Top trends in asset management for 2025

January 14, 2025

Report

Mark Buckley

Parijat Banerjee

Kryszia-Bisson

Noam-Cotton

Christopher Dunn

John Feng

Susan Gould

Emma-Haffenden-Back

Seiji-Ishii

Ken Yap

Report

Mark Buckley

Parijat Banerjee

Kryszia-Bisson

Noam-Cotton

Christopher Dunn

John Feng

Susan Gould

Emma-Haffenden-Back

Seiji-Ishii

Ken Yap

Share

Share

Executive Summary

The ascendency of private market strategies, an innovation boom in ETFs and the growing challenge of a trans-Atlantic divide on ESG are just some of the trends that will help define the global asset management industry in the year ahead. In this report, we draw on our research with institutional investors and intermediary distributors, and relationships with our asset manager and investment consultant clients around the world, to identify seven important trends to watch in 2025.

Introduction

The ascendency of private market strategies, an innovation boom in ETFs and the growing challenge of a trans-Atlantic divide on ESG are just some of the trends that will help define the global asset management industry in the year ahead. In this report, we draw on our research with institutional investors and intermediary distributors, and relationships with our asset manager and investment consultant clients around the world, to identify seven important trends to watch in 2025:

- The semi-liquid revolution: The sale of semi-liquid alternative products into the wealth channel will be a key source of AUM and revenue growth for asset managers.

- Great service in private strategies: Traditional asset managers entering private markets are raising the bar on client service.

- Relationship management more important than ever: RMs have always been the cornerstone of asset management relationships, but as institutional investors’ needs become ever more complex, RM performance will matter more than ever.

- Slowing customization creep: 2025 could be the year asset managers start taking a more nuanced approach to meeting clients’ customization requirements.

- Rethinking investment consultant relationships: Some asset managers are already rethinking their approach to consultant relations to transform the relationship into a partnership in order to bring the best ideas to the shared client.

- ESG rift divides a global industry: The election of Donald Trump will make an already complicated situation even more challenging for global asset managers attempting to navigate diverging views on environmental, social and governance investing.

- ETFs: The cradle of innovation in asset management: The boom in exchange-traded funds could further accelerate in 2025 as ETFs solidify their status in the industry as the place where innovation happens.

The semi-liquid revolution

Investors in 2025 will see a continued boom in new and innovative semi-liquid alternative products in the wealth channel.

Asset managers selling alternative strategies and private market investments are targeting wealth as a top source of AUM growth. That includes both private market specialists, who are expanding franchises into high-net-worth from their mainstay institutional base, and traditional asset managers, many of which are introducing alternative strategies into existing wealth distribution businesses.

All this expansion can be traced to the growing popularity of semi-liquid products—open-end funds that allow investors to take on exposure to illiquid alternative and private assets while retaining the ability to periodically redeem at least a defined portion of their stake.

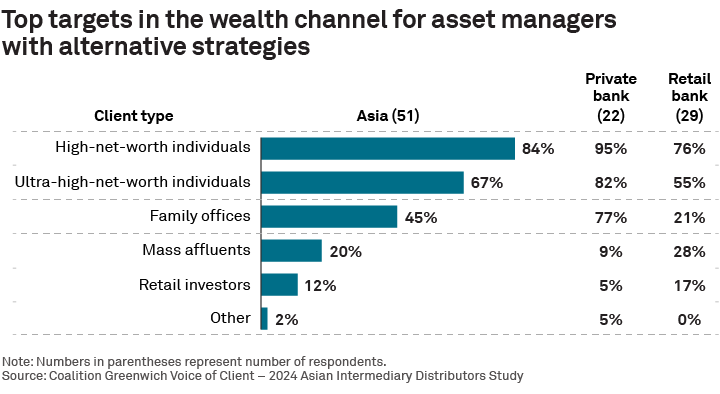

Look for asset managers to build on that momentum in the year ahead by rolling out a steady stream of new products and fund structures covering an expanding array of alternative asset types and strategies. As shown in the following chart, which is based on conversations with intermediary distributors in Asia, asset managers debuting these products are targeting high-net-worth and ultra-high-net-worth investors through private banks and on third-party fund distribution platforms, and through family offices.

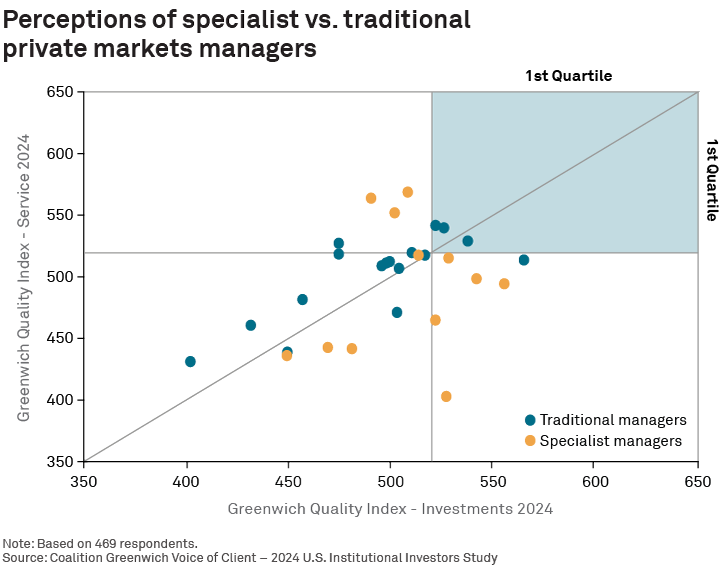

Great service in private strategies

Specialist asset management firms that have long dominated private markets have, in many cases, paid less attention to client service and the client experience.

That situation is changing as private markets evolve. The tremendous growth in private debt, private equity and other alternative asset classes has attracted new competitors from the ranks of traditional asset management. Many of these firms have bountiful resources and customer service baked into their DNA. As they enter these new markets, they are raising the private markets’ service bar.

Incumbent specialists are aware of the “service gap” between themselves and traditional managers, and they have already started working to close it. Specialist managers are hiring CX professionals, reassessing the role and skill sets of client-facing professionals, gathering independent client feedback, benchmarking service levels relative to market leaders, and embarking on other initiatives to ensure that the corporate culture focuses on service.

For specialists, replicating the service capabilities of traditional managers, most of whom have adopted client-centricity as a core organizational strategy, will be easier said than done. Regardless of how close specialist firms can come to matching the service standards set by traditional managers, the main beneficiaries of this competition will be clients, who should experience a steady improvement in client service standards in private markets strategies in 2025 and beyond.

The role of relationship managers will continue to increase in importance

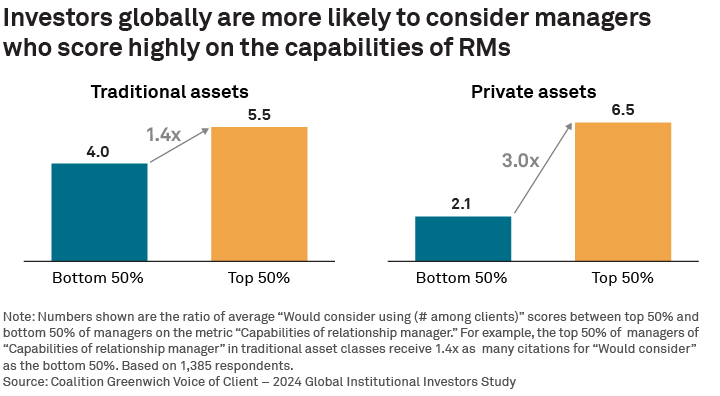

RM performance has always had a significant impact on client retention, cross-sales and brand favorability. In traditional strategies, managers whose RMs rank in the industry’s top 50% in terms of client ratings on capabilities are 1.4 times as likely as other firms to be considered for a new traditional mandate, and 3.0 times as likely for private assets.

Clients today expect their asset managers to do more than simply deliver alpha. Managers are expected to understand clients’ unique goals, challenges and strategies, and to provide solutions and a customized level of service. Meeting those expectations requires close cooperation among teams across an asset management organization, including investment, distribution, client service, technology, and others.

The RM is the point of the spear, coordinating work and resources from across these groups and delivering results to clients in a timely, responsive and accessible way. To do so, RMs must possess both the skill and the organizational empowerment to “bring the firm” by accessing client data, technology—including analytics and other AI applications—account planning resources, and intellectual property that allow them to broaden and deepen conversations with clients.

In the best-case scenario, these efforts elevate the manager to the status of a strategic partner in the eyes of the client—a designation that pays huge dividends in terms of client retention and cross-sales. Regardless of whether a manager ever rises to that level, the strength and performance of the client relationship is increasingly influenced by the quality of the RM. For that reason, asset managers should consider ways to strengthen their RM teams while also formalizing their process for monitoring RM performance by benchmarking client ratings against objective scores for rival firms.

Slowing customization creep

Customization has been the buzzword in institutional asset management. However, we believe 2025 could be the year asset managers start altering their approach to the trend by taking a less expansive and (do we dare say?) more customized approach to customization.

Asset managers around the world have embraced client-centricity as a defining strategy. Although that commitment has resulted in significant improvements to the client experience (as documented in Coalition Greenwich research into client satisfaction rates), it has also resulted in “customization creep.” To win a mandate or build a foundation for a future cross-sale, salespeople have become incentivized to promise client-specific or customized products or service. Once those promises are made as part of the sales process, client service teams and the rest of the organization are obligated to deliver.

The costs of those promises are adding up. Most asset management firms are not built to be custom client service engines, and managers often have to create new operational processes to meet customization commitments. Although some large managers are working to build scalable solutions that can be used to customize relationships with any client, the vast majority of customization projects are conducted on a one-off basis. New tools or products developed and deployed for individual accounts can be a major drain on profitability.

We expect growing numbers of asset managers to consider how they are addressing customization strategically (do they do it, and if so, to what degree) and tactically (how do they do it efficiently). As they do so, we’re advising our clients to adopt these five approaches that can help address customization creep:

- Establish tiering standards: Clients should be tiered by specific needs, potential wallet or other metrics, and the scope of services offered to each tier should reflect its relative importance. While all clients should receive good service, clients are not created equal and should not be treated as such. Critical to this element is the internal enforcement of standards.

- Offer a menu: Managers should develop a set of specific client services that offers a distinct advantage over competitors. These services (reflective of the client’s tier) should be offered to new clients as part of the onboarding process.

- Set a cadence: Knowing that clients may oversubscribe to the tier-specific services, the manager should establish regular coaching touchpoints with the client to ensure they are getting the most out of the overall services agreement.

- Trim the offering: Ultimately, the goal is to improve the client’s overall level of satisfaction while reducing the number of specific services offered, giving the client exactly what they need and saving the manager unnecessary costs and resources that could be deployed elsewhere in the client’s favor.

- Invest in technology: Despite the upfront investment, client service technologies such as client portals and APIs enable service at scale. Leveraging a flexible, user-friendly data platform will empower clients to self-serve and permit more transparent, secure transfer of information between clients and managers.

Consultant relations doubles down on relationships

Recognizing the impact that consolidation among investment consultants is having on the industry, forward-thinking asset management firms will be adjusting their approach to consultant relations in 2025.

The use of investment consultants is nearly ubiquitous among institutional investors in the United States and the United Kingdom, and only slightly less widespread in Canada. In recent years, consultant use has started climbing in continental Europe, where usage rates rose from 29% in 2022 to 35% in 2024.

Part of this growth can be attributed to diversification in institutional investment portfolios. As asset owners take on exposures to alternatives, private markets and other new asset classes, they are less familiar with investment strategies and the asset managers who offer them. Although investment consultants have worked hard to expand and deepen the range of services they provide, manager selection remains by far the No. 1 reason institutional investors hire consultants.

M&A activity among investment consulting providers is adding to the clout of surviving firms. For example, in 2014, the top 20 investment consultants in the U.S. held about two-thirds of institutional client relationships. By 2023, consolidation among consultants had driven that share to 85%.

More than ever, big investment consultants prize partnership. As consultants’ clients move into strategies that are new, less-liquid and more complex, they are looking for asset managers who can work with them to educate asset owners about specific markets and strategies, and explain how the manager’s products are differentiated from others on offer.

Across all asset classes, investment consultants are trying to position themselves as solutions providers as opposed to simple intermediaries in manager searches. As they do so, they are seeking managers willing to partner with them to build flexible, personalized and even custom product solutions for important clients.

It is the job of the consultant relations team to forge those partnerships—a task that entails both building out the relationship to understand the specific needs and demands of the consultant organization, and marshalling the internal resources needed to meet those needs.

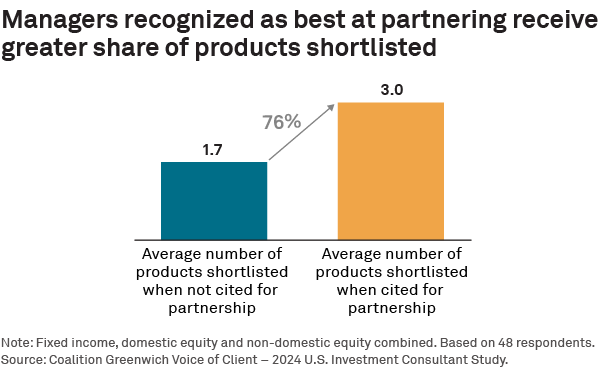

If all that sounds like a lot of costly work, there is a payoff. Data from our annual global Investment Consultant Study shows that asset managers rated by consultants as best-in-class at partnering have a significant advantage over competitors when it comes to getting their products shortlisted by consultants.

ESG rift divides a global industry

The election of Donald Trump will make an already complicated situation even more challenging for global asset managers attempting to navigate diverging views on environmental, social and governance investing.

The U.S. and the rest of the world have been moving in opposite directions on ESG. In Europe, about 90% of institutional investors say they consider ESG criteria when choosing an asset manager. In the U.S., that share topped out at 55% in 2022 before dropping to 47% in 2023 and just 38% in 2024.

In the U.S., the backlash against ESG has been fueled by questions among investors about ESG’s ability to enhance returns and about potential violations of fiduciary duty to clients by asset managers who include non-investment-related criteria into their decision-making. Around the world, investors and regulators have identified instances of “greenwashing” and exaggerated ESG claims by asset managers and corporations. These issues have become so pronounced that the very term “ESG” is falling out of favor, not only in the U.S., but also in Europe and other areas, replaced by sustainability, responsibility and other alternatives.

But those concerns have not, in any way, weakened the commitment of non-U.S. investors to make environmental and social considerations a core part of their investment decisions. Outside the U.S., the integration of ESG into manager selections and investment processes is being driven by a combination of market demand and regulatory action. The EU is leading the push for global ESG governance and standards with common reporting metrics and disclosures.

Regardless of any pushback in the U.S., the impact of this global embrace of ESG investing is just too large for asset managers to ignore—even if they wanted to. Bloomberg Intelligence expects ESG assets to make up one-third of total global assets under management in 2025.

Against that backdrop, the return of Donald Trump to the White House could put global asset managers in a bind. A new Trump administration is likely to target ESG-friendly rules from both the Securities and Exchange Commission and the Department of Labor. A reversal on those and other ESG-related regulations would make it even harder for asset managers to operate and market funds incorporating environmental and social criteria.

Those changes could radically alter the landscape for global asset managers. Sustainable investments and being able to clearly evidence incorporation of sustainable principles are important to AUM growth in Europe and Asia. However, managers from those regions might not be able to sell their ESG-based offerings in the U.S.—an obstacle that will become even more daunting as these managers move from selling ESG-specific funds to incorporating ESG into their investment process for all products. Meanwhile, U.S. managers who scale back or eliminate ESG at home would find themselves at a huge disadvantage when competing for mandates in Europe and Asia.

Some global asset managers are already using dual pitchbooks to market products inside and outside the U.S. However, if ESG rules and practices continue to diverge, the challenge for global managers will go well beyond any marketing fix. In 2025, the entire asset management industry will be watching to see how the growing ESG divide affects business strategies and global franchises.

ETFs: The cradle of innovation in asset management

The boom in exchange-traded funds will continue and possibly even accelerate in 2025 as ETFs solidify their status in the industry as the place where innovation happens.

Over the past decade, the overall size of the ETF market has increased nearly fivefold, to roughly $13 trillion. This growth represents a new evolutionary stage for ETFs that we believe is just beginning.

For much of the three decades since the launch of the first ETF, AUM growth has been driven mainly by the explosion of demand for passive investment strategies. That situation has changed, dramatically. For the past two years, more than 60% of new ETF listings in the U.S. have been active investment strategies. Asset managers are harnessing the versatility, flexibility and liquidity of ETFs to create new actively managed products covering everything from traditional strategies to alternatives.

Despite that growth, active strategies represent under 10% of the ETF market. We believe that share will climb in 2025 and continue rising for years to come. Innovation in active strategies will fuel additional growth in global ETF AUM, which is still only about one-third that of mutual funds.

Non-traditional assets will contribute to the next phase of ETF proliferation. In September, State Street and Apollo Global Management filed to launch the first actively managed ETF that invests in both public and private credit. The approval of that fund could open the floodgates to a new breed of ETFs that directly hold private assets. ETFs have also facilitated investor access to cryptocurrency since the first Bitcoin ETF launched in 2021. Today, there are over 60 crypto ETFs. The market structure impact of these fund launches will only get bigger over time.

We see several other trends that will fuel ETF growth in 2025. First, as demand for ETFs grows, large asset managers who have not jumped on the ETF band wagon will feel the pressure to offer ETF opportunities as part of their overall product strategy. Actively managed ETFs represent a potential opportunity for these firms to deliver differentiated products and avoid me-too offerings. Conversion of existing mutual funds to ETFs is already contributing to ETF growth.

Second, until now, ETFs have been slow to gain traction in some key channels, including among institutional investors and in 401(k) plans. Institutional adoption of ETFs has been growing, and we expect this trend to continue. Given its sheer size, even incremental increases in institutional usage will have a major impact on global ETF AUM. Third and finally, the ability to customize ETF products to meet specialized needs and exposure requests will continue driving new demand among both retail and institutional investors. (For additional insight into the evolving role of ETFs from our Market Structure & Technology team, see Top market structure trends to watch in 2025.)

Mark Buckley, Parijat Banerjee, Kryszia Bisson, Noam Cotton, Christopher Dunn, John Feng, Susan Gould, Emma Haffenden-Back, Seiji Ishii, and Ken Yap advise investment management firms globally.