The customization conundrum: Satisfying clients without hurting the bottom line

Share

Share

Introduction

Two decades ago, most corporate credit-investing strategies operated primarily by owning (or not) corporate bonds. Larger institutions utilized credit default swaps (CDS) to hedge default risk or gain synthetic exposure, but otherwise, bonds were it. Bonds were bought and sold via relationships and phone calls; systematic credit investing was rare, and systematic credit trading non-existent.

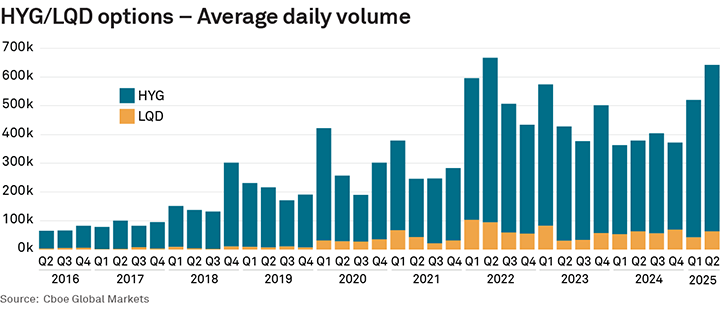

Fast forward 20 years: 44% of U.S. corporate bond volume trades electronically, up from nearly zero,1 with dealers executing nearly one-third of orders with no human intervention.2 Portfolio trades make up 10% or more of volume on any given day, credit ETF volume equates to 15–20% of the notional volume traded in the bond market, and systematic investing and trading is all the rage.

Despite this progress, a robust futures market—something taken for granted by interest-rate and equity traders—has, until recently, eluded the credit market. This is not for lack of trying. The first batch of new contracts launched in 2007 before the financial crisis hit its stride, with additional offerings coming after Dodd-Frank in 2012. Those contracts worked to mimic the CDS market, bringing CDS exposure into a futures framework under the assumption that new, more stringent oversight of the swaps market would drive traders elsewhere. That focus on converting swaps traders to futures and bringing futures traders into the credit market ultimately did not work.

The SEC’s Rule 6c-11 in 2019, which allowed ETFs to be created with or redeemed for a customizable subset of the bonds the ETF was tracking, unleashed huge market demand for trading and holding credit ETFs. In other words, rather than needing a fixed basket of individual bonds to create a new ETF share, a customized subset of that list, agreed upon by the issuer and the authorized participant, would now do.

The ETF create-redeem process, in turn, became a new tool for market makers. It helped corporate-bond electronic trading grow as market makers tapped ETFs to support their bond market-making operation, while systematic credit investors grew in number, following the increase in market transparency and access.

In 2018, Cboe launched its first credit future focused on the same index that the largest credit ETFs track (iBoxx iShares $ Investment Grade and High Yield Corporate Bond Indices), grasping onto the fast growth of ETFs as a trading vehicle and leaving behind the past generation’s focus on the swaps market.

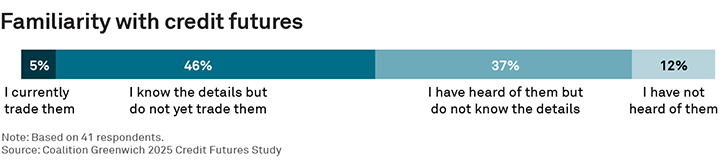

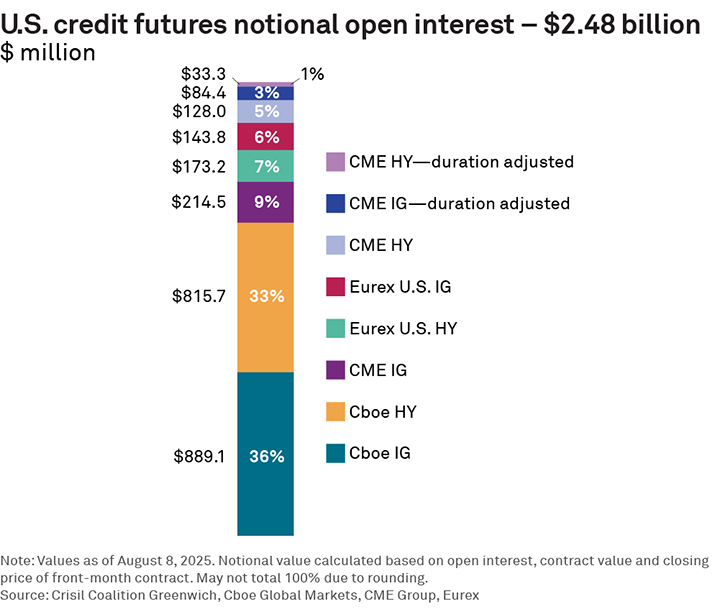

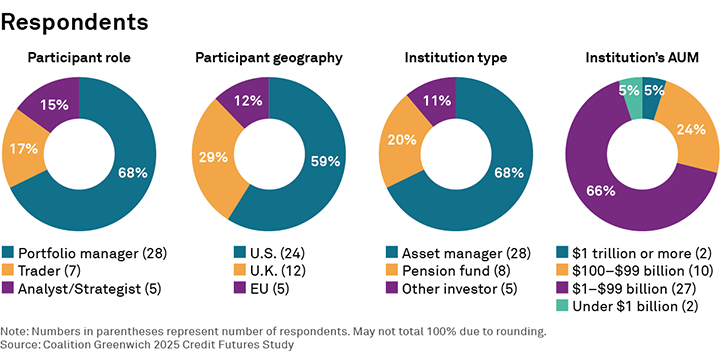

Additional credit futures competition followed post-pandemic, first from Eurex, then CME Group and then ICE, with the new credit-trading market structure reiterating the potential benefits of credit futures for market participants. With 83% of our study participants aware of the products, market-wide open interest of U.S. contracts near $2.5 billion, and positive reviews from early adopters, credit futures growth in the months ahead seems inevitable. This research examines the sentiment, and current and expected future use of credit futures based on responses gathered from 41 credit investors in the U.S., U.K. and Europe.

Why credit futures?

Credit futures offer the same benefits market participants have come to love in futures tracking other asset classes, and some that are unique to credit markets. Unlike bonds and ETFs, some credit futures in the U.S. trade nearly 24 hours a day, five days a week. Using credit futures also comes with built-in leverage and capital efficiency, as margin requirements are considerably lower, at ~2–5%, than the 50% required via Reg T in equity markets (that govern ETF trading). In other words, less capital is required to gain the same exposure you would via ETFs or the bonds themselves.

Futures also offer an easy mechanism to short the bond indices they track, whether to hedge or to speculate— something that remains complex and expensive with other products. Bond ETFs can be sold short, but the cost of borrowing those shares can fluctuate dramatically and may be perceived as prohibitively high in times of market stress. One can technically borrow corporate bonds with a goal toward shorting them as well, but again, the cost and availability of those bonds make this approach unworkable.

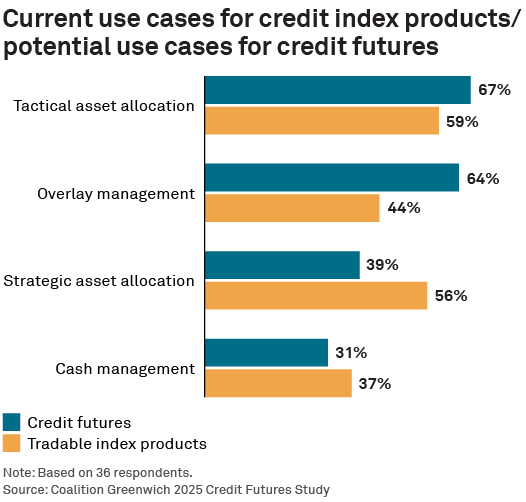

Thinking more holistically and from an investment perspective, our study participants most often mentioned tactical asset allocation and overlay management as strong potential use cases for credit futures. For the former, futures offer an efficient way to quickly adjust overall exposure to the credit market, hedge existing positions or implement views on credit spreads. For instance, if an upcoming market event is expected to widen credit spreads, futures could be used to express that view in a way that would be difficult using bonds themselves. Cash management, mentioned by nearly one-third of our participants, presents a similar use case, with credit futures providing a mechanism to quickly put excess cash to work when sourcing and selecting the bonds needed may take time.

As a tool for overlay management, portfolio managers can adjust credit risk, enhance yield or otherwise optimize a portfolio without having to change their core holdings, all with the inherent benefits of credit futures outlined above.

Roadblocks to adoption

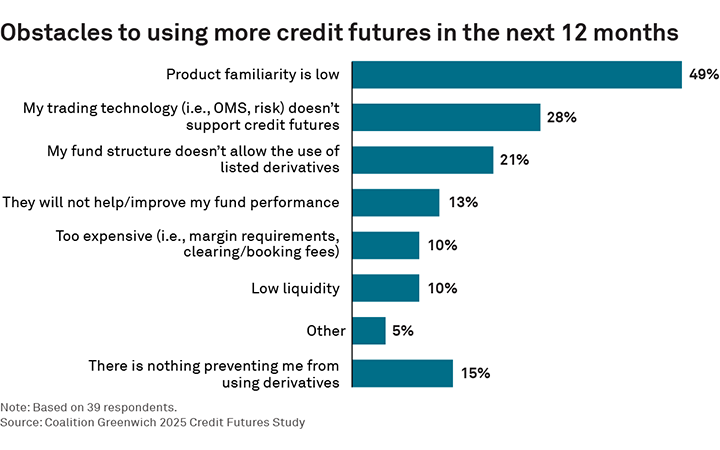

History has proven that widespread adoption of new futures contracts can take time. Futures contracts tracking everything from oil to volatility to the equity market have been launched into a skeptical market only to become a mainstay five or even 10 years later. As demonstrated by nearly half of our research participants who pointed to low product familiarity as the biggest obstacle to credit futures growth, increasing awareness on the trading desk is a critical element to success.

Familiarity also links closely with behavior change. Muscle memory can be hard to alter for portfolio managers who have spent an entire career investing only with bonds or using solely ETFs for overlay management. In that same vein, some of our participants believe that futures will not improve fund performance and/or are too expensive, emphasizing the need to model potential outcomes when futures are in the mix and then measure actual outcomes. Data that demonstrates the benefits of changing behavior is often what moves the needle. Tried and true is a common approach in investing, but standing out often requires doing something new.

Trading-technology support for credit futures ranked a distant second, which speaks to the near ubiquity of futures functionality in modern fixed-income order management systems. It is, however, possible that those currently trading and investing in only corporate bonds would not have futures trading functionality enabled or available, a technology challenge that is somewhat easy to remedy, depending on the OMS provider, via user-interface enhancements and new exchange connectivity.

Downstream processing and risk management can also require upgrades and education on the buy side. While neither the futures workflow nor the modeling of credit risk is new for most institutional investors, the combination of those two elements might be. The advent of swap futures over a decade ago caused similar operational concerns that were ultimately surmounted but required time and focus.

Liquidity concerns were only raised by 10% of our investor participants, a positive sign. Investors often note that it’s not about their ability to get into a position, but to get out when the time comes. So, while credit futures volume and open interest remain in a growth phase, the existence of brand-name market makers and the robustness of the underlying credit market have mitigated liquidity concerns that often plague new contracts.

An expanding ecosystem

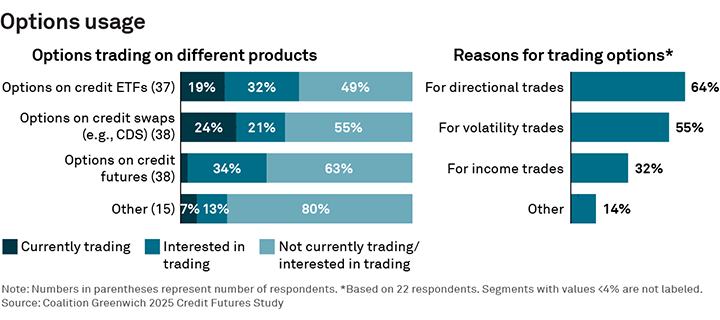

The growing adoption of credit futures presents opportunities beyond the direct use cases we’ve presented thus far. Options trading in the credit market has grown notably in the past several years, as traders and portfolio managers look to speculate (directional trades), generate income and manage what has felt like constant market volatility.

While options on credit futures are barely in their infancy, they were cited as the credit-options product investors are most interested in trading. Swaptions (options on CDS) were most heavily used, which is not surprising, given our study participants are institutional investors, followed by options on ETFs, which now play a large role in implementing bond strategies. But the opportunity for credit futures stands out. Swaptions are traded OTC and, as such, need counterparty-specific documentation, and options on ETFs come with higher margin requirements and smaller trade sizes. Options on credit futures could prove to be a happy middle ground, offering both institutional exposure and the ease of exchange trading.

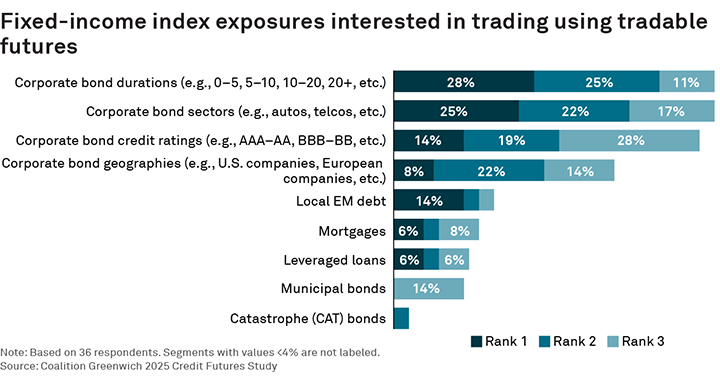

Opportunities also exist to expand the current suite of credit-futures products beyond their current broad investmentgrade, high-yield and emerging-market (EM) debt focus. Investors expressed interest in finer slices, whether for products focused on specific durations, sectors, credit ratings, or regions. An expansion into more narrow indices is already playing out on the ETF market, but credit futures can present more institutionally tailored solutions compared to the retail focus of most ETFs.

Conclusion

The credit market has undergone an incredible transformation over the past 15 years. A market that was once driven by phone calls and closely held prices is now driven by automated executions, systematic investing strategies and data so plentiful that market participants often struggle to make use of it all. This transformation has led not only to a bigger and more liquid market, but a market ecosystem that is considerably more diverse than ever. A more diverse market brings with it more diverse needs.

Previous attempts at credit futures targeted CDS traders and futures-focused firms, neither of whom were ultimately interested enough to help the market grow. The current batch of credit futures targets corporate bond investors, dealers and market makers, with products that track the same indices used in popular ETFs and as portfolio benchmarks. Hindsight being 20/20, the current approach, coupled with today’s market structure, leaves us hopeful that the credit market will finally get the futures product it deserves.

Kevin McPartland is the Head of Research for Market Structure & Technology at Crisil Coalition Greenwich.

2https://www.greenwich.com/market-structure-technology/corporate-bond-dealers-focus-trade-automation

Methodology

Crisil Coalition Greenwich gathered 41 responses from credit investors in the U.S., U.K. and Europe in June 2025. Questions focused on the use of credit derivatives in the investing process, use of credit futures and future demand for credit-focused futures products.

Investors are asking their asset managers to customize service offerings, and in many cases, managers are happy to oblige. Requests for customization create valuable opportunities for managers to differentiate themselves from rivals and deepen client relationships by providing service arrangements tailored to investors’ specific needs.

However, managers moving to take advantage of these opportunities are quickly discovering that customization has some major drawbacks. Namely: Providing customized service propositions to clients is expensive and creates a level of operational complexity that can sap organizations of efficiency.

Today, customization creep represents a real risk to asset management bottom lines. This report can help asset managers navigate this challenge by presenting a detailed breakdown of customization from the perspective of asset management clients. We examine how demand for customized service is evolving among investors around the world and pinpoint exactly what customized features and services they value most. Next, we analyze current satisfaction rates among investors to determine how well asset managers are doing at meeting client demands and where managers can find the best opportunities to differentiate themselves through customization.

Our goal is to help asset managers meet client needs at the lowest possible cost and maximize ROI on customization investments.

Quantifying demand for customization

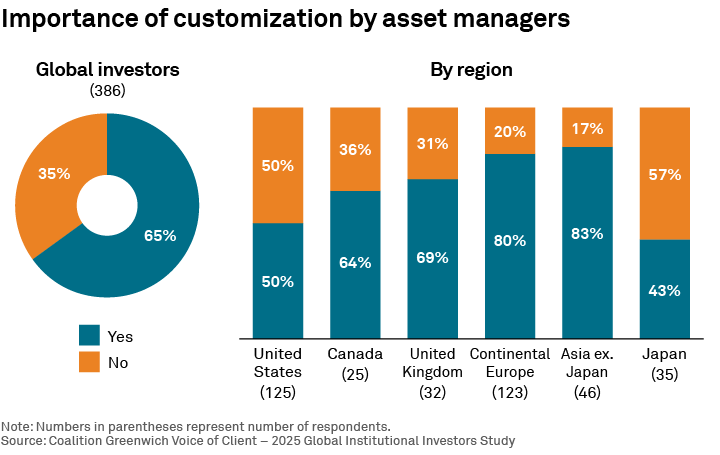

Roughly two-thirds of institutional investors around the world say customization is an important aspect of their relationships with asset managers. That share is highest in continental Europe and Asia, where the proportion of institutions rating customization as important tops 80%. It is lowest in the United States, at 50%, and in Japan, at 43%.

The importance of customization varies considerably among different types of institutions. For example, 9 out of 10 insurance companies view customization as an important element of their relationships with asset managers—a share that likely reflects their complex balance sheets and liability structures. At the other end of the spectrum, only slightly more than half of corporate pension funds say customization is important. As one might expect, larger funds are much more likely than smaller funds to prioritize customization.

Assessing the payoff for customization

Asset managers who take on the cost and complexity of customization can reap significant benefits. Globally, half of institutional investors say they award additional mandates to asset managers who provide customized products and service, including two-thirds of Asia-based institutions and three-quarters of institutional investors in Canada. Banks are especially likely to award extra mandates to managers who customize.

Approximately 40% of institutions—and more than half in continental Europe and Canada—say asset managers who provide bespoke or customized offerings are included in all RFPs. Managers who deliver on customization also have a better chance of getting access to senior decision-makers. Finally, some institutions are willing to pay additional fees for bespoke service, including a third of Canadian institutions and closer to 40% of institutions in the U.K. Around the world, the biggest institutions with the most purchasing power are the least likely to express a willingness to pay for customization.

Defining customization

When institutions talk about customization, what exactly do they mean? While there is no shortage of conversation about customization in the industry today, we believe there is far too little talk about precisely which services and products institutions want customized, and what that customization looks like in practical terms. To better define these terms, we asked institutions around the world to name the specific aspects of manager service and product offerings they want customized.

A service model featuring a single point of contact via a dedicated account manager is rated as an important or very important element of manager relationships by nearly 70% of respondents. Next are customized obligations in the investment agreement, such as notification of a change in fund manager. In third place are customized fees and rebates, followed by bespoke types of investment reporting and customized service level agreements (SLAs).

Institutional investors place an extremely high value on customization across the spectrum of obligations, servicing and self-service. Institutions in Asia and continental Europe place special emphasis on customization in investment agreements and SLAs. Globally, insurance companies and public pension funds assign the most value to customized investment agreements, SLAs and operational setup.

In the area of due diligence questionnaires (DDQs) and fees, institutions in continental Europe are especially interested in customized fees and rebates, and institutions in the U.K. assign the highest level of importance to DDQs that incorporate bespoke questions. Around the world, public pension funds place the most emphasis on customized fees and rebates.

Demand for customized reporting and portfolio analytics among U.S. institutions lags demand for bespoke features among institutions in other parts of the world. Insurance companies place the highest value on customization features across reporting and portfolio analytics.

Measuring institutional satisfaction with manager customization

Now that we’ve defined what it is that institutions want in terms of customization from managers, the next logical question is: Are they getting it? On an industry-wide basis, the answer appears to be yes. In a large majority of the service and product categories discussed in this report, upwards of three-quarters of institutions say they are satisfied or very satisfied with the level of customization they receive from managers.

However, there are nuances to those results that can help asset managers make important decisions about where to direct their investment dollars when it comes to building out customization capabilities.

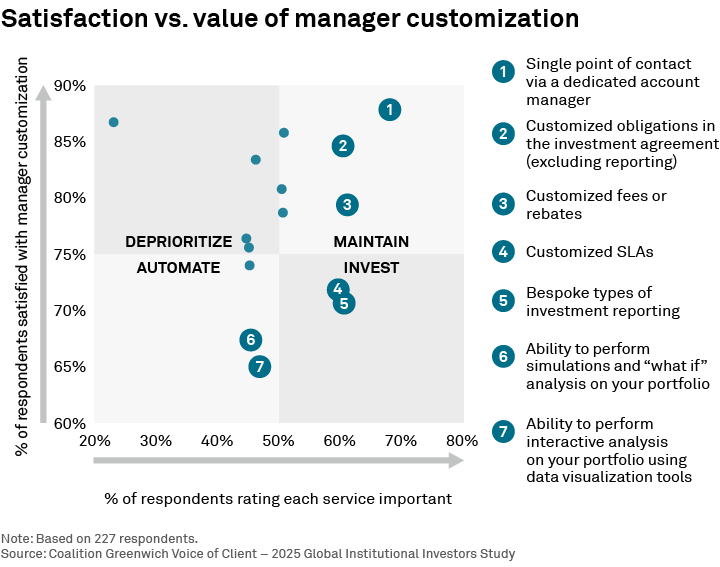

As illustrated in the preceding graphic, we asked study participants about 15 specific services areas to gauge their relative importance and institutions’ satisfaction with the level of customization they are currently receiving from their managers.

From the perspective of institutions, “Maintain” is the optimal range is in the upper right-hand quadrant. Items like a single point of contact and customized obligations in investment agreements rank high in both importance and satisfaction, meaning the customization feature is highly valued by the institution and well delivered by the institution’s managers.

Asset managers might be more interested in items that appear in and near the bottom-right “Invest” quadrant, which depicts customization features for which institutional demand is high, but a sizable share of institutions think managers are falling short in meeting their expectations. Based on the results presented in the chart, asset managers looking to pinpoint the areas in which they could generate the highest levels of ROI on customization-related investments should focus on bespoke investment reporting, interactive portfolio analytics, and customized SLAs.

At the other end of the spectrum, some offerings that might seem worthwhile probably won’t deliver much bang for the buck. For example, managers are doing a good job providing 24/7 support facilities, but institutions do not assign much value to that level of access and support.

A workable framework for customization

Managers face two main challenges when it comes to customization. First, the features most prized by institutions are often also the hardest and most expensive to deliver at scale. Second, the number and scope of customization requests from clients in aggregate have the potential to bog down manager operations, adding complexity, increasing costs and draining efficiency.

For those reasons, managers today must be prepared to push back and draw a hard line against customization initiatives that don’t make sense. Managers must acknowledge that clients will accept almost any additional service as part of their investment mandate, even if it doesn’t provide any real value. In the end, both managers and clients lose if resources are being misallocated to unnecessary services. To avoid that situation, managers need to take a wider perspective, get closer to clients to better understand specific needs, and—most importantly—dare to tell clients, “No.”

To assist managers in developing this type of workable strategy, we present the following customization framework designed to help managers make practical decisions about the costs and benefits of potential customization projects and start building an operational foundation capable of delivering cost-effective customization to clients at scale:

- Establish tiering standards. Clients should be tiered by specific needs, potential wallet or other metrics that matter to the manager, and the scope of services offered to each tier should reflect their relative importance. Critical to this element is the internal enforcement of standards, or in simpler terms, keeping salespeople honest.

- Offer a menu. Managers should develop a set of specific services in which they offer a distinct advantage over other competitors. These services, which must be reflective of the client’s tier, should be offered to new clients as part of the onboarding process.

- Set a cadence. Knowing that clients will likely oversubscribe to their tier-specific services, the manager should establish regular coaching touchpoints with the client to ensure that they are getting the most out of the overall services agreement.

- Trim the offering. The manager’s ultimate goal should be to improve the clients’ overall level of satisfaction while reducing the number of specific services required, giving clients exactly what they need and saving the manager unnecessary costs.

- Invest in technology. Despite the upfront investment, client service technologies such as client portals, APIs and, most pressingly, artificial intelligence, enable managers to deliver and customize service at scale. Leveraging a flexible, user-friendly data platform driven by AI will empower clients to self-serve, permit more transparent, secure transfer of information between clients and managers, and facilitate the provision of customized service, reporting and analytics to clients around the world.

Christopher Dunn, Head of Investment Management—Europe, and Marlie Vredenburgh, Senior Relationship Manager, advise our investment management clients in Europe and North America.