Share

Share

Executive Summary

Programmatic research infrastructure encompasses automated, data-driven systems that underpin much of the analysis taking place in investment management today. As datasets grow larger, the use of tooling for consuming, coding and modeling is becoming imperative. Consequently, the need for employee upskilling and support is also increasing. In this report, Crisil Coalition Greenwich evaluates the current challenges and future needs of investment teams in regard to programmatic research infrastructure, analytics tooling and workflow efficiency. Our data and insights are based on interviews we conducted between September and October 2025 with 66 investment professionals working at buy-side firms in the United States, United Kingdom and Europe.

Methodology

During September and October 2025, Crisil Coalition Greenwich, in partnership with Bloomberg, conducted interviews with 66 CTOs, CIOs, heads of desks, quantitative researchers, analysts, portfolio managers, and other investment professionals working at buy-side firms in the United States, Europe and the United Kingdom. Questions explored the current challenges and future needs of investment teams regarding programmatic research infrastructure, analytics tooling and workflow efficiency.

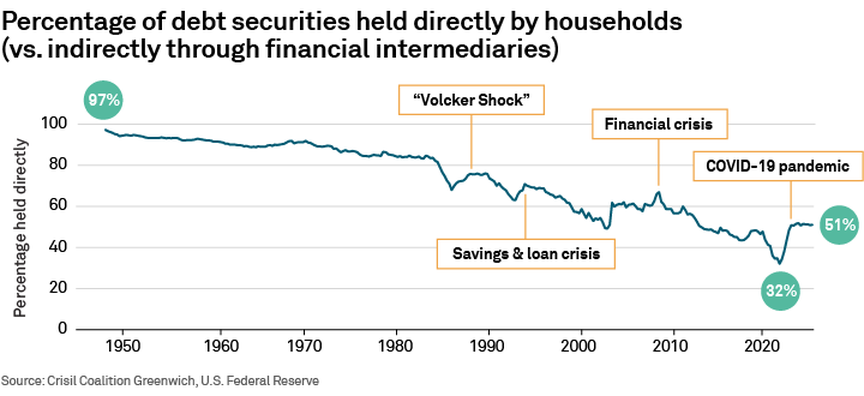

In 1945 at the end of World War II, 97% of fixed-income investments by U.S. households were held in individual bonds. The Investment Company Act of 1940, which created the modern mutual fund structure, was only five years old. Retail investors had just begun to take advantage of this new investment wrapper.

By the end of 2021—76 years later—only 32% of household fixed-income assets were held in individual bonds. Mutual funds and exchange-traded funds (ETFs) eclipsed individual bond buying, with easy access to a diversified portfolio, lower fees, more transparent pricing, and a trading process that looked and felt like the more familiar equity market. With the post-pandemic stock market soaring, buying individual bonds seemed relegated to retired baby boomers and ultra-high-net-worth investors, while the rest of the American investing public focusing on fixed-income ETFs. Then rates started to rise.

Bonds are back

As the federal funds rate grew to 5%, holding bonds until maturity was in vogue again. Retail bond buyers loved the high yields (relative to the zero rates they were used to) without the worry of short-term market movements that can impact the value of mutual funds and ETFs. As a result, individual bond holdings grew to 51% of retail fixed-income investments at the end of Q2 2025 (the most recent data), only slightly below the peak of 51.8% reached in Q4 2023.

A more automated and electronic bond market helped make this transition possible. Incumbent and start-up brokers finally focused on creating/upgrading bond trading screens for DIY investors. Electronic trading growth in the institutional market helped improve liquidity on trading venues traditionally geared toward retail investors. Financial advisors gained better access to real-time pricing, inventory and execution capabilities, which facilitated more investment opportunities to offer clients. And technology innovation allowed large asset managers to attract retail bond buyers to separately managed accounts (SMAs) via reduced minimums, while still making a profit due to more automated portfolio construction, rebalancing, tax loss harvesting, and cash management, ultimately requiring considerably less human intervention than it did a decade ago.

It’s easier to buy bonds but…

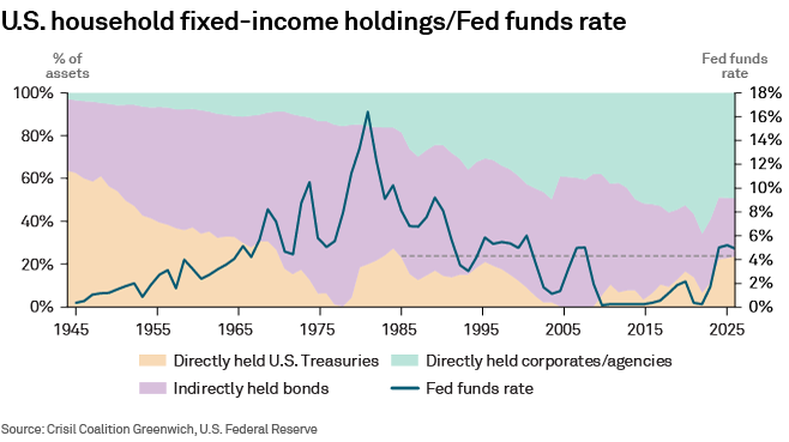

Market factors and these innovations worked together to support an impressive 20% growth in the value of overall U.S. household fixed-income holdings from pre-pandemic 2019 to the end of 2024. As money poured back into bonds, and the percentage of those held directly grew from 32% at the end of 2021 to 51%—their highest level since Q1 2013—the market began to debate if a structural shift had occurred. Were individual bonds once again a real competitor to the ETFs and mutual funds that had until recently been the dominant method of retail fixed-income investing?

Fast-forward to the Fed’s September and October 2025 rate cuts, and the evidence has begun to indicate the shift might ultimately prove to be cyclical. Non-zero rates for the first time in a generation made investing in fixed income exciting again, while market innovations made it easier than ever. But decades of data suggests that despite a vastly more liquid, transparent and accessible bond market, investment funds will retain their crown over the long run as the primary method of retail fixed-income investing in the United States.

It was mostly U.S. Treasuries

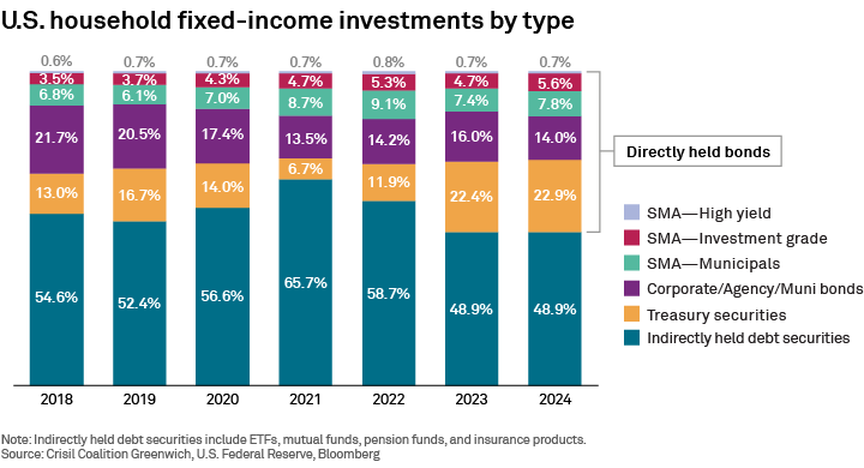

To understand why, it is important to dive more deeply into the numbers. Most of the retail wealth that poured into individual bonds following the 2022 rate hikes went into U.S. Treasuries (remember 9% I-Bonds?), which as of Q2 2025, account for roughly one-quarter of U.S. household fixed-income assets. This is the highest level in relative terms since 1985 at the tail end of the “Volcker Shock,” when then Fed Chairman Volcker dramatically raised rates to quash inflation. Another jump in retail buying of U.S. Treasuries happened in the early 90s following the savings and loan crisis. A third occurred in 2009, following the global financial crisis and, of course, the latest in the years following the COVID-19 pandemic.

Investors often buy U.S. Treasuries as a safe haven, which certainly drove buying in 2022. Retail investors were also excited to lock in 5% rates, something that bonds held to maturity do better than most ETFs, which continuously buy and sell bonds causing yields to fluctuate with market rates. The same shift from funds to bonds did not occur in the corporate bond market, however, despite some big-name issuers, such as Microsoft having higher credit ratings than the United States. In fact, directly held corporate bonds make up less of the U.S. retail fixed-income portfolio now than they did in 2019.

ETFs are a big part of why. Credit ETFs are plentiful and liquid for both institutions and retail investors, while Treasury ETFs—though they have certainly grown—are much less prevalent. That slower ETF adoption could bode well for future retail U.S. Treasury bond buying, but U.S. Treasury ETFs will inevitably capture more assets in the years ahead, while declining interest rates sap retail demand.

Treasury bonds are also easier to understand and buy. Even though retail investors must scroll through maturities and understand “yield to worst,” there is only one issuer and only 10 on-the-run bonds to choose from. Have you ever tried to apply filters to find corporate bonds to buy via a retail broker platform? Even if you know what to filter on, the results can be intimidating.

SMAs are big but not for everyone

Separately managed account (SMA) assets are up nearly 70% since pre-pandemic 2019, and at the end of 2024 (the latest data), accounted for over 14% of retail fixed-income investments. Looking only at corporate and municipal bonds, which make up the majority of SMA assets, SMAs held 50% of retail bond assets at the end of 2024, up from only 34% in 2019.

Primarily utilized by high-net-worth investors, SMAs can be customized for tax efficiency and investors’ expected cash flow needs, features most ETFs and mutual funds can’t provide. Technology has made it feasible for wealth managers to decrease account minimums from $2 million or more to $100,000 or less, which has drawn in more assets from a broader array of investors.

While SMA access will continue to expand in the years ahead, SMA assets are still cyclical. While the 14% of fixed-income investments they account for is up from 10% in 2019, it is below the 2022 peak of 15%, when rates were rising and money poured into bonds. SMA’s 50% share of corporate and municipal bond holdings is also down from its 2022 peak of 52%. Further, while account minimums are also likely to continue to decline as increased automation lowers costs for managers, individual ETFs or portfolios of fixed-income ETFs provide a less expensive and more accessible option for most U.S. retail investors.

Bonds are not stocks

Lastly, bonds just aren’t as exciting to retail investors as stocks, which tend to offer higher returns in exchange for higher volatility. Retail investors often buy stocks because they know the company, use the product or simply because they expect the price to go up. And they often do the buying directly from their phone. Bonds are more often bought based on risk and expected yield, and primarily via a financial advisor. Very few people seek out Apple bonds because they love their phone, or they see long-term upside. But they will seek out a bond from a company they don’t know because it is rated AA, has a 3% yield and matures in 2029.

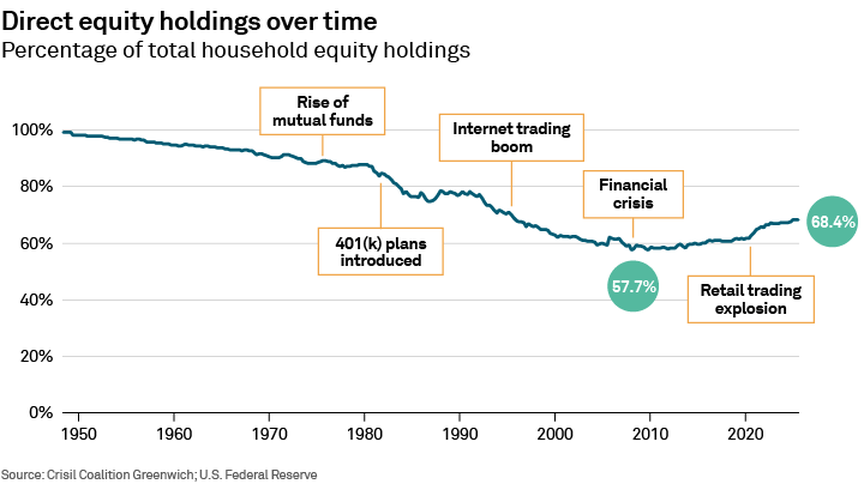

Just like bonds, equity markets have seen a move away from individual stocks toward funds over the past 80 years. However, the trough of directly held equity securities of 58% during the 2008 financial crisis is notably higher than the 30% hit by the bond market in 2021. Further, the growth since then, back to 68% in 2025, has been more consistent through the mini bear markets we’ve had in the past several years. Whether the estimated 30 million new retail investors that entered the market post-pandemic1 will keep buying and holding stocks through a prolonged bear market is yet to be seen. And while 401(k) plans generally do not allow for holding individual stocks, IRAs do—and IRA assets are double those in 401(k)s.2

The pie is getting bigger

But is it different this time? Past performance does not guarantee future results, and it is impossible to debate that the bond-trading ecosystem and the technology that powers it has made incredible strides in the past decade.

Fixed-income ETFs have seen an equally amazing growth trend over the past decade, with not only more diverse strategies but, perhaps more importantly, lower fees and easier access via zero-commission equity trading accounts. Most mass affluent investors in the U.S. can and will continue to get their fixed-income needs from ETFs.

However, as net worth approaches the high category, tools that provide easier access to bonds could change behavior. Let’s say an investor owns $100,000 of an investment-grade bond ETF with a 6 basis point fee. Despite the low cost and liquidity of that investment, it’s possible that transferring that position into a separately managed bond account could provide higher yield and a lower tax burden that nets to a lower total cost of ownership. Today, doing that comparison is nearly impossible, unless you’re a professional investor or you rely on a financial advisor.

But perhaps an easy to use, side-by-side comparison tool could go a long way to changing behavior. If the benefits are clear, then moving those assets will be obvious. Providing a mechanism to seamlessly sell the ETF and buy the bonds after the decision is made would be even better. None of this is science fiction—the technology exists now. Such solutions could allow SMAs to retain their post-pandemic gains and grow them in the years ahead, even when rates decline.

With all that said, everyone should cheer the improvements in liquidity and accessibility in the bond market we’ve seen over the past decade. Fixed-income ETFs and mutual funds hold bonds, and so demand for those two still drives demand for the bonds themselves, which improves liquidity and market access for everyone.

Kevin McPartland is the Head of Research for Market Structure & Technology at Crisil Coalition Greenwich.

1The Economist - https://www.economist.com/finance-and-economics/2021/08/21/just-how-mighty-are-active-retail-traders

2Investment Company Institute - https://www.ici.org/statistical-report/ret_25_q2

Methodology

Data from the Federal Reserve and Bloomberg was analyzed in Q3 2025 to better understand the long-term fixed-income investing habits of U.S. households. Several datasets were combined to paint a complete picture of the fixed-income holdings of U.S. households from 1945 through Q2 2025. Institutional bond market participants and service providers were also interviewed to help interpret the data and inform the research results.