Formerly known as Market Intelligence & Analytics

Formerly known as Market Intelligence & Analytics

Risk Consulting

We help financial institutions develop and validate risk models, design scorecards and calculate risk parameters.

Risk Models and Framework Services

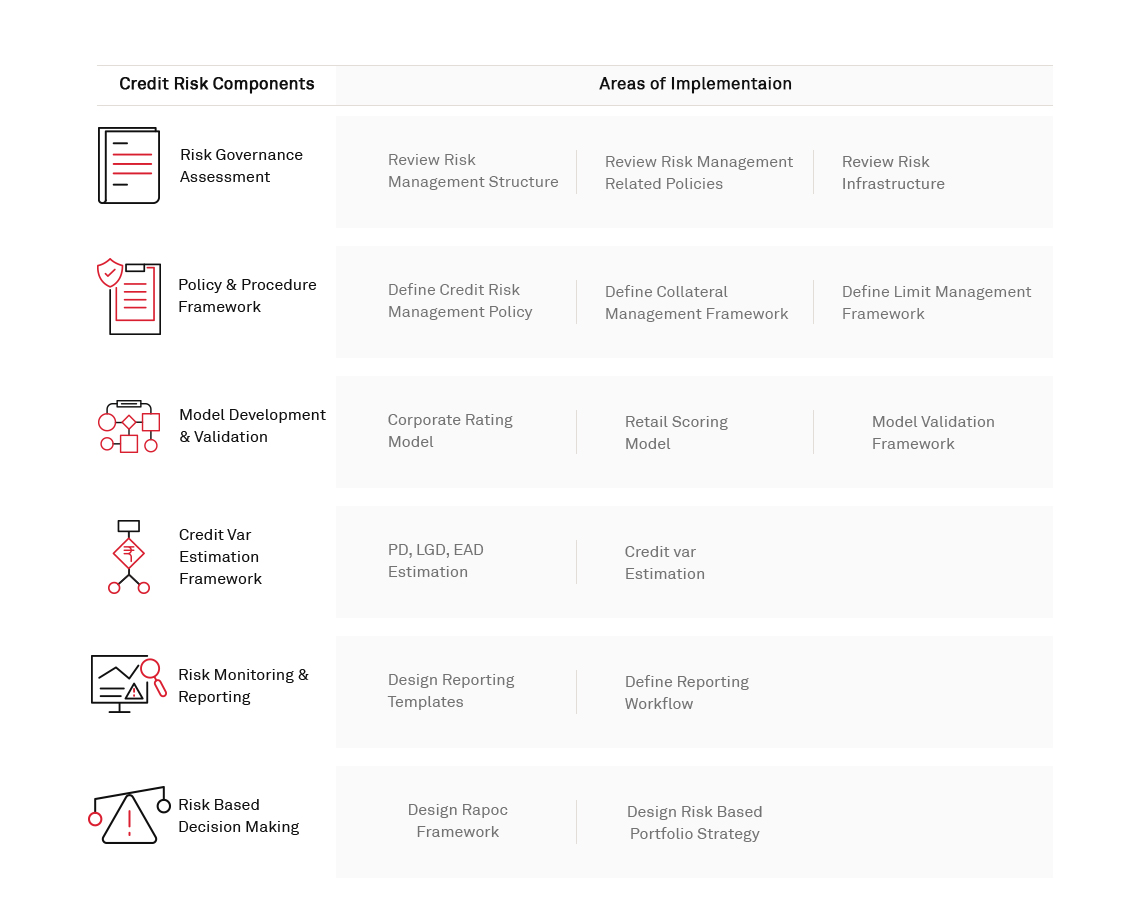

Credit Risk Consultancy Services

Market Risk Consultancy Services

Market risk management consulting includes development and validation of risk measurement models, development of asset-liability management (ALM) framework, as well as the development of related policies and procedures.

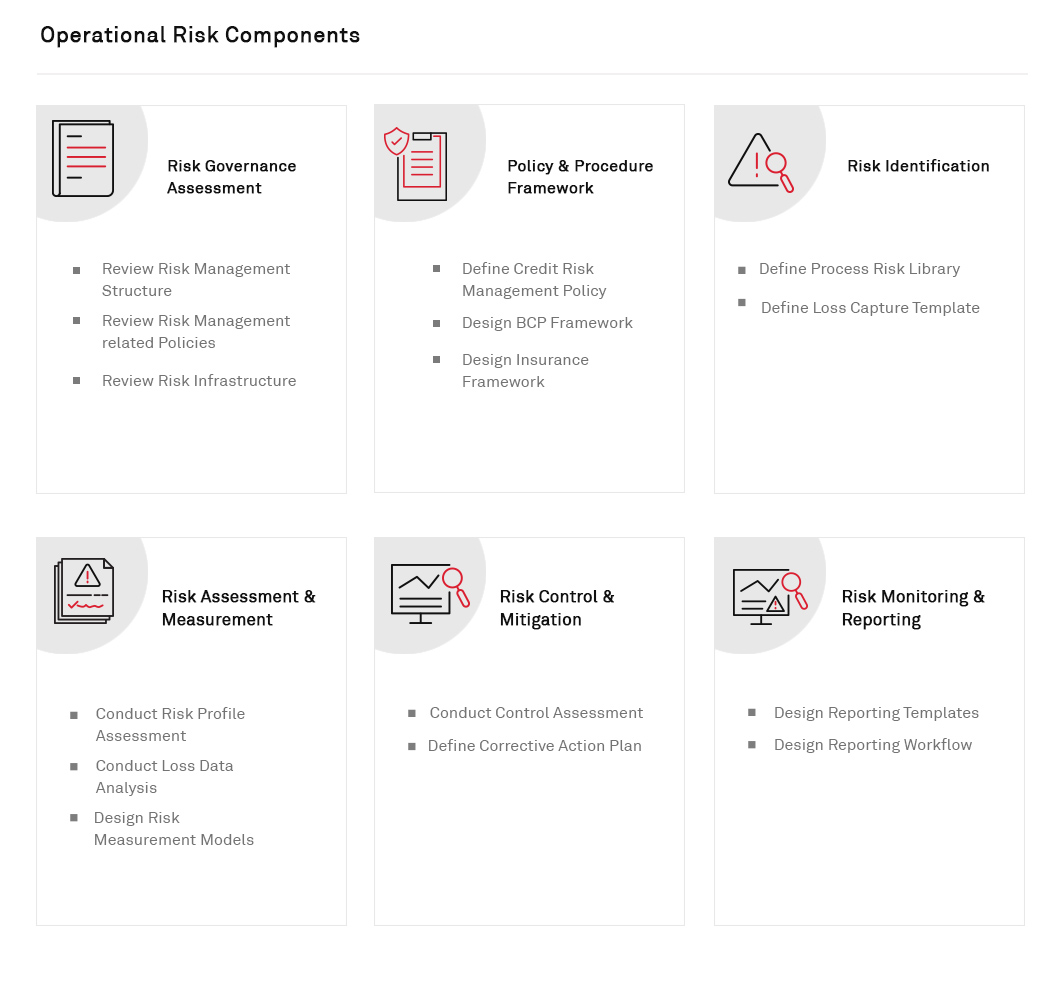

Operational Risk Consultancy

Crisil Risk Solutions reviews, recommends and designs operational risk management frameworks.