Top Trends in Asset Management for 2024

Share

Share

Methodology

Asset managers have no shortage of challenges facing them in 2024. In the near term, managers are navigating a mix of volatile markets, elevated interest rates and the continued threat of economic recession. Over a longer horizon, managers are contending with persistent pressure on fees, margins and overall profitability. Coalition Greenwich has identified a series of trends that will help determine winners and losers in this complicated environment and have a strong influence on the overall direction of the asset management industry in 2024 and beyond.

Introduction

Asset managers have no shortage of challenges facing them in 2024. In the near term, managers are navigating a mix of volatile markets, elevated interest rates and the continued threat of economic recession. Over a longer horizon, managers are contending with persistent pressure on fees, margins and overall profitability.

Baked into all these issues is technology. Artificial intelligence (AI) and other innovative tools are creating unprecedented opportunities to lower costs, improve efficiencies, deepen institutional relationships, and better serve clients.

However, all that innovation comes at a steep cost, and the demand for significant annual technology investments is emerging as a key driver of industry consolidation, as smaller asset managers seek the scale they need to keep pace with better-equipped rivals in a digital marketplace.

Coalition Greenwich has identified a series of trends that will help determine winners and losers in this complicated environment and have a strong influence on the overall direction of the asset management industry in 2024 and beyond:

- Private Markets: Opportunities for Traditional Managers

- Product Management: Asset Managers Get Back to the Basics

- AI: From Experimentation to Use Cases

- Service Quality: A Focus on “Service Alpha”

- Strategic Partners: On the Rise as Manager Rosters Shrink

- Stewardship: A Middle Path Through an Increasingly Complex ESG Environment

Private Markets: Opportunities for Traditional Managers

Over the next three years, 40% of institutional investors around the world plan to increase allocations to private debt. More than a third expect to boost private equity allocations, and about 30% plan to expand allocations to private infrastructure equity. Those increases would come on top of decades of expansion into private markets, as institutional investors seek to secure higher potential returns while diversifying portfolios, protecting against inflation and reducing volatility.

Investors building out allocations to private assets are not limiting their expansion to the brand-name managers typically associated with private markets. About 30% of institutions globally expect to add new managers to their rosters in both private debt and private equity. In 2024, those plans should translate into opportunities for traditional asset management firms to establish or expand their footholds in private markets.

Coalition Greenwich data shows that when it comes to private investments, institutional investors do not necessarily have a strong preference for specialists. They are more than willing to hire generalists for a private market mandate—as long as the generalist manager has dedicated private-market resources that demonstrate expertise and a true commitment to these complex asset classes.

That said, generalists moving into private markets will have to overcome one big advantage held by well-established specialists: institutions’ emphasis on hiring managers with proven track records in navigating long-term market cycles in private credit, private equity and other private assets.

Product Management: Asset Managers Get Back to the Basics

Increasing competition and mounting pressure on margins and balance sheets will force asset managers in 2024 to become increasingly diligent about business basics like operating efficiently and optimizing business functions. Simply put, as conditions become tougher, asset managers will have to focus on the basics in order to maintain profitability and achieve growth.

In practical terms, that means devoting as much or even more attention to managing existing products as the organization does to new product development. Although product management is less sexy, in a hyper-competitive marketplace, it will likely have a bigger impact on the bottom line.

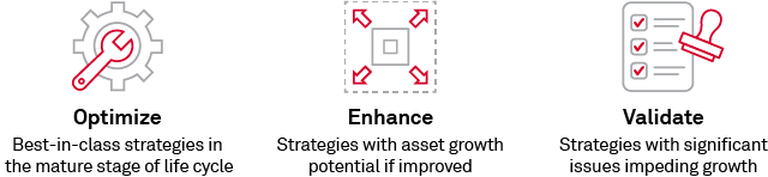

Coalition Greenwich works with clients to build linear, repeatable diagnostic tools that help managers assess the status of their overall product propositions and the individual products they offer. These “Product Viability Assessment Frameworks” use complex quantitative and qualitative analytic metrics to help managers classify their product strategies into the following categories:

Running this analysis is akin to getting an annual physical. The results will give management a clear view of the health and potential of each product strategy. Data from the exercise will reveal which products should receive additional funding for growth, which products might need additional investment to get back on track, and which products might be best discontinued because they are destroying value through underperformance, resource consumption or brand/reputation damage. Just as importantly, a careful annual analysis will show what specific steps the organization can take to enhance growth and improve profitability on a product-by-product basis.

AI: From Experimentation to Use Cases

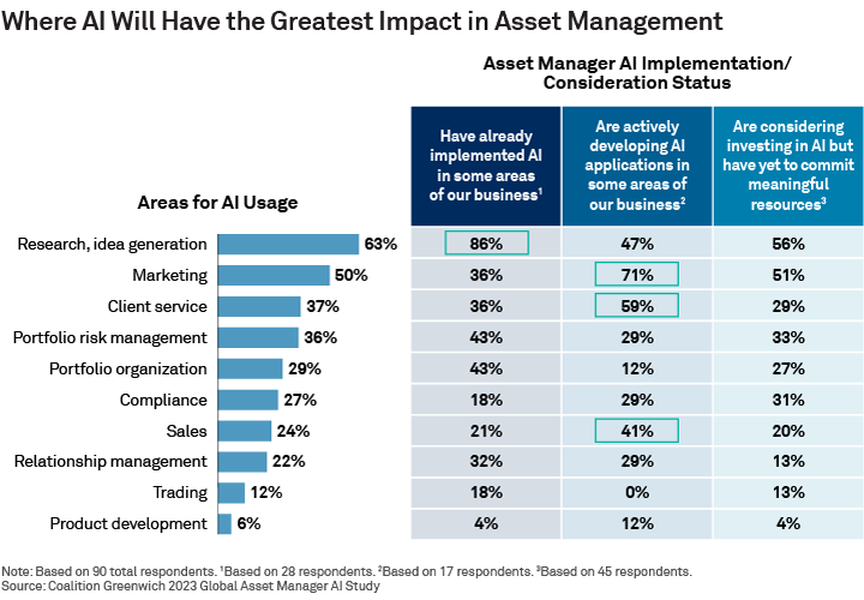

Asset managers in 2024 will move from experimenting with exciting new AI applications to rolling out use cases that deliver real value to their clients and to their own businesses.

Over the next several years, managers believe AI will have the biggest impact in two areas: research and idea generation, and marketing. More than 85% of asset managers have already implemented AI in some capacity for research and idea generation, and roughly 70% of managers who are actively developing AI solutions are concentrating on marketing. Sizable shares of managers are also working to integrate AI into client service and sales.

Asset managers looking to generate fast and strong returns on their AI investments in 2024 and beyond should consider focusing more of their development and implementation budgets on easing friction in the onboarding process, particularly the compliance aspect. Fewer than 1 in 5 global asset managers have implemented AI in compliance, and only about 30% say they are actively working to develop AI solutions for the function.

Recent Coalition Greenwich research has shown that onboarding, and related compliance, remains one of the most problematic “pain points” in institutions’ relationships with their asset managers. However, it is not an area that appears to be a top priority for the use of AI solutions.

Reducing the burden of AML and KYC processes will go a long way in improving the client experience, enhancing client perceptions of overall service quality and, thereby, minimizing asset and client attrition levels and boosting cross-sales. As a result, asset managers who are first movers in rolling out effective AI solutions in onboarding compliance could differentiate their firms and create a real competitive advantage.

Service Quality: A Focus on “Service Alpha”

Institutional investors are becoming increasingly aware of the growing variation in service quality among the asset managers they employ. Technology innovations, improved data analytics and other advances have provided asset managers with a robust tool set for improving service quality, addressing traditional service “pain points” in onboarding and other areas, and enhancing the client experience overall. Some managers have gone all in, investing heavily to upgrade technology and client-service staffing, and to integrate the two into next-gen service models. Other managers have not paid the same attention to service, leading to increasing divergence in service quality scores across the industry.

In 2024, we expect growing numbers of institutional investors to prioritize the concept of “service alpha,” or the client-service value that managers provide.

For managers, achieving service alpha requires a holistic framework addressing all the service touchpoints (or interactions) along the client journey. That framework must include independent client feedback that provides reliable data against which they can benchmark performance and set goals. It must also include cross-functional action plans to address shortcomings, assess performance and foster continuous improvement.

Managers looking to make rapid gains in client quality ratings (and minimize risk of future slippage) should focus particularly on issues most likely to trigger manager reviews. The top three trigger events for institutional investors are performance concerns, team changes and changes in portfolio risk/return profile. When any of these events occur, the manager must be ready to execute a seamless procedure of communications and service that provides transparency and preserves client trust. It is in these moments that service alpha, which takes years of hard work to achieve, will be enhanced or lost.

Strategic Partners: On the Rise as Manager Rosters Shrink

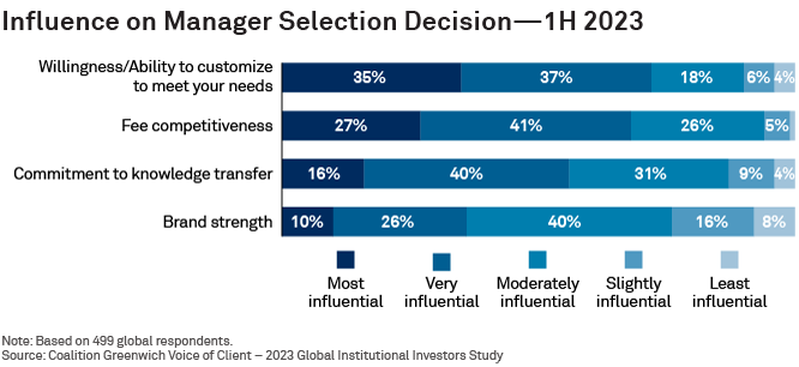

As shrinking rosters intensify competition for institutional investors in 2024, asset managers will be looking for ways to preserve existing relationships while trying to win new ones in a much tighter marketplace. Building off the notion of service alpha, managers working to strengthen their competitive positioning should consider the concept of “relationship alpha,” or the value their relationships bring to clients above and beyond pure investment returns, and relative to the value delivered by rival managers.

The chart that follows shows the manager traits that have the biggest influence on institutions’ selection of their managers. To generate relationship alpha, managers will have to excel in most, if not all, of these areas.

However, at a time when institutional investors are consolidating relationships, managers will have to go further to preserve opportunities for growth. To that end, conditions in the year ahead will place a premium on the elusive concept of “strategic partnership.” Managers who are considered to be strategic advisors have much stronger client relationships, lower rates of client and asset attrition, and are much more likely to hold multiple mandates.

To achieve strategic advisor status, managers must first meet the table-stakes requirements of competitive fees and a high-quality service model that is both effective and responsive. Then, managers must focus on the things that truly differentiate strategic advisors from their peers. Institutions identify three key factors that can elevate a manager to the status of strategic advisor:

- Willingness to customize products

- Best source of intellectual capital transfer

- Most useful advice on investment policy and strategy

Stewardship: A Middle Path Through an Increasingly Complex ESG Environment

Perceptions and practices in environmental, social and governance (ESG) are diverging, creating an increasingly challenging environment for asset managers. The U.S. is experiencing something of a backlash against ESG amid questions about the relationship between ESG goals and fiduciary responsibility, and new state laws banning the use of ESG criteria by some state entities.

Meanwhile, in Europe and Asia, institutional investors continue to adopt ESG standards. Even in Europe, however, things are becoming more complicated, as an emerging set of regulations and standards changes and narrows the definition of what qualifies as “ESG.”

Developing a universally acceptable approach to ESG will be a critical strategic priority for any asset manager operating across these regions. For that reason, in 2024, we expect growing numbers of asset managers to seek out a middle path that enables them to meet the expectations and requirements of institutional investors who have implemented ESG into their investment processes and portfolios, while also demonstrating strict adherence to fiduciary responsibility.

One sign that a shift is underway will be reduced usage of the actual label “ESG.” As that phrase draws fire in the U.S. and takes on a much more prescribed, legal meaning in Europe, look for asset managers to begin downplaying the abbreviation ESG in favor of similar, but less controversial terms like “stewardship.”

Mark Buckley, Parijat Banerjee, Todd Glickson, Christopher Dunn, Seiji Ishii, Ken Yap, Sophie Emler, Susan Gould, and Arifur Rahman advise our investment management clients globally.