Share

Share

Executive Summary

Buy-side traders are doubling down on transaction cost analysis (TCA) as a crucial tool to optimize performance and boost returns. With trading growing increasingly complex and competitive, the ability to accurately measure and minimize transaction costs has become a key differentiator for investors seeking to maximize returns. Every buy-side desk in our study conducted TCA for their equity trading in the past year, with almost 80% doing so at least quarterly. Brokers and TCA providers take note: A whopping 85% of buy-side traders rely on quantified TCA to assess broker trade performance, with 20% using it as their primary metric. Just 5% consider it unimportant in their review process. The days of TCA as a mere box-checking exercise for best-ex reviews and compliance meetings are fading. Today, it’s a vital component of a head trader’s toolkit, empowering institutions to refine their strategies, optimize performance and, ultimately, enhance their portfolio returns. In a world where every basis point counts, TCA is no longer a nice-to-have, but a must-have. By harnessing the power of TCA,

Methodology

From July through September 2024, Coalition Greenwich interviewed 40 buy-side equity traders in North America. The study was conducted over the phone, online and in-person. Respondents answered a series of qualitative and quantitative questions about their daily workflow, broker selection and evaluation, technology platforms used, commissions, technology budgets, and business practices in the U.S. cash equity space.

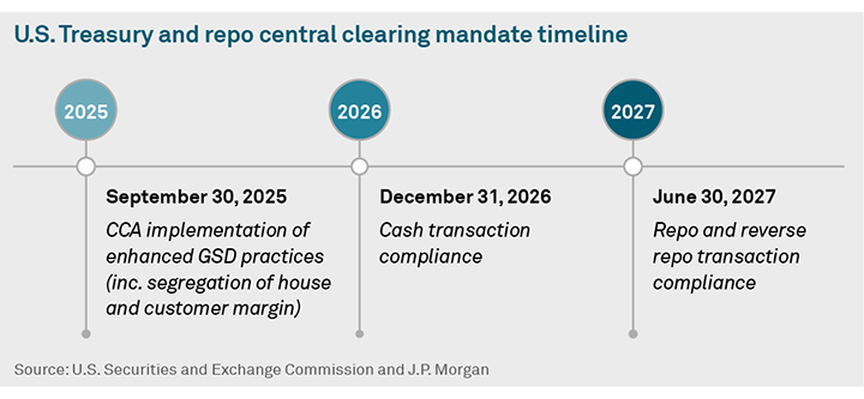

Crisil Coalition Greenwich published its previous paper on the U.S. Securities and Exchange Commission’s (SEC’s) central clearing mandate of U.S. Treasury securities and repo in Q2 2025.1 Since then, several updates to clearing models, participating covered clearing agencies (CCAs), technology, industry concerns, and more have come to light.

In addition, SEC Commissioner Mark Uyeda has been tasked with overseeing the implementation of the U.S. Treasury Clearing Mandate. On September 30, 2025, the SEC released an update on its website focusing on the remaining issues expressed by market participants.2 This report examines these challenges to central clearing, summarizes the plethora of recent announcements concerning the development of new clearing models and enhancements to U.S. Treasury and repo clearing practices, and provides industry perspectives on how the remaining steps to go-live dates might unfold.

Clearing model enhancement

When we covered this topic earlier this year, different approaches to support both done-with (executed between an executing firm customer and an agent clearing member (ACM)) and done-away (executed between an executing firm customer and another government securities division (GSD) netting member or its client) business models were starting to emerge for cash and repo trading. A degree of uncertainty loomed over how the industry would evolve practices to meet regulatory guidelines.

More recently, a deluge of announcements from the Depository Trust & Clearing Corporation (DTCC), the Chicago Mercantile Exchange (CME), Intercontinental Exchange (ICE), the London Stock Exchange (LSEG), and Euroclear, as well as trade associations, including the Securities Industry and Financial Markets Association (SIFMA), the International Swaps and Derivatives Association (ISDA) and the Futures Industry Association (FIA), have shed some light on lingering industry issues.

Addressing ‘double margining’ issues with FICC’s Collateral-in-Lieu (CIL) service

On September 3, DTCC announced that its Fixed Income Clearing Corporation (FICC) subsidiary formally submitted a rule filing with the SEC to enhance its Sponsored Service with a new tri-party offering. The Sponsored General Collateral (GC) CIL service is “…designed to leverage the haircut typically posted by dealers to money market funds and other cash investors in tri-party via a central clearing party (CCP) lien that is applied ‘in lieu’ of both a Sponsor guaranty of client performance and the posting of margin to the CCP…, thereby solving for the so-called ‘double-margining’ challenge.”3

This enhancement allows FICC to take a lien on collateral instead of collecting additional margin on the cash side of the trade. Participants are able to leverage existing agreements and infrastructure, which increases capital and margin efficiency, simplifies compliance, and improves access to clearing through FICC’s Sponsored GC service. The CIL service will be offered by leveraging the Bank of New York’s (BNY’s) tri-party service to manage collateral and settle both done-away and done-with repo business. The filing will appear on the Federal Registrar with a public comment period. FICC is planning to launch CIL in December 2025, pending regulatory approval—something members are happy about on the money-market side and feel is well-received to help alleviate double margining and bank risk-weighted assets (RWA).

Accounting review of FICC agent clearing service (ACS) model

On September 11, SIFMA’s Accounting Committee Working Group completed its review of FICC’s ACS model and consulted with the staff of the SEC’s Office of the Chief Accountant regarding questions that had been raised. As part of this review, broker-dealers acting as an agent to the customer when performing clearing services were keen to hear that customer done-away repo transactions in the ACS can be treated with balance sheet netting.

In its white paper, SIFMA writes, “The primary question addressed is whether the ACM is acting as a principal or as an agent with respect to the customer’s repo transaction facing FICC post novation. This distinction is important because an ACM acting as principal is required under United States Generally Accepted Accounting Principles (“US GAAP”) to recognize the customer’s repo transaction on its balance sheet. An ACM acting as agent would not recognize the customer’s repo transaction on its balance sheet but would recognize or disclose any assets, liabilities, and/or contingent off-balance-sheet exposures resulting from its role as agent (e.g., guarantees, margin receivables and payables). This analysis applies to both ‘Done-With’ and ‘Done-Away’ trades.”4

FICC’s ACS model for tri-party repo announced

FICC announced another exciting development on September 23 with its proposed ACS service model for tri-party repo.5 Investors wanting tri-party capabilities by leveraging BNY’s tri-party service were excited to learn that FICC submitted a proposed rule change filing to the SEC to offer an ACS Triparty Service for repo to ACMs and their executing firm customers. This includes done-with or done-away repo. The development of the proposed ACS Triparty Service is expected to offer more clearing and margin efficiency to ACMs by enabling two main parties to focus on the economics of a trade as the tri-party agent deals with administrative tasks like collateral management.

Lingering advocacy points

Expanding the inter-affiliate clearing exemption

The inter-affiliate exemption, which is designed to exempt administrative trades between different parts of the same firm from the clearing mandate, is a top concern of market participants. Fortunately, some headway is being made with this issue. In our Q2 report, we wrote:

“Market participants are seeking relief in some of the ‘unpopular’ aspects of the mandate. The inter-affiliate carve-out is one example. In this case, eligible FICC members (e.g., banks, broker-dealers or FCMs) may take advantage of the exemption from the Treasury repo clearing requirement. However, if the exemption is used, then the affiliate’s Treasury repo needs to clear (as if it were a FICC member)—which is causing some head-scratching. Inter-affiliate trades are purposed for liquidity management.”

Most in the industry feel inter-affiliate trades shouldn’t be brought into scope, given what they are used for. In this sense, hearing the rule “isn’t fit for purpose” is a common gripe. One industry professional we spoke with was struggling to establish a better understanding of the inter-affiliate carve-out with the SEC. (Some industry experts are suggesting the use of volume thresholds may be helpful in determining whether clearing is mandated or not.) All told, industry sentiment is clear: Moving U.S. Treasuries from one entity to another for inventory management to facilitate settlement should not fall into scope. There is a continued push to either change this language or scrap it.

In its September 30 release, the SEC acknowledged the need for the exemption to include cash transactions and to allow for internal liquidity and collateral management. Including additional types of affiliates and broadening the concept of affiliate within the inter-affiliate exemption has also been mentioned. Although we don’t yet have the specifics, this announcement has the potential to be great news for the industry.

Clarifying the extraterritorial scope of the U.S. Treasury clearing mandate

The impact of the clearing rules on non-U.S. firms has also been a point of contention. We are pleased to see the SEC include this lingering point in their September 30 release, as we also addressed over-scoping and international reach concerns in our previous report:

“The final clearing rules determine clearing requirements based primarily on the market participant type (e.g., securities dealer, hedge fund) and registration status with a CCA. As written, it appears they do not focus solely on U.S.-based firms. If no further changes or clarifications are put forward by the SEC, the rules will bring into scope a long list of internationally based firms operating in the U.S. Treasury market in the U.S. The swaps market again sets a precedent here, having defined a U.S. person to determine who was required to follow CFTC rules. There is no such distinction in this case, however, suggesting a more global mandate.”

No doubt many of us recall grappling with the definition of a U.S. person during the advent of the swaps clearing proposal when sorting out which entities were subject to the mandate. Likewise, market participants will welcome guidance on this topic from the SEC and look forward to more prescriptive language within the proposal to avoid confusion and non-compliance.

The impact of failed trades or clearing agency outage

We emphasized concerns regarding credit checks and the management of trade failures in our Q2 paper.

“First and foremost, credit checks are a cause for concern. Typically, the FCM community wants activity and credit-limit data before they become responsible for a trade. None of the infrastructure required for pre- or post-trade credit-limit checks that FCMs need to operate exist today in repo. While there is precedence for solving this problem in the swaps market, questions remain as to how problems might surface and how such an infrastructure will evolve to remediate them.

For instance, more than 50% of repo trading is done by voice today (even if it is booked electronically). A precarious scenario could arise should a counterparty’s clearing agent lack enough credit, particularly if this was discovered after a voice trade was executed. Which party is on the hook to ensure the trade will perform and is cleared? Is a transaction void if there is a failure or does it live on in some capacity? Additionally, no one is certain who will actually run the credit checks or how quickly they will need to happen. Industry professionals agree this issue needs to be ironed out immediately or there’s a chance that done-away repo activity may be hindered. While the technology to perform these checks does exist, the industry still needs to agree on the best path forward.”

The SEC also acknowledges failed trades are a problem in its September 30 release and adds another layer by mentioning clearing agency outages. However, to date, confusion remains concerning how credit checks should be managed. Presently, the SEC does not include any requirement that CCAs perform or get involved in FCM credit checks. Leaders we spoke with believe the progression of credit checks will ultimately wind up being an industry solution, rather than a regulatory one, and could possibly involve pre-funding or more real-time use of the OSTTRA’s LimitHub platform to connect trading venues and CCPs.

Meanwhile, the processes around failed trades and outages will likely be guided by some regulation. We expect to see similar practices used in U.S. swaps clearing, where the remediation of two types of defaults—administrative errors and clearing member defaults—are spelled out. No doubt, there should also be guidelines pertaining to when the clearinghouse takes control of a position(s) and what the recovery plan will look like.

Assessing gross versus net margin alternatives for segregated customer accounts

Lastly, the SEC points to margin practices for customer accounts under Rule 15c3-3a as another area in need of more work. The debate concerns the collection of customer margin for U.S. Treasury securities by broker-dealers that is deposited with a qualified clearing agency (QCA) as a debit in the reserve formula resulting from money owed to the firm by customers, e.g., from funds borrowed on margin accounts. This new practice introduces questions relating to how margin should be calculated and delivered.

Historically, a netting approach is used, where firms calculate margin across combined customer accounts, with consideration for offsetting long and short positions. The new rules specifying margin now get calculated on a gross basis for each customer individually, effectively eliminating any netting benefit. Margin must now also be delivered for each customer separately to the QCA, adding operational challenges.

Risk-reducing benefits of cross-product margining aren’t recognized in SA-CCR

ISDA has been vocal about a bank regulatory capital element at play concerning U.S. Treasury clearing and cross-margining. Presently, the benefit of cross-product and cross-margining isn’t recognized in the Standard Approach for Counterparty Credit Risk (SA-CCR) due to insufficient netting across, e.g., U.S. Treasury securities and futures. As a result, the exposure at default (EAD) client portfolio calculation won’t have risk-reducing elements, which leads to unnecessary capital charges that banks are forced to hold. Increased capital requirements may make it more difficult for banks to facilitate cross-margining for clients, if these savings can’t be realized as they are within the clearinghouse. Capital markets leaders are actively meeting with regulators to ensure this issue is top-of-mind for the next version of the Basel endgame.6

Margin efficiency and the future state

CME and FICC provide quarterly statistics focused on cross-margin savings that follow Committee on Payments and Market Infrastructures (CPMI) and the International Organization of Securities Commissions (IOSCO) standards.7 In doing so, CME collaborates with FICC to align values relating to participants that had margin savings. Typically, cross-margining combines futures and U.S. Treasury securities positions. During Q2 2025, these savings were roughly 57% of the margin requirement. The notional or dollar amount of margin savings is also publicly available. Both figures are a good way to keep track of the progress of the cross-margining program.

Expanding FICC cross-margining to end users

In September 2025, DTCC cleared roughly $11.1 trillion notional of U.S. Treasury securities daily, more than double the volumes observed over the past two-and-a-half years. While it is difficult to estimate how close the industry is to clearing the majority of the market, the introduction of enhanced clearing models and positive accounting treatment for balance sheet relief are positive signs. CME added to this momentum when it announced its intentions to expand cross-margining to end users on September 29, 20258—addressing a top challenge that was also acknowledged by the SEC in its September 30 release.

CME worked with FICC to launch a cross-margin program in January 2024. Initially, the program worked well and proved to be efficient for basis trades with the opposite positions in futures and cleared cash. Over the past six months, roughly 18 new entrants signed paperwork to enter CME’s direct clearing process, as adoption escalates. Many clients have done well finding cross-margining opportunities. However, CME-FICC is a house program only available to direct clearing members at this time. If approved by regulators, the expanded agreement will extend the program to dually registered FCMs and broker-dealers who wish to make the program available to their clients.

The customer expansion is expected to encapsulate both done-with and done-away models. One possible limitation is that, on the FICC side, customers would need to get margin savings by funding margin themselves—a workflow that isn’t typical today in the U.S. Treasury and repo markets (although client funding of margin is standard in the derivatives space). The market will need to get more comfortable with customers posting their own margin versus a sponsoring member covering the CCP margin obligation.

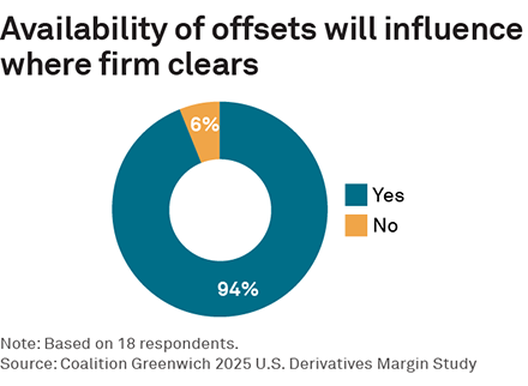

CME set to enter securities clearing

Data from our recent study shows that 94% of participants believe offsetting risk positions—or offsets—affect where a firm might choose to clear.9 Respondents from clearing broker, executing broker and buy-side firms agree that if they could receive offsets and gain margin, collateral and other efficiencies across USD swaps, futures (and options on futures) as well as cash securities (U.S. Treasuries and repo) in one location, they would be enticed to reconsider where these products clear.

In late 2024, CME Securities Clearing, Inc. (CMESC) filed an application with the SEC to register as a clearing agency for secondary cash market transactions, extending the company’s capabilities.10 The development is intended to provide cross-margining of futures, options, swaps, and cash in one place to improve the efficiency of financial instrument use and risk requirements. While CME-FICC cross-margining has been prioritized this year, it is likely this initiative will move to 2026, depending on engagement with regulators, as approval is still pending.

The hedge fund community and high-frequency trading firms may find value in CMESC. These customer types tend to trade a variety of products, including interest-rate swaps (IRS) and futures, which would benefit from cross-product margining efficiency but can’t take advantage of current programs, since most aren’t direct FICC members (although some asset managers have set up direct FICC memberships to take advantage of the house cross-margin program). Although it’s feasible, sell-side firms could also take advantage of the CMESC program. FICC has a lot of inertia with these member firms, which would likely continue to rely on CME-FICC cross-margining.

More CCAs expected

Early this year, Euroclear launched its delivery-versus-payment (DVP) repo service as an initial step into clearing services for U.S. Treasury securities.11 The service offers cash lenders similar operational efficiency for DVP repo transactions as tri-party repo transactions. This offering is also designed to include both cleared and non-cleared DVP repo by cash lenders, including FICC DVP sponsored repo trades.

Meanwhile, in May 2025, the London Clearing House (LCH) began the clearing of U.S. Treasury futures as part of a partnership with the FMX Futures Exchange. The agreement would allow for cross-margining of IRS and futures, and raises speculation that LCH is on a path to also clear U.S. Treasury cash securities and repo. Our October 2024 findings reveal that market participants feel the clearing of U.S. swaps and interest-rate futures in one clearinghouse could yield potential margin savings of up to 80%. This research sets a positive stage for the extension of this type of clearing structure.12

Finally, on August 19, 2025, ICE Clear Credit announced the submission of an application and rulebook to expand its current registered clearing agency designation to include U.S. Treasury securities and repo clearing.13 ICE Clear Credit currently clears credit default swap (CDS) instruments. ICE intends to leverage ICE Link for trade matching, porting and connectivity across platforms. However, the U.S. Treasury clearing service is intended to be a distinct offering with its own rulebook, membership, risk management framework, financial and liquidity resources, and risk committee. Both done-with and done-away models will be supported.

Conclusion

The industry is making progress as we head toward the go-live dates for U.S. Treasury securities and repo clearing. New clearing models are being developed by CCAs to address clearing preferences as well as remediate industry hurdles connected to done-with and done-away models and cross-margin efficiency. Further, client clearing is happening at scale at FICC today through Sponsored and ACS Services, and additional plans to extend clearing to more end users are in motion.

While there is no immediate indication that go-live dates for the mandate will again be pushed back, challenges could create further delays if they aren’t resolved by the first or second quarter of 2026. Although several industry concerns still loom, capital markets professionals take the September 30 SEC release acknowledging these top-of-mind issues as a positive sign the implementation of the rules will stay on track.

Audrey Costabile is a senior analyst on the Market Structure & Technology team.

1Crisil Coalition Greenwich, U.S. Treasury Clearing: A New Timeline and Uncertain Trajectory, June 9, 2025

2U.S. Securities and Exchange Commission, Update on Working Toward Treasury Clearing Implementation, September 30, 2025Challenge

3DTCC, FICC Submits Rule Filing with the SEC for Approval to Offer New “Collateral-in-Lieu” Service as Part of its Sponsored General Collateral Offering, September 3, 2025

4SIFMA, Accounting Treatment for UST Repo Transactions Cleared Through FICC, September 11, 2025

5DTCC, FICC Submits Proposed Rule Change Filing to the SEC to Offer New Agent Clearing (ACS) Triparty Service, September 23, 2025

6ISDA, FIA, SIFMA, Cross-product Netting Under the US Regulatory Capital Framework, April 2025

7CME Group, CPMI-IOSCO Quantitative Disclosures, www.cmegroup.com

8PR Newswire, CME Group Files to Expand FICC Cross-Margining to End User Clients, September 29, 2025

9See Coalition Greenwich, Fixed Income Cross-Margin Opportunities: A Driver of Change, September 17, 2015

10CME Group, CME Securities Clearing, Inc.; Notice of Filing of an Application for Registration as a Clearing Agency Under Section 17A of the Securities Exchange Act of 1934, December 13, 2024

11Euroclear, Euroclear Launches U.S. Treasury DVP Repo Service, February 18, 2025

12See Coalition Greenwich, The Portfolio Margining Imperative for Interest-Rate Derivatives, October 16, 2024

13ICE, ICE Announces Its Treasury Clearing Application and Rulebook Have Been Published by the U.S. Securities and Exchange Commission, August 19, 2025

Methodology

Crisil Coalition Greenwich spoke with 20 industry leaders at global clearing firms as well as professionals working on both the buy side and sell side during October 2025. Conversations focused on the challenges and trends related to U.S. Treasury and repo clearing requirements.