How the capital markets feel about tokenization

Share

Share

The adoption of Japan’s Asset Owner Principles could trigger a surge in demand for outsourced chief investment officer services (OCIO) among pension funds and other institutions.

The government of Japan established the Asset Owner Principles in 2024 as part of its broader set of investment, governance and risk management reforms aimed at improving institutional investment outcomes, enhancing long-term investment returns for savers and strengthening the country’s capital markets.

Whereas earlier reforms had been targeted mainly at Japanese companies and investment managers, the Principles are focused on asset owners. Japanese policymakers concluded that weak governance among the country’s asset owners was contributing to what it saw as the country’s suboptimal institutional investment performance. To rectify that situation, the government developed and issued the Principles, a set of guidelines intended to enhance how large institutional investors, such as public and corporate pension funds, insurers, and endowments and foundations, manage assets and oversee investment managers.

The voluntary guidelines codify best practices and expectations for institutions in governance and fiduciary responsibilities, strategic investment strategies and portfolio allocations, asset manager selection, monitoring and fees, and other areas.

Ultimately, the government’s goal in issuing the Principles was to professionalize Japanese asset owners, many of which have been managing billions of dollars in assets with small investment teams, limited expertise and opaque governance structures.

Professionalizing asset owner investment operations

By encouraging asset owners to tighten governance policies and adopt best practices in investments and other areas, the Principles could eventually trigger dramatic changes in institutional investment operations, portfolio allocations and manager rosters—including a potential surge in demand for OCIO services.

Professionalizing investment operations and modernizing portfolios according to the guidelines laid out in the Principles will increase complexity. Many asset owners, especially smaller institutions, will struggle to marshal the expertise and resources required to operate in this new environment.

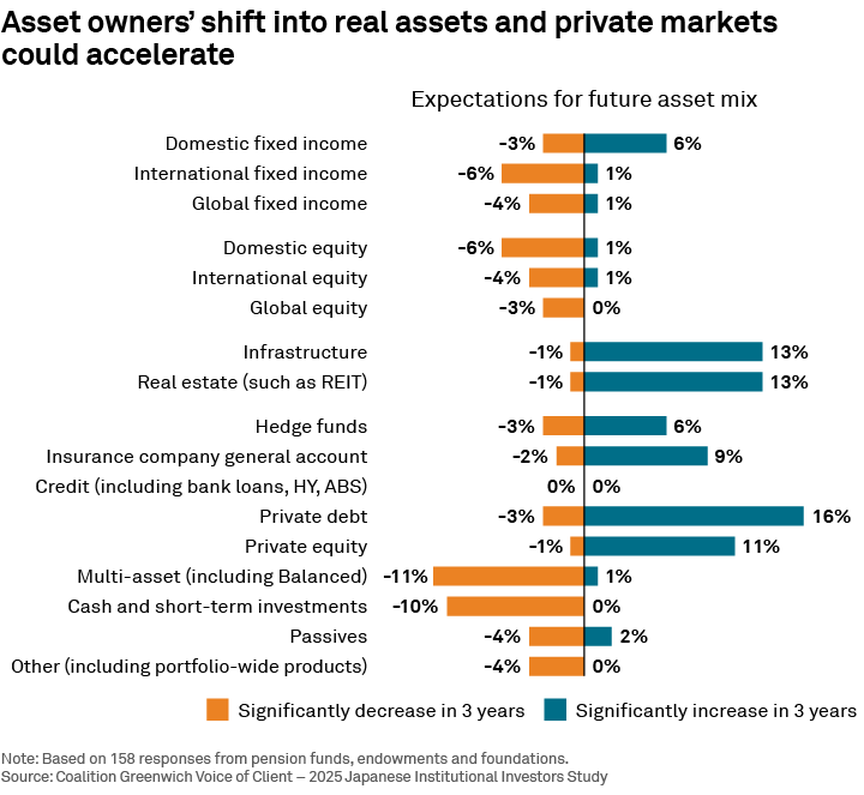

As just one example, pursuing the Principles’ ultimate goal of enhancing long-term risk-adjusted returns could lead to a shift in portfolio allocations away from fixed income, especially domestic bonds, toward risk assets, especially alternatives and private assets.

As illustrated in the preceding graphic, Japanese pension funds, endowments and foundations already have plans to expand allocations to real estate and alternatives. Approximately 16% of these asset owners plan to significantly increase allocations to private debt over the next three years, and more than 1 in 10 expect to meaningfully expand allocations to real estate, infrastructure and/or private equity. In each case, only a relative handful of asset owners plan to reduce these allocations.

If the governance and investment guidelines included in the Principles accelerate this move into real estate and alternatives, asset owners will have to contend with the increased complexity that comes from investing in these illiquid and often unfamiliar asset classes. In private debt, private equity, real estate, infrastructure, and other alternative asset classes, investors face unique challenges in cash flow management, valuation, monitoring and risk management, and manager selection/access.

Those tasks would compound new demands arising from implementation of the other governance and investment guidelines spelled out in the Principles. The resulting workloads could strain the operational capacity of some Japanese asset owners, especially smaller institutions.

Some asset owners see OCIO as a potential solution

For some of these institutions, the answer might be OCIO. Currently, only about 3% of Japanese institutions use an OCIO manager. That usage rate is far lower than that found in other institutional markets. For example, over 20% of U.K. institutions use an OCIO manager, as do 16% of U.S. institutions.

If implementing the Principles brought Japan’s usage to levels comparable with these markets, that shift alone would drive huge growth in OCIO. Around the world, most institutions that use OCIO allocate 100% of their assets to the OCIO manager. Factoring in even the smaller group of institutions that use OCIO only for a specific part of their portfolio, OCIO managers claim over 90% of their clients’ portfolio assets on average across North America and Europe.

How likely is it that Japanese institutions will turn to OCIO? One way to answer that question is to look at what services OCIO managers offer and compare that list to projected needs among Japanese asset owners who are in the process of adopting the Principles. The graphic below shows the most common services offered by OCIO managers.

The following graphic shows which of these services resonate most with asset owners around the world. The chart lists the top objectives of asset owners who utilize OCIO managers. Asset owners want OCIO managers to augment their own investment expertise and their access to attractive investment strategies and managers. Asset owners are also looking for OCIO managers to enhance overall investment returns and risk-management capabilities, and to buttress fiduciary oversight and reporting.

Many of those objectives track word-for-word with the guidelines laid out in the Asset Owners Principles. Others reflect some of the likely second-order effects of broad implementation of the Principles. For example, if the enhanced fiduciary responsibility and investment practices introduced by the Principles lead to increased investment in private assets, Japanese asset owners will likely be seeking access to new strategies and managers, some of which might be out of reach for smaller institutions offering smaller mandates. For these asset owners, OCIO managers can provide real value by pooling assets and securing mandates with large, in-demand specialists in private debt, private equity and other asset classes.

A changing landscape for asset management

Adoption of the Asset Owner Principles will have widespread ramifications for the Japanese investment management industry. Changes in the way asset owners interpret fiduciary responsibility, craft and implement investment strategies, choose managers, and allocate portfolio assets could alter the competitive landscape for asset managers. For example, asset owners looking to diversify portfolios might become more open to working with foreign managers and with specialists in private assets, real estate and alternatives.

Increased adoption of OCIO by Japanese asset owners could also have an impact on asset management fees. Declining profitability has been a major challenge for institutional asset managers in Japan, and fee compression has been a big driver of that trend. Widespread use of OCIO by Japanese asset owners could put additional downward pressure on fees.

The entry of OCIO managers would mean more competition for institutional mandates, which could drive down fees. It could also force some managers to discount fees as they are displaced from traditional mandates and instead take on sub-advisory roles for OCIO managers.

To compete in this new environment, both domestic and foreign asset managers will have to make adjustments to their strategies. Those adjustments should include a response to increased demand for OCIO. This process is already underway. In 2025, Nomura announced that it was expanding its OCIO offering in Japan, and existing OCIO offerings from Goldman Sachs Asset Management, BlackRock and other asset managers gained momentum.

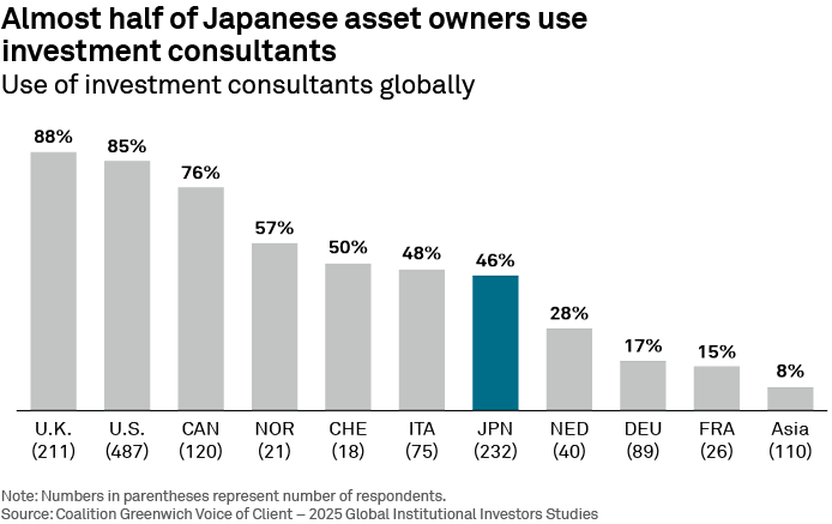

Also in 2025, Mercer announced that it was partnering with Mizuho Financial Group to provide OCIO services in Japan. This announcement was particularly notable in that it brought together the Japanese trust bank industry with the global consulting industry. As shown in the graphic above, about half (46%) of Japanese asset owners use investment consultants, a share that’s up from 43% in 2024. Among Japanese pension funds, endowments and foundations, that share tops 50%.

Meanwhile, trust banks have historically provided Japanese asset owners with many of the services now being offered by OCIO managers, and many Japanese corporate pensions already delegate large portions of portfolio management to trust banks through segregated mandates or advisory structures.

With government reforms pushing asset owners away from traditional approaches and toward more professionalized and formalized OCIO arrangements, it will be interesting to watch the evolution of the market in the coming months and years to see who comes out on top of the OCIO game: trust banks who already have incumbent partnerships with Japanese asset owners, consultants who see OCIO as a way to expand their franchises with high-margin business, or asset managers looking to protect, and hopefully grow, AUM and revenue bases.

Tomomi Shige, Parijat Banerjee, and John Feng advise our investment management clients in Japan.

Methodology

From April through October 2025, Crisil Coalition Greenwich conducted interviews with 255 of the largest corporate pension funds, public pension funds, financial institutions, and endowments and foundations in Japan. Total reported fund assets were ¥517 trillion. Senior fund professionals were asked to provide quantitative and qualitative evaluations of their investment managers, qualitative assessments of those managers soliciting their business, and detailed information on important market trends.

Asset tokenization can make transfers easier and faster and, by doing so, allow capital to be more efficiently and effectively put to work. While we are still far from truly programmable financial assets (e.g., automated dividends or coupons through smart contracts) with instantaneous settlement, we are slowly moving down that path. The SEC’s no-action letter supporting the DTCC has put the industry on a dynamic path where the potential benefits of tokenization are starting to impact markets in a real way.

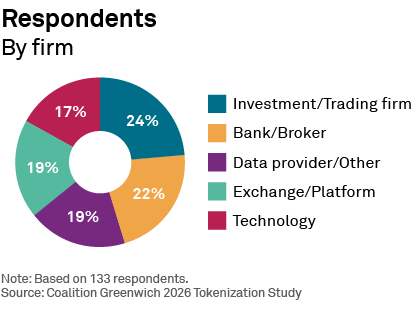

To get a deeper sense of sentiment within the capital markets, Crisil Coalition Greenwich asked our network of market participants about the benefits of tokenization, which asset classes will benefit the most, and where tokenized assets should trade. Over 130 market participants at banks, exchanges and platforms, investment and trading firms, data providers, and technology firms offered insights into what’s real, what matters and where decentralized finance (DeFi) is headed.

Not all tokens are the same

First, some definitions. Not all “tokenized assets” are the same, and it is important to distinguish among them.

- Some tokens are economically linked to an underlying asset but are not the asset itself, as they function like a derivative or structured claim (for example, a token that represents a claim on a special purpose vehicle (SPV) that custodies the asset), so the token holder ultimately bears counterparty risks in addition to any market risk.

- Second, others operate as twin tokens, referring to assets that remain recorded on a separate system of record (such as a ledger at a securities depository). In this model, the token is best understood as a digital representation or receipt, while the underlying asset’s ultimate ownership record remains off-chain.

- Third, in native security tokenization, the token is the asset. The on-chain ledger is the authoritative record of issuance and ownership (with the possible involvement of a transfer agent to offer a snapshot off-chain). Thus, transferring the token is transferring the security itself (for example, a digital municipal bond recorded and settled on-chain with the same legal rights as the conventional instrument).

As we move into the future, many tokenization initiatives are aimed less at creating new wrappers and more at migrating the same asset with the same ownership rights onto a blockchain-based infrastructure (issuance, transfer, and settlement) so that the blockchain becomes the primary system of record rather than a parallel representation.

Assets that are always on

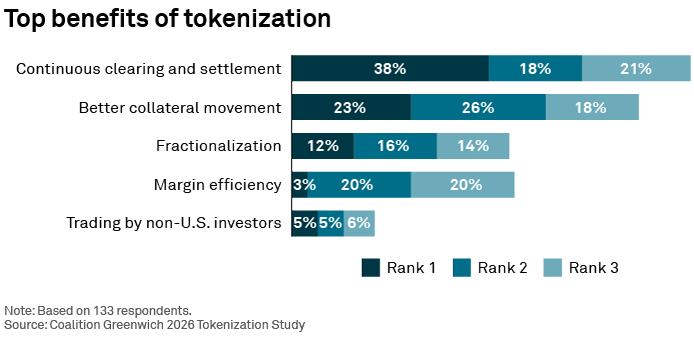

Our study participants overwhelmingly view the benefits of tokenization not in trading, but in post-trade operations. Through a continuous clearing and settlement model, tokenization can improve capital efficiency. Moreover, collateral can move swiftly and transparently. For instance, Tradeweb recently moved collateral (U.S. Treasuries and U.K. gilts) outside of traditional market hours via the Canton network to support repo transactions.

Tokenization creates an environment where assets are always on. Continuous settlement allows for 24/7 movement of assets and opens up greater possibilities for extended market hours and improved settlement windows, which has proven to be one of the biggest catalysts behind the growth of tokenized U.S. Treasuries and money-market funds. If you get a margin call on the weekend when the banking system is closed, tokenization allows you to fund your account immediately.

Always-on assets, including cash, allow for margin efficiencies as well, hence CME’s partnership with Google to tokenize cash and other assets used as collateral.

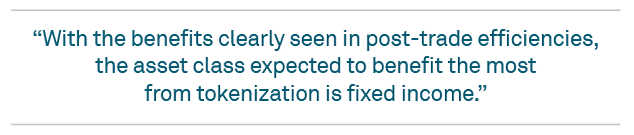

The great unlock: Fixed income tops the list

With the benefits clearly seen in post-trade efficiencies, the asset class expected to benefit most from tokenization is fixed income. Today, U.S. fixed income assets, particularly U.S. Treasuries, back much of the global stablecoin industry. Moreover, these assets are heavily utilized and widely acceptable as margin for derivatives. And while the U.S. Treasury market is considered one of the deepest and most liquid in the world with trading occurring nearly 24/5, the ability to transfer assets overnight (rather than trading with another counterparty) or on the weekend could be hugely beneficial to market participants over time, including by reducing settlement time and offering new settlement windows.

U.S. equities: Trading vs. transfer

While tokenized U.S. equities are growing in popularity, we may still be very much in the early stages for institutions in the United States. For many, the U.S. equities market structure works well. In the front office, traders and portfolio managers don’t necessarily see a need for tokenization and will continue trading U.S. equities as usual.

At the same time, non-U.S. investors might see trading tokenized shares as a way to extend their trading windows. They may also see equity perps (perpetual futures, e.g., via Ondo) as a good way to get exposure to U.S. price action. They may be willing to accept some counterparty risks or technology risks to do so. For instance, Texture Capital and Securitize are firms focused on bringing tokenized versions of companies on-chain, using well-known methods such as transfer agents and alternative trading systems (ATSs).

However, we believe the majority of the U.S. market will want the actual legal ownership, rights and support from the DTCC to enable them to participate in the inherent opportunities available on-chain. The token will entitle the owner to the same rights as if the asset were at DTCC—tokenized shares will have the same ticker symbols and CUSIP numbers as traditional shares, allowing them to be interchangeable.

However, the DTCC is proposing a sub-ledger system, so the transaction can be reversed by DTCC if needed, making this not DeFi. To be fair, neither the Nasdaq nor ICE proposals are fully fleshed out, and we expect developments throughout 2026.

Trading may bring another twist—some traders might prefer trading the tokenized shares using a FINRA broker and through Reg NMS-compliant methods (Nasdaq/Kraken, Dinari and ICE are focused on this). Others will simply want to be able to transfer those shares on-chain as collateral through a FINRA broker for stock lending.

Where assets trade vs. where they simply move

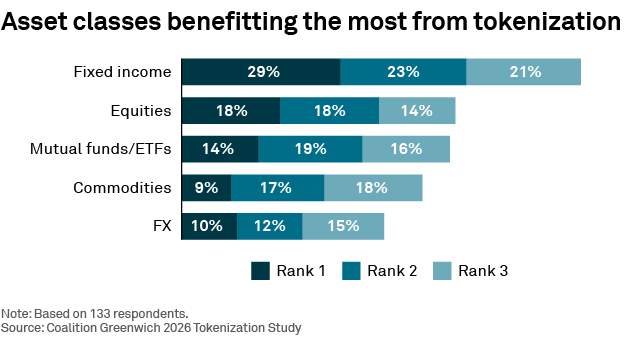

While tokenized assets will bring post-trade efficiencies, most institutional market participants are currently apprehensive about changing their trading workflows to handle these instruments. That largely explains why market participants want tokenized assets to trade on the regulated markets they already know. Securities exchanges (i.e., LSEG, Nasdaq, NYSE) top the list of where market participants think tokenized assets should trade. Derivatives exchanges (i.e., CME Group, ICE) and multidealer platforms (i.e., MarketAxess, Tradeweb) come through as a strong second choice.

The current reality suggests the tokenized versions of U.S. equities will trade via exchanges and ATSs, and bonds. While the story is different for crypto-native investors looking to do everything in an on-chain world and DeFi apps, or with some investors outside the U.S. (e.g., APAC), capital markets professionals want known partners to remain intact, while still getting the post-trade benefits. At the same time, the expertise of crypto platforms will be extended into the traditional exchange groups via licensing and partnerships (i.e., Kraken and Nasdaq), but we believe the same venues will remain for most U.S. institutional investors.

U.S. government pivot

The U.S. government has become much more receptive to the direct and indirect ownership of cryptoassets. But our research suggests the more meaningful development is the growing support for the issuance and management of traditional financial assets on a blockchain or distributed ledger infrastructure. Put another way, the key point is not that investors can now easily buy a Solana ETF, but that they can hold conventional assets (such as bonds or equities), directly on blockchain-based platforms.

For instance, this approach enables investors to own traditional shares on a blockchain while retaining all associated rights, including full ownership, dividend entitlements, and the ability to transfer these shares to other whitelisted wallets or approved investors. In this model, the blockchain serves as the foundational infrastructure for recording, transferring and servicing traditional securities, rather than functioning solely as a platform for crypto-native assets.

Why should you care? We believe tokenization will reduce the amount of idle capital moving forward. The ability to transfer these assets instantaneously and/or post them as collateral is going to be a potent force for positive change. Moreover, we also expect to see traditional capital markets and blockchain infrastructures become much more interconnected, in the same way that payment networks are being connected with stablecoin networks. As the capital markets industry progresses, traditional financial assets will be more readily available for DeFi applications, such as securities lending or collateral for lending or repo.

David Easthope is a senior analyst on the Market Structure & Technology team.

Methodology

In February 2026, Crisil Coalition Greenwich conducted research to better understand tokenized asset market structure, including the demand for tokenized assets, their main benefits and the likely location for trading purposes. We interviewed 133 market professionals at banks and brokers, exchanges and platforms, investment and trading firms, data providers, and technology firms in North America and U.K./Europe.