Electronification and Market Access Drive Alpha in Asian Bond Markets

Share

Share

Executive Summary

Portfolio managers aren't the only ones generating alpha. While trading was once only a necessary cost for implementing an investment strategy, trading desks today with the right market access, platform technology and data-routinely act as alpha contributors, as they strive to beat execution expectations.

While this is true in many markets around the world, the gap between reality and opportunity is noticeably wider in Asian bond markets. Although electronic trading adoption and market transparency have increased in the last decade, market norms grounded in local culture and traditional relationships, and diverse, varied regulatory regimes continue to leave global bond investors yearning for the more structured, electronic markets of Europe and the United States.

Progress in electronification is apparent, but the roadblocks to significant change cannot be underestimated. Changing cultural norms is often harder than changing the technology itself. Relationships are still critical when trading bonds, and so fears that e-trading will disrupt those long-held partnerships leave many in Asia nervous. And on both buy and sell side, many are as yet unconvinced by the cost-benefit analysis of e-trading even while execution cost-savings in the U.S. and most of Europe continue to rise as data and technology improve.

For Asian bond markets to truly realize their potential on the global stage, these roadblocks must be overcome. Increasing the adoption of e-trading is not just about easing the burden on traders or helping investment funds generate more alpha. E-trading almost always brings with it greater price transparency, which then results in improved liquidity and improved liquidity can lead to greater demand for those bonds. Greater demand for bonds means lower borrowing costs for the companies and countries borrowing to drive the entire economy forward.

We are not suggesting e-trading is a main driver of broad economic growth, of course, but evidence suggests that e-trading helps create more efficient capital markets that ultimately allow the world to grow and improve.

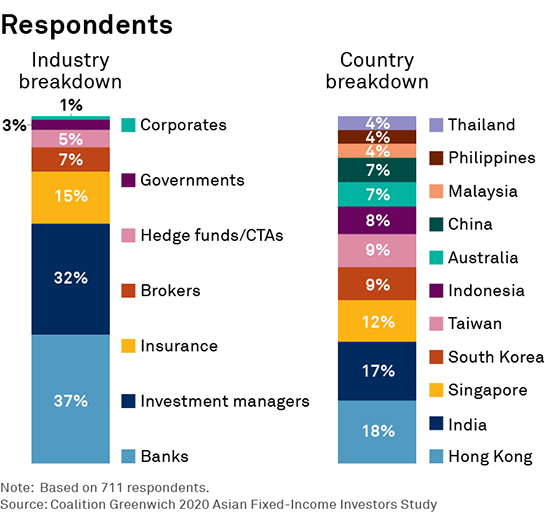

This research, based on interviews with 700 Asian bond investors trading over $2 trillion of domestic- and hardcurrency bonds in 2020, examines the current state of fixed-income e-trading in Asia, roadblocks to progress and areas for growth in the coming years.

Methodology

This research is based on interviews with 700 Asia-based fixed-income investors in late 2020, and conversations with Asia-based dealers and platform providers in 2Q 2021. Topics included dealer relationships, trading volumes, electronic trading adoption, and market structure changes.

Executive Summary

Portfolio managers aren’t the only ones generating alpha. While trading was once only a necessary cost for implementing an investment strategy, trading desks today—with the right market access, platform technology and data—routinely act as alpha contributors, as they strive to beat execution expectations.

While this is true in many markets around the world, the gap between reality and opportunity is noticeably wider in Asian bond markets. Although electronic trading adoption and market transparency have increased in the last decade, market norms grounded in local culture and traditional relationships, and diverse, varied regulatory regimes continue to leave global bond investors yearning for the more structured, electronic markets of Europe and the United States.

Progress in electronification is apparent, but the roadblocks to significant change cannot be underestimated. Changing cultural norms is often harder than changing the technology itself. Relationships are still critical when trading bonds, and so fears that e-trading will disrupt those long-held partnerships leave many in Asia nervous. And on both buy and sell side, many are as yet unconvinced by the cost-benefit analysis of e-trading—even while execution cost-savings in the U.S. and most of Europe continue to rise as data and technology improve.

For Asian bond markets to truly realize their potential on the global stage, these roadblocks must be overcome. Increasing the adoption of e-trading is not just about easing the burden on traders or helping investment funds generate more alpha. E-trading almost always brings with it greater price transparency, which then results in improved liquidity—and improved liquidity can lead to greater demand for those bonds. Greater demand for bonds means lower borrowing costs for the companies and countries borrowing to drive the entire economy forward.

We are not suggesting e-trading is a main driver of broad economic growth, of course, but evidence suggests that e-trading helps create more efficient capital markets that ultimately allow the world to grow and improve.

This research, based on interviews with 700 Asian bond investors trading over $2 trillion of domestic- and hard-currency bonds in 2020, examines the current state of fixed-income e-trading in Asia, roadblocks to progress and areas for growth in the coming years.

E-Trading Adoption: Chasing the U.S. and Europe

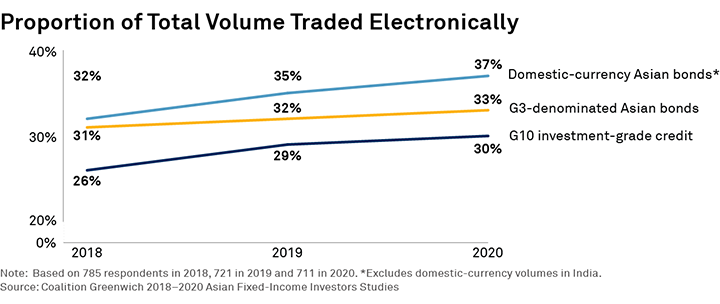

The past four years have brought a notable uptick in e-trading of domestic-currency, G10 investment-grade and hardcurrency credit in Asia, with domestic-currency bonds leading the way. In 2016, Coalition Greenwich data showed1 that 14% of Asian fixed income (including domestic- and hard-currency bonds) traded by the buy side were executed electronically. At the end of 2020, our data showed that buy-side e-trading roughly doubled, with approximately 26% of Asian fixed-income volumes traded electronically via platforms such as Bloomberg, MarketAxess and Tradeweb, including 37% of domestic-currency bonds. The latter data point demonstrates that e-trading growth in Asia is not simply from international firms trading G3 bonds, but is increasingly being driven locally.

The buy side has upped its e-trading adoption in recent years. E-trading venues have worked hard to make this happen, bringing better liquidity, improved functionality and protocol diversity, and enhanced market-data solutions to market. Volumes traded across those platforms have increased as a result. For instance, MarketAxess saw its volumes in the region grow since at least 2018, with a 40% year-over-year increase in volume in 2021—a record year for the firm. And according to data in Greenwich MarketView, Tradeweb’s volume in Chinese bonds was up 58% in the first six months of 2021 compared to the first half of 2020, reflecting growth in e-trading amid overall demand for Chinese debt.

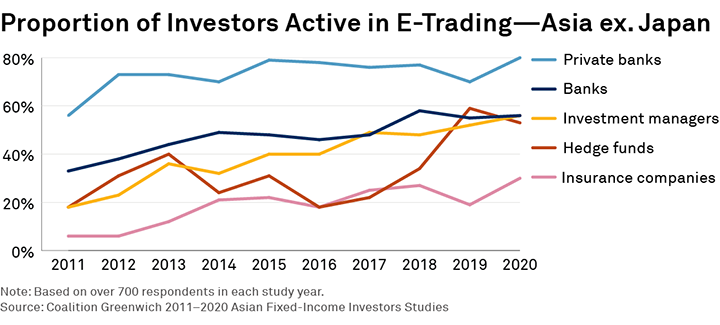

E-trading adoption cuts across investment strategies and firm types, too. Hedge fund traders based in Asia have shown the most dramatic growth over the past four years. While only 18% of the Asia-based hedge funds involved in our research in 2016 traded at least some of their fixed income electronically, in 2020, more than half of those hedge funds did, putting them in line with asset managers and commercial banks.

Investment managers have also shown steady e-trading adoption in the same period. Finally, we note that private banks, ETF market makers and, most notably, dealers are increasing their use of electronic platforms. The proportion of dealers taking on liquidity via request-for-quotes (RFQs) on the MarketAxess platform was already up over 100% year over year in September 2021.

There are a number of factors at play in this growth. First, the digitization of fixed-income markets in Europe and the U.S. has driven global liquidity providers and investors to look for the same market structure in Asia. In addition to the 50% and 40% of investment-grade corporate-bond volumes traded electronically in Europe2 and the U.S.,3 respectively, those markets have seen data availability and transparency surge. This has, in turn, increased the possibility of automation and price improvement via better pre- and post-trade analytics. Bloomberg, MarketAxess and Tradeweb all offer automation tools and real-time pricing services that have gained traction in the U.S. and, increasingly, in Europe. Asian fixed-income investors are more and more demanding those same tools and benefits.

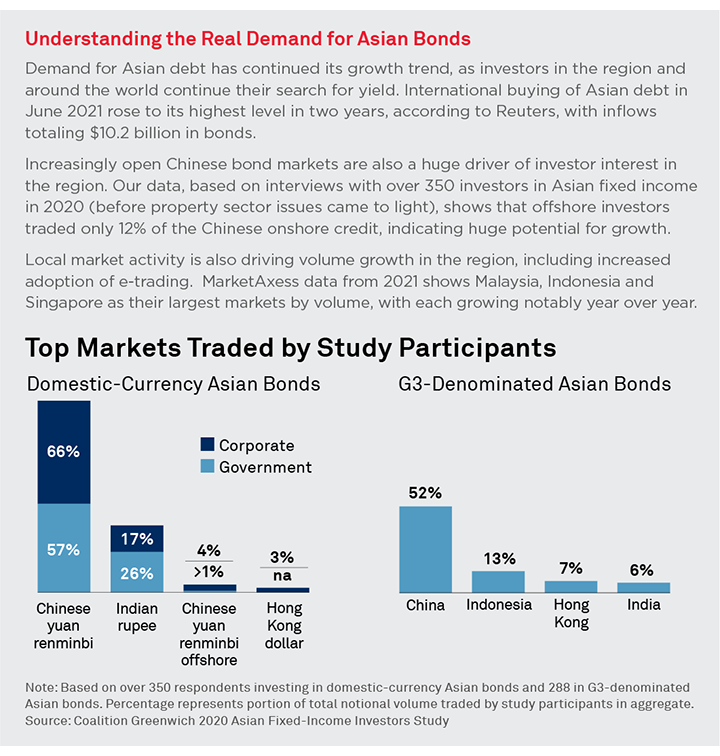

Second, increased e-trading in some of the region’s largest markets has driven some smaller markets to get onboard. While e-trading in the region as a whole accounts for roughly 26% of total volume, our data shows that roughly 80% of domestic-currency bond volume traded by Chinese and Hong Kong investors participating in our study was executed via electronic channels in 2020, helped by the popular Bond Connect program, which is hugely impacting average e-trading levels Asia-wide. Singapore and India, while less electronic than China, have also seen notable jumps in e-trading adoption, with nearly 40% of volume in the former and nearly 50% in the latter executed electronically.

It’s also important to remember that average usage statistics don’t tell the whole story. Larger and more tech-forward investment firms are executing increasingly larger block trades electronically, a sign of improving electronic liquidity that smaller firms are not taking full advantage of.

And lastly, we can’t ignore the pandemic’s impact on digitization worldwide. Our conversations with market participants tell us that there is a real correlation between the increase in remote work and the increase in e-trading around the world and in Asia specifically. Calling multiple dealers from home rather than a trading turret in the office is notably less efficient, and that inefficiency, in many cases, was enough of a catalyst to drive significant behavior change—a change we do not believe will reverse as offices reopen.

Progress via Innovation

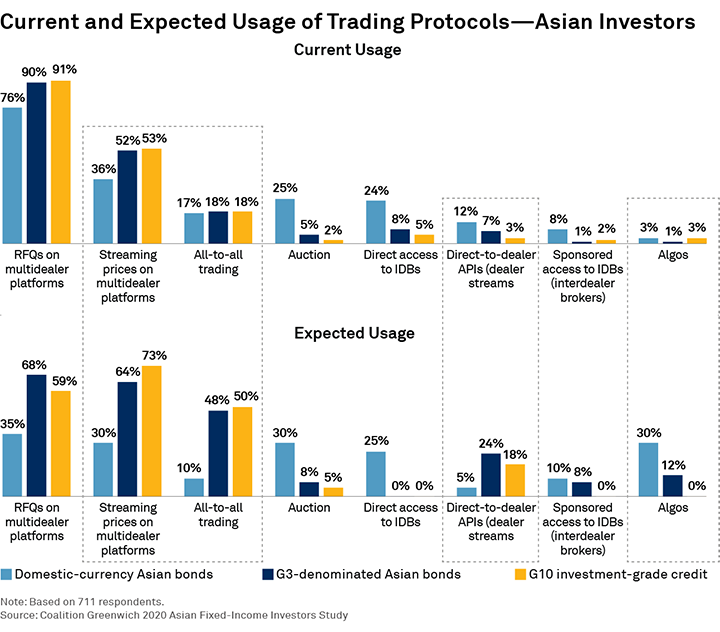

The growth of fixed-income e-trading globally has come not only from increased participation, but also from protocol innovation. Our data suggests that if the market remained driven purely by name-disclosed RFQ, the percentage of volume traded electronically would be considerably lower than it is today.

For instance, all-to-all trading protocols, such as anonymous RFQ and some auction-style offerings, have allowed the buy side to provide liquidity and, conversely, dealers to send RFQs, neither of which would have been possible a decade ago. This speaks to a global trend in corporate-bond trading4 over the past year that has seen an uptick in dealer-to-dealer e-trading, supported by new trading protocols offered by both the traditional dealer-to-client platforms and some interdealer brokers.

Both dealer-initiated RFQs via MarketAxess Open Trading in global markets and trading volumes via Tradeweb Dealer Sweep in the U.S. continue to grow. Further, improvements in real-time bond-pricing algorithms have allowed dealers to stream prices to customers, whether in response to a request-for-stream (RFS) or continuously throughout the day.

Today, trading via RFQ on multidealer platforms, such as Bloomberg, China Foreign Exchange Trade System (CFETS), MarketAxess, and Tradeweb, is the dominant method of e-trading, particularly in G3 and G10 bonds. Streaming prices via these same platforms is also common. Looking forward, investors are expected to more greatly utilize streaming prices—primarily via multidealer platforms, but also from dealers via API for some and, more notably, all-to-all trading. This change in behavior is more targeted toward G3 and G10 bonds for now, but we believe localcurrency bonds will see similar changes in subsequent years.

This move forward can provide huge efficiencies for liquidity providers as well. Not only will it reduce the manual nature of trading via phone, but it will further automate the RFQ process that can still require senior sales and trading professionals to ensure the right client is seeing the right price. Automation will allow the current trading desk to handle more volume without sacrificing client service.

The potential savings here, on both the buy and sell side, should not be underestimated: Across much of Asia-Pacific, voice trading is still the dominant method, with large numbers of salespeople and associated (inefficient) infrastructure built around it. Smarter use of technology and people is needed.

For instance, Coalition Greenwich research in 2Q 20215 showed that executing at mid via all-to-all markets could save the buy side $6 million per day in U.S. corporate-bond markets, leveraging their ability to act as a liquidity maker. That same research also noted that bond dealers were increasingly acting as liquidity takers and, in doing so, improving their ability to manage their risk and balance sheet usage more effectively. In Asia, where dealers are already accustomed to acting as price takers in interdealer markets, we see the opportunity for this behavior to grow even more quickly.

Portfolio trading, offered by nearly every major trading venue, presents another opportunity for growth. Our data shows that 16% of Asian asset managers and hedge funds executed a portfolio trade in 2020, a number that is almost inevitably going to grow in the next two to three years as the operational and compliance challenges6 are resolved. And while only 5% of Asian institutional investors told us they traded ETFs in 2020, growing use of ETFs worldwide is also findings its way into Asian fixed income, which should act as another portfolio-trading catalyst, given the tight linkage between the two trends.

Opportunities for Further Electronification

Despite clear electronification progress over the past several years, there remains much more opportunity for growth and increased efficiency beyond the growth of all-to-all and portfolio trading. Many dealers still have people quoting prices on liquid bonds in G10 currencies, a process that really should no longer need human intervention.

Interestingly, both the largest and smallest economies present some of the greatest opportunities for e-trading venues and the market participants that thrive in an electronic environment. On one end, China is now one of the largest economies in the world, with an increasingly accessible bond market to match. China’s corporate-bond market was worth $9.4 trillion as of 2Q 2021, according to S&P Global, rivaling the corporate-bond market in the U.S. The Bond Connect program and CIBM Direct, which links global investors to the China Interbank Bond Market, have allowed record numbers of international investors to pour in, with international buying hitting, in the case of the former, its highest level ever in July 2021.

Offshore investors trade in this market today via Bloomberg, MarketAxess or Tradeweb, which then connects to local market makers via CFETS. Average daily volume via Bond Connect in October 2021 was up 63% from the previous year,7 with the trading venues seeing similar growth in volumes.8

Increased demand for Chinese bonds also comes from within, where a rise in local dealer participation is likely to bring in more local clients. This demand has created a virtuous cycle: Improved market access has driven the largest index providers to include Chinese bonds in their major indexes, which, in turn, has driven more interest and trading.

Conversely, opportunity for e-trading growth also exists in more local, emerging markets. While a search for yield is driving interest from global investors, historically the markets’ smaller sizes and local market participants that rely heavily on relationships have acted until recently as a deterrent to electronification. This is changing. MarketAxess data shows that their trading volume for local markets in 3Q 2021 grew 135% from the same period three years earlier.

While many emerging markets will never reach the level of transparency and electronification seen in more-developed parts of the world, the tools and data available via the major trading venue providers today, such as all-to-all trading, mean that local market participants with limited internal infrastructure can still gain quick access to the liquidity and transparency of electronic markets. The information edge electronification provides could then be enough to drive more widespread adoption.

More Data, More Metrics and More Portfolio Managers

Improving price transparency in both developed and emerging markets in Asia will go a long way toward encouraging increased participation both domestically and internationally. History has shown that e-trading and price transparency also go hand in hand, with better data making more e-trading possible, which then creates more data and so on. In Asian fixed-income markets, we see two main drivers of change in this regard.

First, traders tend to adopt only those tools that show they can provide real price improvement over time. This means better transaction cost analysis (TCA) is an important part of the electronification of Asian bond markets. While developed markets in Europe and the U.S. are further along in this regard, fixed-income TCA continues to make great progress.

While data access remains fragmented depending on who you are (i.e., buy side, sell side or trading venue) and determining the benchmark price for a given bond at a given time is often as much art as science, trading venues have made great strides in solving these challenges. This progress is critical to e-trading broadly. If buy-side traders of Chinese or Malaysian bonds (or any bonds for that matter) can better measure the results of their execution channel of choice, the more likely they are to make changes in search of the best possible outcome.

Second, it is important to get portfolio managers (PMs) more involved in the execution process. PMs overseeing Asian investment strategies aren’t always based in the region, even when the trading desk is local, which can create a gap between what is ideal and what is realistic with regard to execution expectations. Furthermore, PMs have a unique, vested interest in saving basis points via improved executions. Those savings go straight into fund returns, the primary metric by which PMs are measured. As such, the more access PMs have to the same data and tools as the local trading desk, the more aligned they can all be on the go-to-market strategy.

In addition, all-to-all trading remains in its infancy in Asia, in part because trading desks at real-money asset managers need PM support to “make” a price on a given bond. And to take the conversation full circle, both PMs and traders then need analytics to show how successful trading via all-to-all or other electronic channels has actually been. It is these metrics that will then drive real change over time.

Roadblocks to Change

If data access were the only roadblock to increased e-trading and workflow changes more broadly, it is likely the market would already be further along the innovation curve. As market-structure watchers know, putting the “right” or “best” technology in place is rarely enough to drive long-term behavior changes.

Cultural change on the trading desk is, in fact, more complicated than even the most complex new technology. As we’ve discussed in our research countless times in the past, habits are hard to change and bilateral relationships between firms and individuals act as the lifeblood for the market as whole. This is particularly true in many insular Asian markets, where local relationships are required, even if not by regulatory mandate. As such, many still see the move to e-trading as a breaking down of decades-old relationships that could hurt their business more than it would help.

The buy side worries they won’t receive the same level of services from their trading counterparties if communication between firms decreases, and many sell-side traders fear their profit margins will get squeezed or the newfound trading automation will put them out of work. Yet, the facts to date don’t bear out those fears.

The past several years have proven that those first to adapt to the new market structure are ultimately the biggest beneficiaries of the change. And while e-trading adoption certainly changes the nature of some relationships, the mechanisms in place today are designed to keep relationships intact, while still improving liquidity access. Importantly, even in anonymous all-to-all markets, dealers have benefited as much by taking liquidity as providing it.

The explicit costs of trading electronically can also act as a roadblock, but ultimately, the opportunity costs of not participating in electronic markets have proven much higher. Compensation structures are also at work here, with many dealers still paying salespeople a greater commission for voice trades than for those traded electronically—a clear disincentive to change, despite senior-management focus on cost reductions and the efficiency improvements that come from a more electronic end-to-end workflow. We believe new platform pricing models and sales incentives will emerge over time, acting as a further nudge toward e-trading adoption in Asian markets.

Lastly, e-trading in Asia can’t be tackled as a single problem with a single solution. There are officially 48 countries in Asia, each with its own regulations, local economic needs, borrowing dynamics, compliance requirements, investors, liquidity providers, information-leakage challenges, and cultural norms. This means that trading solutions must be built with standards that allow a common view across the region and with features unique to each market, its rules and unique ways of transacting—no small feat. That said, by focusing on the largest markets first, such as China, Hong Kong, India, and Singapore, considerable progress can be made that might ultimately create new standards that help smaller markets follow the same innovation curve.

Real Demand Makes Progress Inevitable

It is important to remember that e-trading growth is not simply about easing the burden on traders, many of whom are now handling more products and volume than ever before. E-trading almost always brings with it more price transparency, which then results in improved liquidity, which, in turn, can lead to greater demand for those bonds.

Greater demand for bonds means lower borrowing costs for the companies and countries borrowing to drive the entire economy forward. We are not suggesting e-trading is a main driver of broad economic growth, of course, but evidence suggests that e-trading does help create a more efficient capital market, which ultimately allows the world to grow and improve.

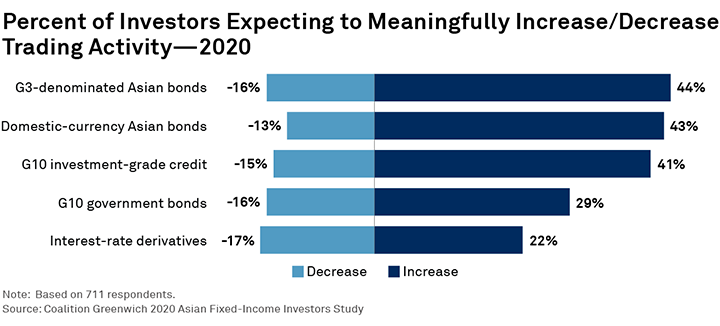

Our data shows that Asian fixed-income investors expect to increase their trading activity in the region going forward, particularly in G3, G10 and domestic-currency bonds. The search for yield globally and growing prominence of many Asian bond markets in global indices both play a part. We expect e-trading adoption to pick up speed, particularly for asset managers, hedge funds and private banks, as many of these firms are increasingly taking a global approach to investment-process standards that include e-trading and automation.

Increasing price and broader market transparency is no small feat, but certainly an effort that many trading platforms and other data providers will focus on going forward. And as data availability increases, we also expect trading-protocol usage to diversify as it has in the West, in particular with all-to-all trading picking up steam in the coming years. Fixed-income markets differ by region and country for many reasons, but going forward, technology should increasingly make these markets more transparent and accessible to all.

Kevin McPartland is the Head of Research for Market Structure and Technology. Parijat Banerjee heads our client advisory for global markets and investment management in Asia-Pacific. Vignesh Srinivasan is a research associate covering Asia-Pacific markets.

1https://www.greenwich.com/fixed-income/asian-fixed-income-e-trading

2https://www.greenwich.com/fixed-income/european-bond-trading-innovation

3https://www.greenwich.com/fixed-income/all-all-trading-takes-hold-corporate-bonds

4https://www.greenwich.com/market-structure-technology/may-spotlight-interdealer-e-trading-finally-getting-attention

5https://www.greenwich.com/fixed-income/all-all-trading-takes-hold-corporate-bonds

6https://www.greenwich.com/fixed-income/making-case-portfolio-trading

7https://www.chinabondconnect.com/en/Data/Flash-Report/Continuous-Influx-Of-Bond-Connect-Investors-And-Activities-Amid-Ftse-Wgbi-Inclusion.html

8https://www.chinabondconnect.com/en/Data/Flash-Report/Bond-Connect-Witnesses-Considerable-Year-On-Year-Growth-In-Trading-In-August.html

Methodology

This research is based on interviews with 700 Asia-based fixed-income investors in late 2020, and conversations with Asia-based dealers and platform providers in 2Q 2021. Topics included dealer relationships, trading volumes, electronic trading adoption, and market structure changes.