The Evolution of Global Bond Trading in Japan

Share

Share

Executive Summary

Global demand for fixed income assets has surged in recent years as yields have increased amidst efforts to dampen inflation in major markets globally. Japanese investors in particular have sought out government and corporate bonds from developed and emerging markets that offer higher yields than can be found at home with little or no additional risk. This demand has increased trading volumes across most fixed income products, leaving investment managers in search of solutions to manage both the volumes and the data necessary to find the liquidity they need. While human intelligence and relationships remain central to the functioning of fixed income markets in Japan and around the world, technology is augmenting investors and traders as they grapple with this new demand. Electronic trading tools are playing a major role in helping investors manage these new market challenges. While e-trading in Japan lags other developed markets, our research has found that adoption in Japan and in Asia more broadly is growing as local investors seek out liquidity in both local and foreign markets. And while the market dynamics of each country and bond can vary widely, bond-trading venues have developed a variety of trading protocols that allow trading of nearly all bonds, from the most liquid to the least and everything in between. Based on interviews with investors in Japan and Asia in the fourth quarter of 2023, this research examines the evolution of fixed income market structure in Japan, how technology is adding efficiency to the trading workflow, the growing role of electronic trading, tailwinds and headwinds impacting e-trading growth, and the opportunities available to Japanese fixed income investors via the electronic trading ecosystem.

Methodology

Coalition Greenwich interviewed over 500 buy-side fixed income investors in Asia in the fourth quarter of 2023. The study was conducted over the phone, online and in-person. Respondents answered a series of qualitative and quantitative questions focused on their dealer relationships, market expectations and use of electronic trading tools.

Executive Summary

Global demand for fixed income assets has surged in recent years as yields have increased amidst efforts to dampen inflation in major markets globally. Japanese investors in particular have sought out government and corporate bonds from developed and emerging markets (EM) that offer higher yields than can be found at home with little or no additional risk. This demand has increased trading volumes across most fixed income products, leaving investment managers in search of solutions to manage both the volumes and the data necessary to find the liquidity they need.

While human intelligence and relationships remain central to the functioning of fixed income markets in Japan and around the world, technology is augmenting investors and traders as they grapple with this new demand. Electronic trading tools are playing a major role in helping investors manage these new market challenges. While e-trading in Japan lags other developed markets, our research has found that adoption in Japan and in Asia more broadly is growing as local investors seek out liquidity in both local and foreign markets. And while the market dynamics of each country and bond can vary widely, bond-trading venues have developed a variety of trading protocols that allow trading of nearly all bonds, from the most liquid to the least and everything in between.

Based on interviews with investors in Japan and Asia in the fourth quarter of 2023, this research examines the evolution of fixed income market structure in Japan, how technology is adding efficiency to the trading workflow, the growing role of electronic trading, tailwinds and headwinds impacting e-trading growth, and the opportunities available to Japanese fixed income investors via the electronic trading ecosystem.

Introduction

Electronic trading is no longer aspirational for global bond markets. The last decade has seen fixed income trading around the world transform from a phone/chat-based network into a sophisticated electronic ecosystem allowing buyers and sellers to interact in ways that, until recently, didn’t seem possible. The request for quote (RFQ) process—the ability to send a firm price request to a list of market makers, receive executable prices, execute with the chosen dealer, and have the trade automatically booked—is increasingly automated. The concept of all-to-all trading, which enables all market participants to trade directly with one another, is fully accepted by investors and dealers alike. Portfolio trading (executing a basket of bonds at a single price), which was once only used by the largest and most sophisticated investors, is now universally accessible and electronic. Last but not least, dealers can now provide automatic price quotes across multiple sectors of the fixed income market, with 100% of U.S. bond dealers in our recent study able to auto-quote investment-grade bonds.

The pace of growth and the nature of e-trading varies from region to region. According to Coalition Greenwich data, in 2023, 42% of U.S. investment-grade bonds traded electronically (on a notional basis), as did 30% of U.S. high-yield bonds and 64% of U.S. Treasury bonds. Across the Atlantic, 63% of European investment-grade bonds and 75% of European government bonds traded electronically in 2023. While European markets are more electronic on a relative basis, the U.S. market stands out given the sheer size of the market and a greater willingness of market participants to execute via new methods (i.e., real-time continuously updated streaming prices, all-to-all, etc.).

Asian fixed income investors broadly have taken notice. Coalition Greenwich interviews with the buy side show that 56% of Asian investors utilized e-trading in 2023, compared to only 36% a decade ago. Traders at traditional investment managers based in Asia have shown the most dramatic growth in recent years. While only 36% of the Asia-based asset managers involved in our research in 2013 traded at least some of their fixed income electronically, in 2023, that percentage jumped to 63%.

Electronic trading in the U.S. and Europe has played a big part in Asia’s adoption, while increased e-trading in some of the region’s largest markets is also driving some smaller markets to get onboard. While e-trading in Asia accounts for roughly 26% of total volume, our data shows that roughly 80% of domestic-currency bond volume traded by Chinese and Hong Kong investors participating in our study was executed via electronic channels in 2020 (the most recent data), helped by the popular Bond Connect program, which is hugely impacting average e-trading levels Asia-wide. Singapore and India, while less electronic than China, have also seen notable jumps in e-trading adoption, with an average of 65% of volume executed electronically across both.

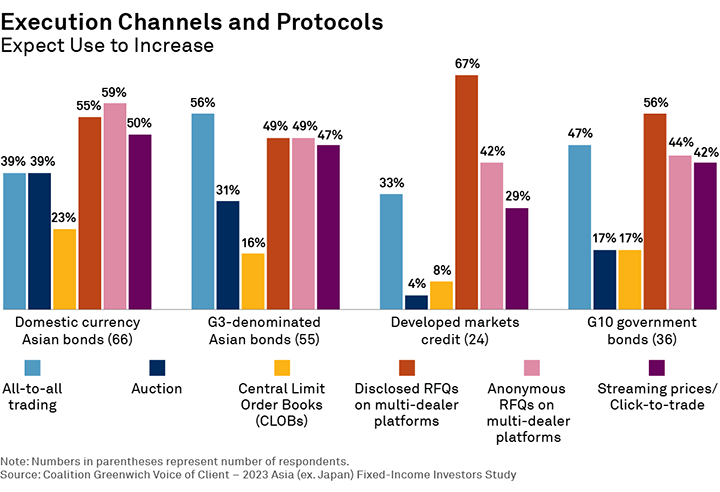

Looking ahead, Asian fixed income investors are already planning to increase their usage of e-trading across product categories and trading protocols. While more than half expect to increase trading via traditional disclosed RFQ in the coming year, it is notable that trading via all-to-all and anonymous RFQ is also expected to grow, particularly for G3 Asian bonds (those issued by Asian sovereigns and corporates in USD, EUR and JPY, but predominantly in USD) and G10 government bonds. This acts as a reminder that e-trading is not one-size-fits-all, with solutions now available for the most-liquid bonds, least-liquid bonds and everything in between.

Why E-Trading is Growing

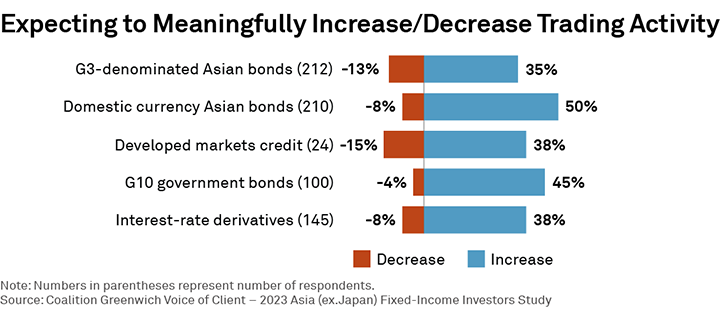

E-trading’s growth is driven in large part by the cost efficiencies, transparency and easy access to liquidity it creates. Investors and dealers are having to handle higher trade volumes, often with the same number or fewer traders. This is particularly important now, given expectations for higher volumes in the year ahead. Half of Coalition Greenwich research participants expected to trade more local currency Asian bonds in the year ahead, 45% more G10 government bonds, 38% more developed-market corporate bonds and 35% more G3-denominated Asia bonds. With Asia-based investment managers averaging only two to four traders per desk across these asset class segments, augmentation via e-trading is the only way to keep up.

Furthermore, execution quality can be more accurately measured and often improves as traders and algorithms have a deeper view of the market. E-trading was once seen as a threat by bond dealers, but it is now widely accepted that the additional distribution capabilities and workflow efficiencies it offers allow trading desks to operate better and, in fact, improve client relationships over time.

Several other powerful factors are driving e-trading’s growth:

OMS integration: The order management system (OMS) is one of the most important tools on the buy-side trader’s desktop. As such, integrating e-trading tools with key OMSs in Japan, such as the solutions offered by BlackRock Solutions, Nomura Research Institute (NRI) and others, can dramatically improve workflows and trading outcomes with order details, compliance requirements, real-time execution data, pricing and liquidity metrics integrated into a single view.

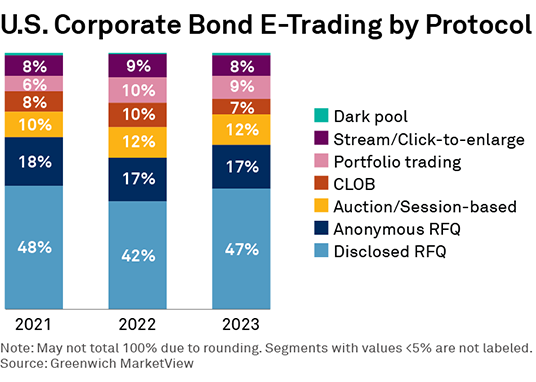

Protocol innovation: E-trading in the bond market has come a long way from its RFQ “automate the phone” roots. Coalition Greenwich measures fixed income e-trading in seven different protocols, all of which offer unique benefits given the trade type, investment goals and/or liquidity needs. Even trading via disclosed RFQ, the most commonly used execution method, has seen tremendous innovation in the past decade.

Request for market (RFM), for instance, which is popular for trading local EM rates products in Japan, requires dealers to provide both a bid and offer price at the client’s request. This reduces information leakage as the requesting client does not need to disclose whether they are a buyer or seller to receive pricing information, and only the winning dealers (rather than all included in the RFM) know whether the trade was a buy or sell.

New approaches are also encouraging more block trading electronically. All-to-all trading solutions, for instance, allow clients to reach out to only a select group of dealers, albeit still anonymously, which further minimizes information leakage to the broader market. This approach is also growing for disclosed trading, with the buy side using data to target the dealers most likely to meet their trading needs.

While the buy side is gaining efficiency through these new tools, there is no sign that this electronification is hurting dealer revenue. In fact, Coalition Greenwich data shows that sell-side revenues for G10 rates trading in Japan grew 66% year over year in 2023, reaching $4.8 billion, while credit trading grew 23% to $1.2 billion.

Opportunity for Japanese Investors

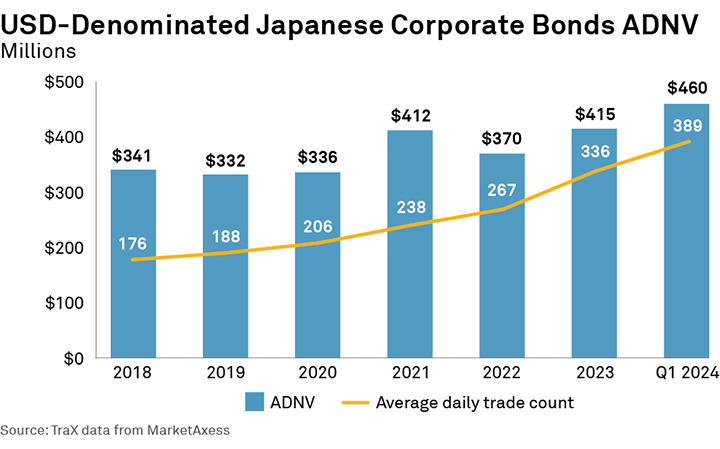

Japanese investors can benefit from these advancements. Japanese investors are the largest holders of U.S. Treasury securities, for instance, with current investments totaling $1.1 trillion at the end of 2023. Coalition Greenwich data shows that globally, 64% of U.S. Treasuries traded electronically in 2023, which provides a strong indication that the best liquidity in that market is on screen and available to global investors. Trading in dollar-denominated Japanese corporate bonds has also grown notably since the onset of the pandemic in 2020, according to MarketAxess data, with the average daily notional volume (ADNV) traded ($460 million) in Q1 2024 up 37% since 2020.

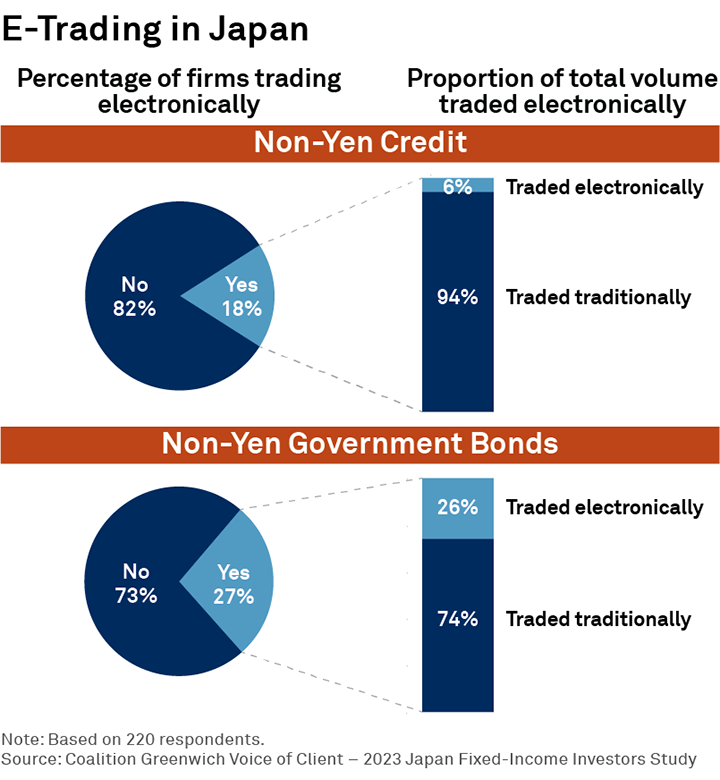

Given this demand, e-trading can provide an edge when implementing a fixed income investing strategy, as widespread adoption in Japan is only just beginning. This is particularly true for those investing in dollar- and euro-denominated bonds. Coalition Greenwich data shows that only 27% of Japanese investors trade non-yen government bonds electronically, with 26% of notional volume executed on the screen (much of which is in U.S. Treasuries).

E-trading in non-yen corporate bonds is much lower, with only 18% utilizing e-trading and only 6% of notional volume traded electronically. However, some of Japan’s largest asset managers are actively trading most of their orders in these bonds electronically, suggesting growth is to come. Among these firms, one is trading half of their volume electronically, two 65–75%, three 80%, and one large Japanese asset manager 100% of their non-yen corporate bond orders electronically. These industry leaders suggest smaller firms will follow their lead over time.

Impediments to Growth

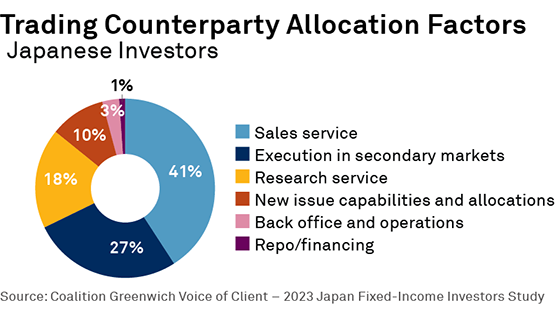

Unlike the U.S. and Europe, where electronic platforms have become a dominant part of the landscape, Japanese bond dealers have been hesitant to fully embrace this shift despite recent progress. This reluctance stems, in part, from a cultural preference for relationship-based trading. Forty-one percent of the flow in Japan credit is allocated based on the sales relationship, compared to 27% that is executed based on execution quality, according to Coalition Greenwich research.

It is important to note that e-trading growth in Europe and the U.S. has not diminished the importance of the dealer relationship in trading. Even in cases when orders are executed by the dealer with no human intervention, the buy-side trader must still feel confident that the responding dealers are providing the best price possible and treating the information included within that order with the utmost care. Ultimately, such technology augmentation leaves both buy-side and sell-side traders to spend more time discussing the market and ideas and less time manually negotiating orders throughout the day.

The cost of onboarding electronic solutions has also slowed buy-side adoption. Most trading venue solutions can be delivered at little or no cost, but the cost of integration (i.e., with an OMS) and compliance can give some investors pause. However, as history has shown us, such cost barriers come down as technology advances, leading to much broader adoption over time. And the execution quality and distribution available via e-trading tools can quickly create a return on investment.

Additional regulatory clarity could also help to move the market forward. While regulatory bodies in the U.S. (SEC), Europe (ESMA) and U.K. (FCA) are actively pursuing policies focused on best execution and transparency, which encourage e-trading, Japan’s regulatory environment continues to discuss the best path forward via engagement with investors, bond dealers and trading venues alike. Further regulatory engagement may help to increase adoption by market participants. Closing this gap with other large global markets will be crucial in fostering a more fertile ground for e-trading to flourish in Japan.

In the meantime, market-driven solutions to increase transparency are helping investors improve outcomes, and ultimately complement any regulator-driven initiatives. Public reporting requirements (e.g., FINRA’s TRACE) in the U.S. certainly aid market transparency, but ultimately, private sector solutions are what have driven e-trading forward. The major trading venues operating in Japan and Asia broadly play a big role here. Most offer real-time evaluated bond pricing, for instance CP+, MarketAxess’ AI-powered pricing engine. Further, the firm operates a post-trade reporting platform, which feeds into TraX, a transaction data solution. TraX takes contributions from bond dealers’ voice and electronic trades and, in turn, offers the market a deeper look at trading activity.

With all that said, by no means does the proliferation of e-trading threaten the importance of the trader or dealer; rather, its operational efficiencies enable them to provide deeper insight into the market and, accordingly, more reliable prices. In other words, e-trading in most markets further encourages healthy competition via the quality of client service and trade-execution capabilities.

Competition Drives Progress

Despite distinct local markets around the world, the bond market has globalized along with other parts of the economy, which means competition comes not only from Japan but from firms around the world. The world’s largest bond dealers in the U.S. and Europe, most of which have aggressively built e-trading solutions, are increasingly competitive with Japanese banks, offering Japanese investors access to global corporate and government bond markets. We expect these non-Japanese banks to build out their local Japanese e-trading offerings as well, which may incentivize local dealers to innovate more quickly.

Japanese investors are under similar pressures from global competition. Fee pressure from the world’s largest asset managers means the buy side more broadly must find ways to cut costs and operate more efficiently to remain competitive. Automation is and must be a key part of any efficiency strategy, which in turn, requires greater adoption of e-trading tools.

Macroeconomic factors are also at play. Low yields from local Japanese bonds continue to drive Japanese investors into other G10 and EM assets. Bond trading venues often provide the easiest access to the data and liquidity needed to invest around the world via the ecosystem of bond dealers and the prices they provide.

The language barrier between Japanese bond dealers and global investors can also limit the ability to trade via manual channels. E-trading removes these barriers and allows investors to access a wider range of price information no matter where they are in the world.

Similarly, time zone differences can also limit direct interactions between investors and dealers. While voice trading has traditionally been limited to trading during Japanese market hours, e-trading allows for transactions such as leave orders that can be traded outside of local hours, often helpful from a best-execution perspective. Further, as dealers increasingly price orders via algorithms, liquidity during Asian trading hours will continue to improve.

Access to Green Bonds

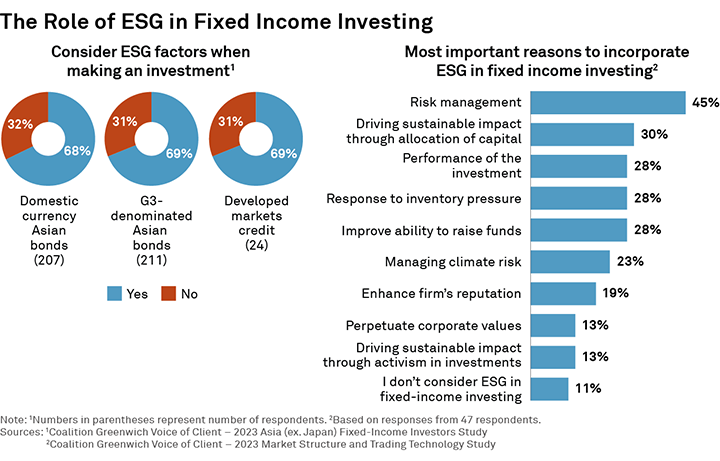

Green bonds and ESG-related fixed income products and data more broadly also present an opportunity. Nearly 70% of Asian investors in our study said they consider ESG factors when making an investment. In a related study of global investors, risk management and improving investor performance were ranked highly as factors to incorporate into fixed income decision-making. Increasing electronic access to these bonds and ESG datasets (which can be built into client dashboards to help source the best bonds) to Japanese investors can act as a further incentive to interact electronically.

Never Say Never

The last 15 years have taught us that market electronification is a story of when and not if. When the idea of all-to-all trading in the bond market was first brought to light more than a decade ago, many said it would never work. Today over one-third of trading on MarketAxess happens via its all-to-all Open Trading platform—proof that market participants are willing to change their habits when it means better liquidity and trading outcomes.

As for the fourth largest economy in the world, the largest holder of U.S. Treasuries and a very significant investor in global fixed income markets broadly, the Japanese market is an inevitable growth story for fixed income e-trading in the years ahead. Innovative solutions targeting the local market, competition from global competitors and strong demand for global debt will all act as tailwinds. While e-trading does change the nature of buy-side to sell-side relationships, relationships are still critical to market functioning, with technology ultimately enhancing the level of service provided.

Kevin McPartland is the Head of Research for Market Structure & Technology at Coalition Greenwich. Seiji Ishii, Head of Japan, leads our advisory with Japanese clients. Vignesh Srinivasan, Research Manager in Asia-Pacific, advises the markets divisions of several global and Japanese dealers.

Methodology

Coalition Greenwich interviewed over 450 buy-side fixed income investors in Japan in the fourth quarter of 2023. The study was conducted over the phone, online and in-person. Respondents answered a series of qualitative and quantitative questions focused on their dealer relationships, market expectations and use of electronic trading tools.