A continuous economic and geopolitical ‘poly-crisis’ is creating a powerful incentive for companies around the world to invest in trade finance and supply chain management capabilities. This new focus is accelerating digitisation and opening the door to next-gen solutions with the potential to make these core corporate functions more transparent, flexible and efficient.

Companies use trade and supply chain finance for two main reasons: First, as a form of debt finance where the buyer’s bank assumes the responsibility of paying the seller and takes the risk on the buyer having performed its own due diligence, and second, as a means of managing risk of non-delivery those goods. If a buyer pays up front, there is no leverage if the goods do not arrive. With trade finance, it’s banks that take on this risk – and therefore create a bridge between the seller and the buyer. At the macro level, risk is often triggered by geopolitics while at the micro level it is often prompted by distrust in the counterparty. In both cases it drives corporates’ appetite for trade finance – in addition to the availability and cost of bank loans and capital markets funding.

Hence, just a decade ago, when interest rates and funding costs were still at historic lows, globalisation was on the march and no one had heard of a coronavirus, the reasons for using trade finance were very different than they are today. When CFOs turned their attention to supply chain management, it was mainly to reduce production costs by shifting manufacturing to lower-cost markets and to achieve higher efficiencies by perfecting just-in-time production.

The situation could not be more different today. Large companies face an expanding list of interconnected challenges. ‘Higher for longer’ interest rates are pushing up corporate funding costs. The normalisation of trade flows and supply chains in the wake of the global pandemic has been interrupted by a series of new disruptive events, including wars in the Ukraine and the Middle East, and attacks on shipping in the Red Sea. Geopolitical tensions between China and both the European Union and the United States were disrupting global trade even before the return of Donald Trump to the White House. Since his inauguration in January 2025, the announcement of tariffs and the threat of additional levies have added further barriers to established trade corridors.

In this environment of rising costs and risks, companies see the possibility of a much bigger payoff from any initiative that increases efficiency and flexibility. That dynamic is changing the return on investment (ROI) equation for global corporates on investments in trade finance and supply chain management.

Trade finance as a funding alternative

With uncertainty on the rise, corporate treasury departments are using every tool at their disposal to shore up balance sheets and ensure access to credit. Every year, Crisil Coalition Greenwich asks more than 2,500 CFOs and group treasurers of large corporates around the world to name their departments’ top priorities for the next 12 months. In 2024, participants from North America, Europe and Asia named “financing and refinancing” as their top priority for the coming year by a significant margin.

Corporate borrowers working to refinance existing low-cost debt in today’s higher-rate environment have been hoping for relief from continued central bank rate cuts. Although the European Central Bank as well as the Bank of England appear, at least for now, on track for more easing despite a recent uptick in prices, stubborn inflation data in the US has caused the Federal Reserve to pause, with some economists even seeing the chance for a rate increase in 2025. The upshot – it is much less likely corporate funding costs will drop significantly any time soon.

Trade credit provides a direct source of financing that can help offset high borrowing costs or limited credit availability because a third party in the form of the financier takes the risk on the buyer and seller. This alternative is especially important to companies in Asia where one-third of corporates experienced financing issues in 2024; up 12% from the year before.

Asian companies last year also cited additional concerns, such as FX volatility, payment delays and a lack of credit availability at acceptable terms. These issues seem especially acute in China, where financing has become tougher to secure and more expensive. Companies in China report that, over the past 12 months, foreign banks operating within China – especially European banks – have become more conservative in extending balance sheet.

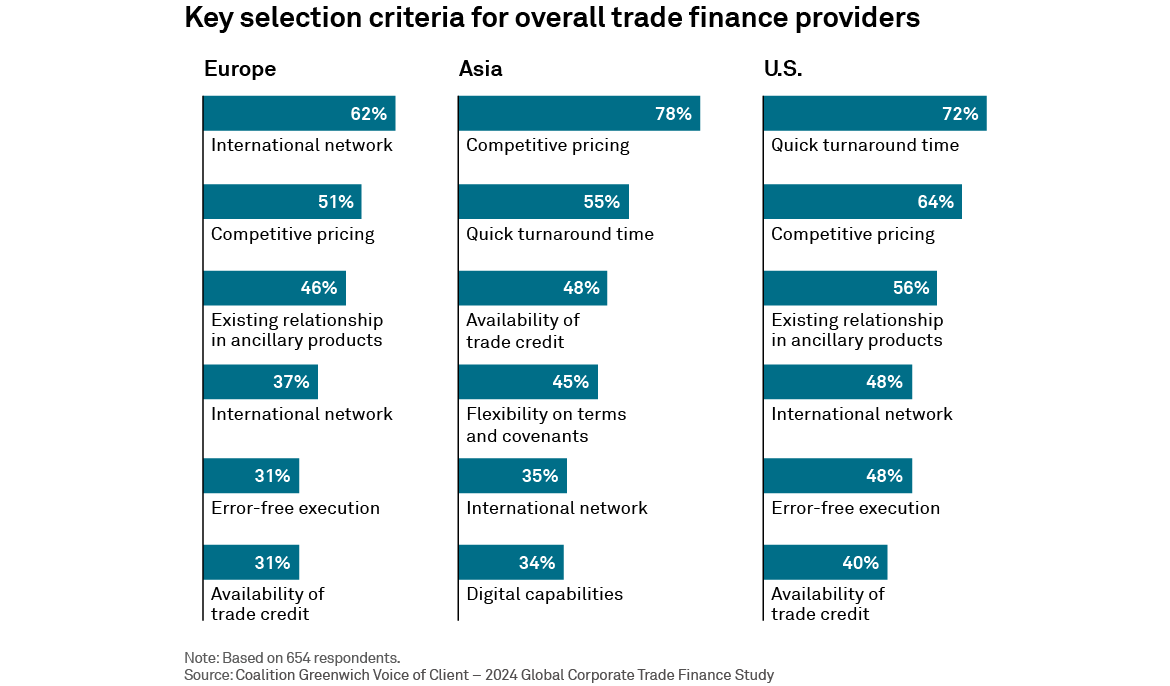

Reflecting that challenging funding environment, roughly half of large corporates across the Asia region now cite “availability of trade credit” as one of the key reasons for choosing a bank for transaction banking services, versus 40% of US corporates and only around 30% of large companies in Europe.

Share

Share