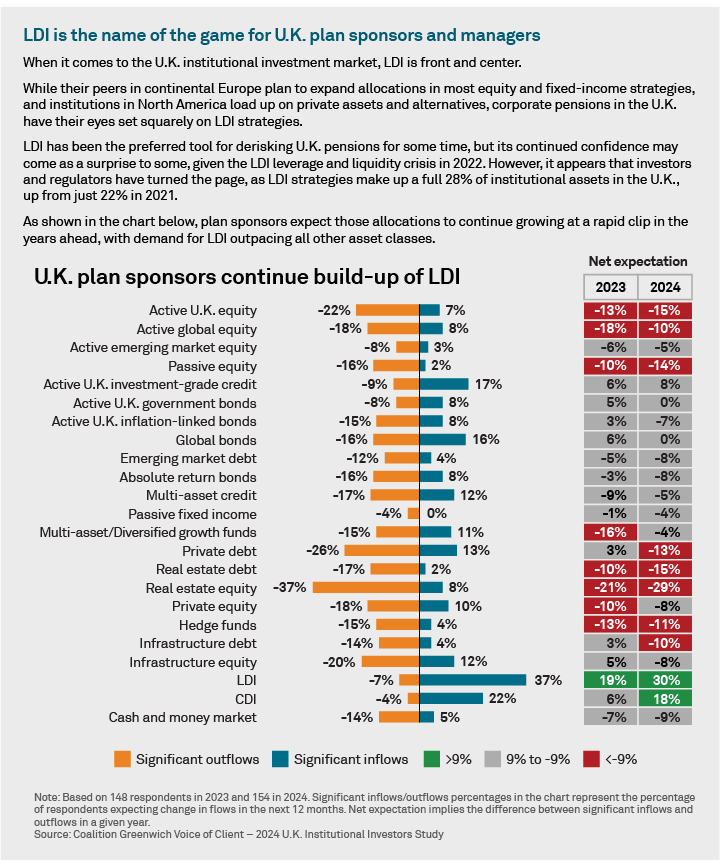

European investors enter 2025 with a surprising level of optimism given the set of economic, political and geopolitical challenges facing Europe’s investment markets. In continental Europe, pension funds, insurers and other institutions expect to significantly increase allocations to equity and fixed-income products in the year ahead, while also increasing their exposures to alternative asset classes. In the United Kingdom, corporate plan sponsors are committed to immunizing defined benefit pension schemes and plan to continue that work by upping their allocations to liability-driven investment (LDI) strategies.

Methodology

From January to August 2024, Crisil Coalition Greenwich conducted interviews with 252 of the largest institutional funds in the United Kingdom and 372 key decision-makers at the largest continental European institutional investors. Institutional investors in the U.K. included corporate funds, local authorities and other institutional funds. Institutions in continental Europe included corporate, public, and industry-wide defined-benefit, defined-contribution and hybrid pension funds, banks (including Sparkassen in Germany), foundations and churches, insurance and reinsurance companies, sovereign pension reserve funds, and other non-pension institutional investors including official institutions, central banks, monetary authorities, sovereign wealth funds, and supranationals. Between April and July 2024, Crisil Coalition Greenwich conducted 180 interviews with some of the largest fund distributors in Europe. Senior gatekeepers were asked to provide detailed information on their business priorities, quantitative and qualitative evaluations of their investment managers, and qualitative assessments of those managers soliciting their business. In 2024, Crisil Coalition Greenwich undertook a study with asset managers to assess the latest trends in product development and management. Globally, we gathered feedback from 74 senior stakeholders at 68 firms on their views of the current product landscape, including product development and management approaches and processes, differentiators, product shelf outlook, stakeholders and product review triggers. In addition, this report summarizes the findings from a flash study in August 2023 with 99 asset managers on the evolving role of AI in asset management.

In this paper, we present some highlights from our 2024 European Investment Management studies. An analysis of data from that research reveals three trends that will help define the direction of the asset management industry in continental Europe and the U.K. in the months and years to come:

- Investors embrace barbell “lite”: With more opportunities to take on exposures to private markets and other alternatives, institutional investors and intermediary distributors across Europe are moving toward barbelled portfolio strategies, however with a limited scope compared to other markets.

- A new, data-driven ESG: European investors remain deeply committed to ESG and are advancing into a new phase characterized by improved reporting, better data and an emphasis on quantifiable impact.

- Differentiation through operations: Asset managers directly interact with their clients only a handful of times every year, but clients interact with manager data every day. As reporting and data delivery make up a bigger part of the client experience, asset managers have an opportunity to differentiate themselves with best-in-class operations.

Investors embrace barbell “lite”

European investors are gravitating to what we at Crisil Coalition Greenwich have dubbed “barbell lite” portfolio allocation strategies. The barbell strategy has become popular among investors around the world, and that truth holds in Europe as opportunities to access alternative strategies expand.

Investors using a barbell approach take on large allocations to low-cost passive strategies in public asset classes in which they perceive more modest opportunity for alpha generation, and sizable allocations to high-alpha strategies, largely in alternative asset classes. The losers in this deal are traditional active strategies that fall between these two poles.

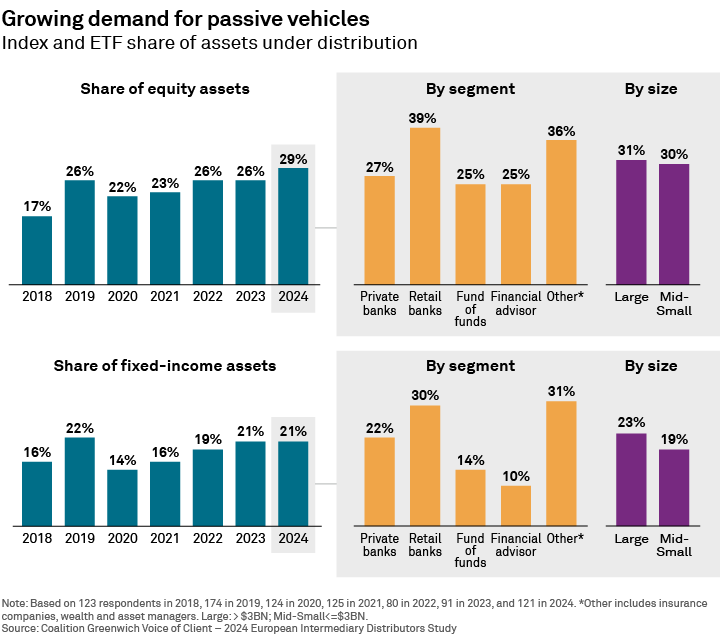

European investors are adopting this approach but at a slower pace and on a smaller scale than we’ve seen in other regions, North America in particular. For example, investors on intermediary distribution platforms in continental Europe have been steadily increasing their allocations to index and ETF products, typically for passive strategies, which have grown from just 22% of total assets in 2020 to 29% in 2024. In fixed income, allocations to these products increased from 14% in 2020 to 21% in 2024.

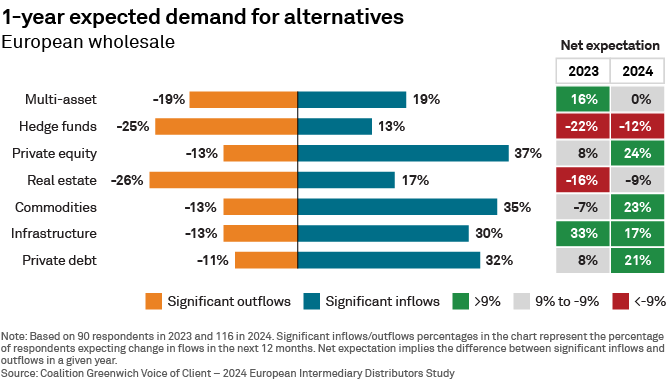

Meanwhile, investors are generally planning to increase allocations to alternatives. As shown in the graphic above, more than a third of intermediary fund distributors in continental Europe and the United Kingdom expect investors on their platforms to significantly expand allocations to alternative asset classes such as private equity, commodities and private credit in the next year.

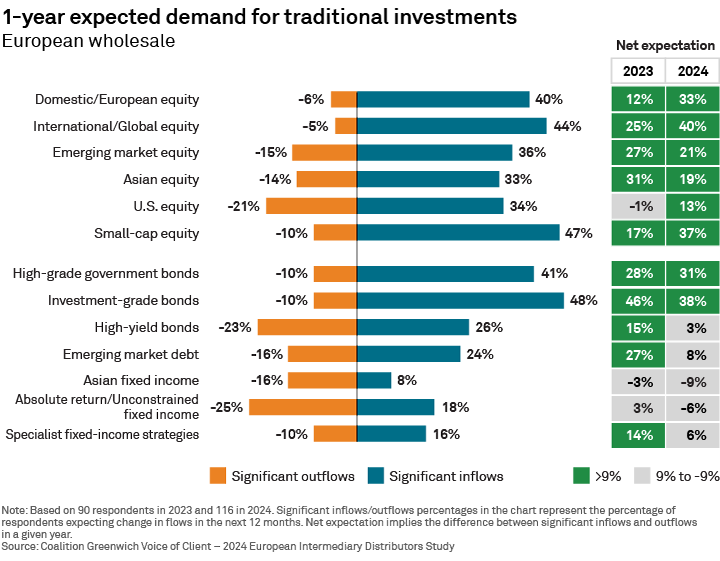

However, it’s important to note that expected demand for traditional equity and fixed-income strategies is likely not only to hold up next year, but to top demand for alternatives by a sizable margin. That’s the “lite” in barbell lite. As shown below, more than 40% of intermediary fund distributors in Europe expect investors on their platforms to significantly increase allocations to a list of traditional asset classes ranging from international/global equities and small-cap stocks to investment-grade bonds.

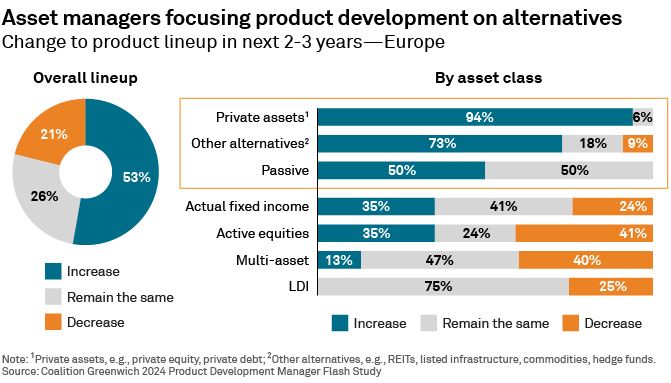

Although demand for traditional active strategies appears solid for the moment, we believe investors in Europe and around the world will continue moving from “barbell lite” toward a fuller barbell approach, as managers continue to roll out new semi-liquid products designed for the wealth channel and opportunities to take on private and alternative exposures expand. Almost 95% of the European asset managers participating in a 2024 special study on product development expect to expand their product lineups in private markets, and nearly three-quarters expect to increase the number of alternative products they offer overall.

A new, data-driven ESG

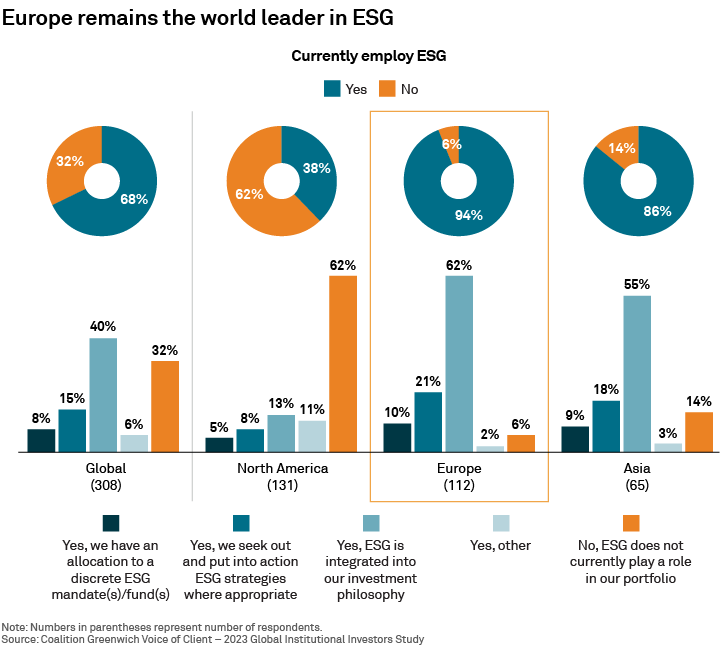

Environmental, social and governance investing (more often called sustainable investing) has permeated the European investment industry and is now moving into a more mature, and hopefully more stable and effective phase characterized by better and more actionable data. Aggressive action by EU regulators and social pressure from both consumers and civil society more broadly fueled the rapid rise of ESG across European investment markets. Europe is by far the leader in ESG adoption, with nearly 95% of European institutional investors employing ESG in their investment processes and portfolios. That’s in sharp contrast to practices in North America, where only 38% of institutions currently employ ESG.

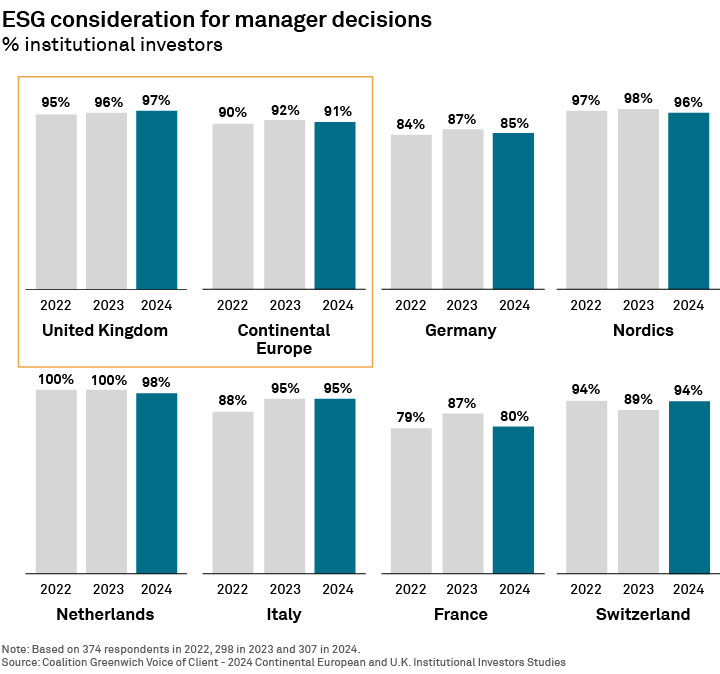

As shown in the preceding graphic, ESG capabilities have become an essential feature for asset managers competing for investment mandates in Europe. In the intermediary channel, more than two-thirds of fund distributors now require asset managers on their platforms to have a clear and comprehensive ESG policy.

As it spread throughout Europe, ESG has been in a constant state of evolution. Initially, most asset managers implemented ESG mainly through screens that filtered out companies and investments that ran afoul of ESG criteria. The next step was the launch of dedicated funds and products that featured ESG exposures as their raison d’être.

More recently, asset managers have responded to demands from the market and regulators by fully integrating ESG into their core investment processes and every investment product. Today, 62% of European asset managers have fully integrated ESG into their investment philosophy. Again, that approach diverges dramatically from practices in North America, where only 13% of managers say they have integrated ESG into their investment processes.

ESG is continuing to evolve. Over the past decade, greenwashing scandals, concerns about performance and questions about how best to make and measure impact have stirred up controversy about ESG. Rather than dissuading institutions from adopting environmental and social considerations into their investment processes, these issues have prompted European investors to hone ESG data, methodologies and even marketing strategies to ensure better outcomes. Regulators have also contributed by implementing the EU Sustainable Finance Disclosure Regulation (SFDR), which has helped improve corporate reporting standards and standardize ESG data, allowing for more accurate analysis of impact and better decision-making.

Those efforts are paying off. ESG data is becoming more actionable. In 2023, roughly 40% of European intermediary fund distributors cited “difficulty measuring impact” as a serious obstacle to additional ESG integration. In 2024, that share dropped 10 percentage points.

So, despite some serious obstacles, momentum for ESG shows no signs of slowing in Europe. To the contrary, nearly 70% of European institutional investors expect ESG’s influence to increase over the next 12 months. That said, the ESG of the future will look much different than the ESG of the past. In fact, it probably won’t even be called ESG. Given recent greenwashing scandals, many asset managers, institutional investors and companies are dropping the name “ESG” altogether in favor of less loaded terms like stewardship and sustainability.

In the next, more mature phase of ESG, investors and companies will spend less time marketing and brand-building around these issues, and more time generating and quantifying impact. That means more accurate and standardized reporting, better and more reliable data, and more active ownership, in which investors generate impact by working directly with portfolio companies to change practices.

Differentiation through operations

With alpha getting harder to come by in traditional equity and fixed-income strategies, many asset managers have worked to differentiate themselves as providers of superior client service. While our research demonstrates the efficacy of that strategy-managers deemed as having best-in-class service get more cross-sales and more leeway from clients during times of poor performance-it’s also getting harder to stand out as more firms focus on service. So where can managers turn for a competitive advantage? Although it might seem curious, we think the next frontier for differentiation could be operations.

Institutional asset managers directly interact with their clients only a handful of times every year, but clients interact with manager data every day. As cloud computing unlocks seamless connectivity, data analytics become more powerful and AI permeates investment markets, asset managers have an opportunity to stand out from the crowd based on the quality and ease of their reporting, operational capabilities and general ease of doing business.

European institutions say recent technology rollouts from their managers have improved core functions like reporting, portfolio analysis, research, and due diligence. Nevertheless, institutional investors remain lukewarm about their managers’ technology offerings overall. Only about half of institutions in continental Europe and 40% in the U.K. give their managers high marks for their technology propositions. That finding suggests there is a real opening for managers to brand themselves as sophisticated organizations whose technology delivers real benefits to clients.

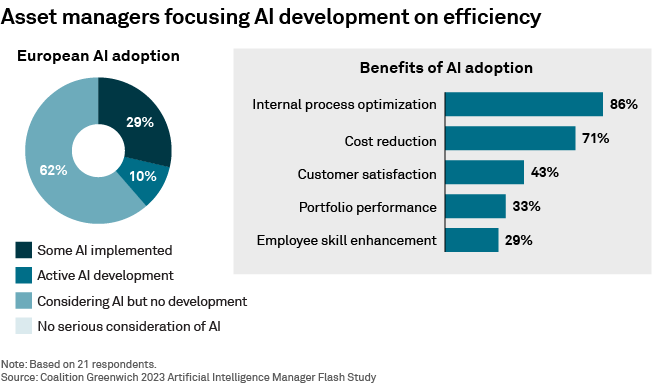

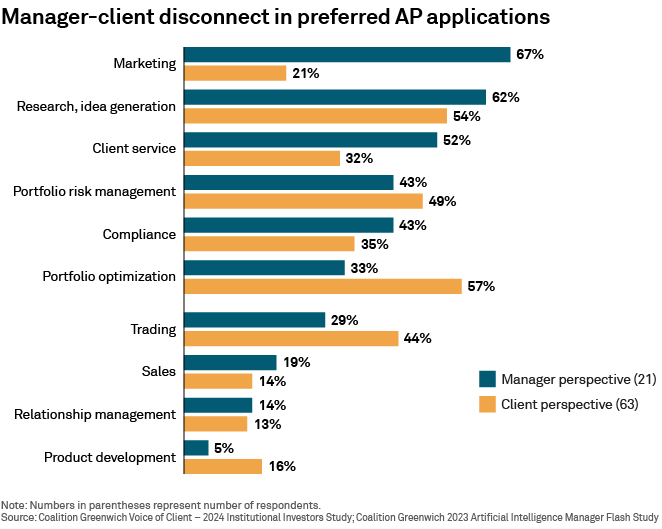

AI should be helping managers capitalize on this opportunity. Nearly a third of European asset managers say they have implemented AI or are in active development of AI applications. For the most part, however, these early AI initiatives are focused on optimizing internal processes and lowering costs.

We believe strongly that asset managers who prioritize reporting, data delivery and other operational capabilities in their development budgets for technology in general and AI in particular have an opportunity to build a competitive advantage over their rivals by helping institutional clients seamlessly receive, digest and analyze data.

Christopher Dunn, Kryszia Bisson and Alastair Brown advise our investment management clients globally.