Share

Share

Executive Summary

The evolution of buy-side front-office trading technology continues. Providers of order management systems (OMS), execution management systems (EMS) and portfolio management systems (PMS) are continuously updating their capabilities and product coverage in an effort to keep up with increasing client demand.

Methodology

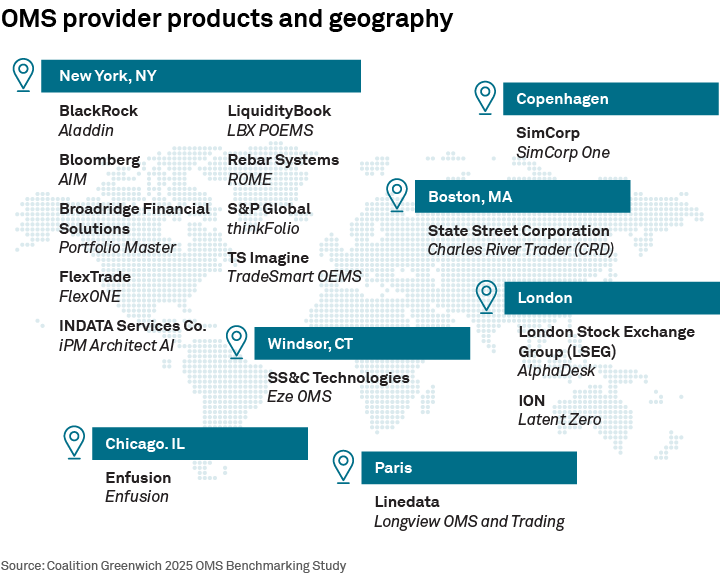

Throughout the second and third quarters of 2024, Crisil Coalition Greenwich collected data from 14 OMS solutions providers to better understand current offerings and what to expect in the next two to three years. OMS were analyzed to assess core system capabilities, competitive differentiators, roadmap plans, support and resilience models, and more. Eleven of the firms included in our study are based in the U.S., while four are headquartered in Europe/the U.K.

The evolution of buy-side front-office trading technology continues. Providers of order management systems (OMS), execution management systems (EMS) and portfolio management systems (PMS) are continuously updating their capabilities and product coverage in an effort to keep up with increasing client demand. As a result, OMS, EMS and PMS distinctions are blurring, creating confusion among users. Portfolio managers (PMs) and traders are left wondering what the differences are between systems, which solution is best suited for their investment strategy and workflows, and whether the current tech stack is still the right fit.

In this report, Crisil Coalition Greenwich provides deep insights into the core capabilities offered to buy-side managers by 14 OMS providers. The goal of this research is to equip users with information that aids in the choice of solutions to enhance and future-proof their business. The research examines:

- Buy-side user demand: Current market dynamics are pushing PMs to find new ways to generate returns and traders to improve execution quality. We also explore needs associated with investment in new markets and products and how that translates into OMS technology demands.

- Current OMS offerings: An overview of the OMS providers in our study focuses on the “DNA” of offerings, client segments and primary geography using the solution, product coverage, as well as several other important features buy-side users must consider before investing in a solution.

- The future state of OMS solutions: The OMS provider roadmap summarizes the capabilities in development for 2025. We explore in detail the many different ways providers are responding to demands for innovation to help users achieve their investment goals.

Buy-side needs drive OMS evolution

Generating alpha and increasing efficiency remain top-of-mind for buy-side professionals in this era of hyper competition and shrinking investing fees. New strategies often incorporate a variety of different products in several regions and asset classes. These investment ideas can only be successful with the right infrastructure to handle portfolio challenges, best execution and operational workflows. As such, investment in an OMS that can accommodate more complex strategies serves as a differentiator.

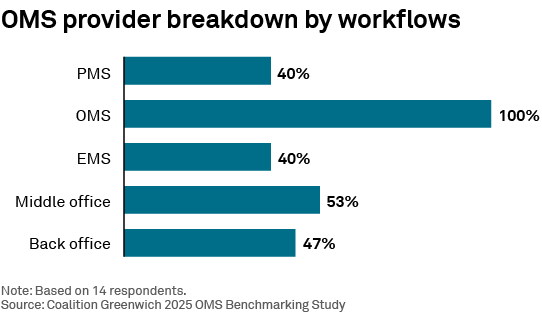

OMS systems are becoming more front-to-back and now often include EMS and downstream capabilities. This trend has emerged over the past few years and continues to develop. While some managers need very asset class-specific features and functionality, many firms stand to benefit from combined solutions and broader functionality. For example:

- Company size matters. Smaller funds and startups may wish to rely on a front-to-back solution that includes front office functionality, accounting/IBOR workflows, post-trade reconciliation, and reporting modules. Having one system to support is less strain on limited IT resources. The trend toward more SaaS (software- as-a-service) solutions, hosted capabilities (including FIX network connectivity) and compliance continues.

- Trading volumes and business models are a factor. Larger and more complex firms with numerous subaccounts that trade a variety of global asset classes may benefit from broader solutions with more front-to-back capabilities. Deciding factors often boil down to the adequacy of the solution. For instance, combining the functionality to create what-if investment scenarios across the portfolio that include hedging and cash or collateral management with the ease of embedded execution tools is attractive. From a support and disaster recovery (DR) standpoint, fewer systems to support may decrease complexity and cost.

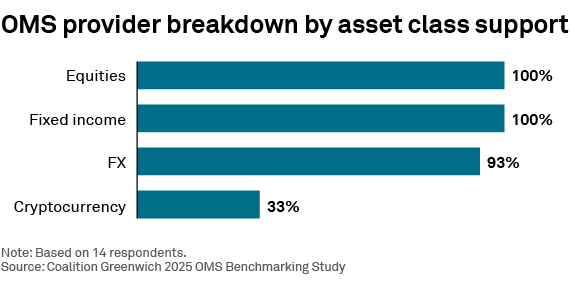

- Business decision-making shapes OMS solution choice. Often, system choice is in the hands of compliance, the C-suite and other leaders looking to get more bang for their buck, fewer contracts and vendors to manage and approve as well as other efficiencies. When this happens, broader front-to-back solutions may take precedence. OMS solutions with consistent yet flexible capabilities across multiple products and asset classes offer competitive advantages-especially as newer products like cryptocurrency are added to the portfolio.

- Integration with other technology is a top consideration. Integration need is pushing managers to select OMS provider firms with broad networks and solid partnerships. Solutions with a larger number of these touchpoints all along the trade life cycle help close some of the data and other workflow gaps created by the cobbling together of different technologies. Of course, the complexity inherent in replacing legacy software creates a huge roadblock to putting the perfect solution in place.

The OMS solution provider landscape

Three-quarters of the OMS providers analyzed in our study are based in the U.S. with the remainder in Europe and the U.K. While in some cases headquarters are less about the location of clients and more about where the founders are from, the heavy concentration in U.S. does reflect the importance of that revenue pool for OMS providers. But as we will discuss later, the next phase of growth is likely elsewhere.

OMS adoption by user type, location and size

OMS providers are characterized by a number of client attributes. We primarily examine OMS users by the following categories:

- SegmentGeography

- Assets under management (AUM)

- Use cases/strategies

- Workflow need

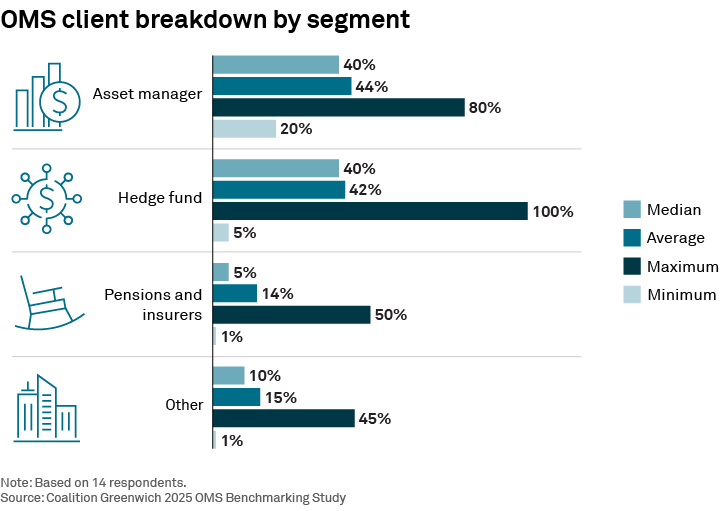

Clients’ needs vary by each segment. In many cases, one type of client, such as an asset manager or a hedge fund, will dominate an OMS’s client base as some solutions are specialized to cater to a particular segment’s needs. In most cases, vendors are expanding their reach by segment, geography and AUM profile.

Expanding to new segments is important to providers. For instance, many that started out offering services to hedge funds have grown their capability set to attract more traditional asset managers. Likewise, the addition of large insurers and pension funds has also been a key goal.

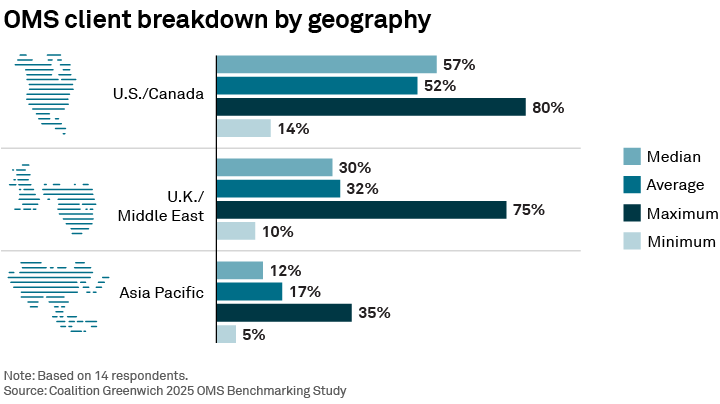

Geographically, the push to break into new regions is in full swing. Most providers in our study have a client base that is predominantly in the U.S. and Europe, with growth in Asia still aspirational. Looking ahead, OMS providers will expand globally as their clients do, which ultimately allows them to attract local investors in these new markets (i.e., Asia and emerging markets broadly), and thereby helps improve their global reach.

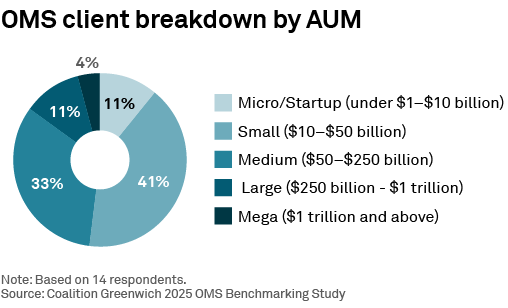

Size-wise, the market “sweet spot” of client AUM ranges from $10 billion to $250 billion and is made up of firms that require an OMS but may not be large enough to efficiently build and maintain systems in-house. While there are, of course, larger users in the mix, there is a trend toward attracting underserved smaller AUM firms through easy to deploy SaaS-based and managed-services solutions. While generally aimed at the $100 billion and under manager, such deployments are slowly but surely working their way into larger organizations.

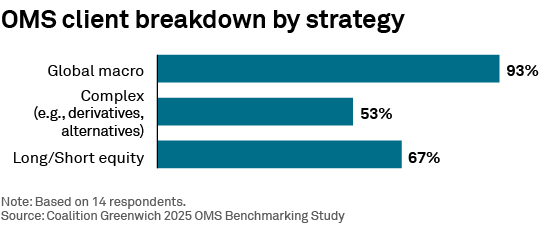

The majority of OMS providers support global macro investing, following market-wide trends and the adoption different versions of that strategy. Traditional long/short equity strategies are also commonly supported, as these were a core focus of the OMS pioneers 30 years ago. More recently, complex derivative strategies have grown and are becoming a niche focus of several OMS providers. Hedge funds and asset managers are increasingly looking to derivatives, securitized and structured products as important elements of the portfolio to generate alpha.

The future of OMS solutions

Vendors in our study indicate roughly 20% or more of their product revenue is invested in R&D associated with their platforms. While some of this investment targets advanced technologies such as AI/ML, the majority is going to less exciting but more mission-critical system enhancements.

What are OMS providers focused on building now?

As mentioned, systems are getting bigger and are becoming more front-to-back than ever before. Professionals at buy-side firms are gravitating toward multi-asset class solutions. The management of workflows, including books of record, compliance checks, audit trails, and other downstream capabilities, are changing the look and feel of vendor OMS solutions.

Where the OMS and EMS meet

We also found nearly all OMS vendors offered at least some EMS-like capabilities. Typically, this includes integration with algo and broker wheels (primarily for equities) and other execution management functionality across asset classes. In some cases, more advanced functionality, including pre-trade transaction cost analysis (TCA), actionable indications of interest (IOIs), price snapping, and other features, are also part of the solution. Execution functionality for bonds and digital assets are a popular topic, but are still early days with some few exceptions.

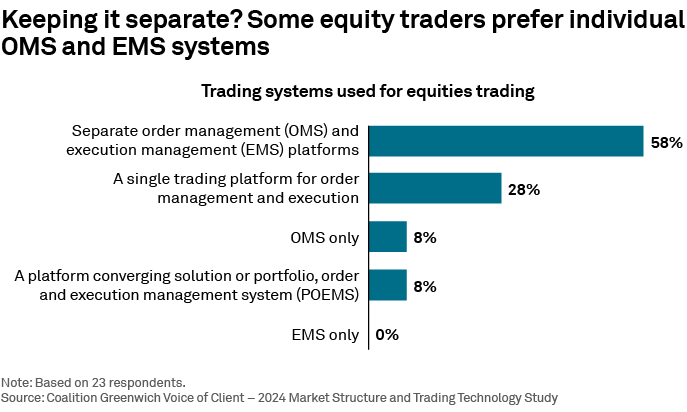

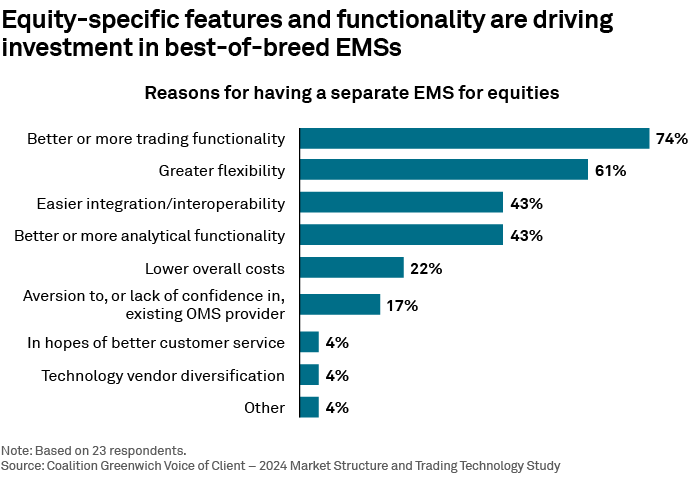

Despite these developments, we found that many equity traders are keen to keep OMS and EMS solutions separate (even though almost 30% want combined solutions-a figure we expect to increase over time). Why might this be the case?

Equities trading in particular is mature enough to garner very specific requirements. Thus, the flexibility of an advanced solution is key. Integration is also an important element. Advanced analytics like pre-trade TCA, broker selection and algo selection tools are becoming more necessary to achieve best execution and gain an edge-which rationalizes why nearly all OMS providers in our study are adding these capabilities and more.

Solutions in the fixed-income market are still evolving. Our research in 2024 found that roughly 10% of bond investors currently have an EMS, with many deciding that the staging and execution functionality built into their OMS is good enough. Our research does suggest that buy side professionals must increasingly focus on execution automation in the bond market, which means new technology is required for nearly everyone. Whether that will ultimately come packaged in an OMS, EMS or directly into the trading venue front end remains to be seen.

OMS solutions are also becoming increasingly modular, open and customizable. Buy-side PMs and traders have a range of choices and possibilities when considering a broader and more front-to-back solution versus connecting parts of several systems to create optimal workflows and functionality. This helps providers gain a competitive advantage as users don’t always have the time, money and staff to manage system integrations. As a result, many clients will start off using a portion of the full offering then gradually bolt on another bit of the same vendor’s technology rather than trying to piece together disparate systems.

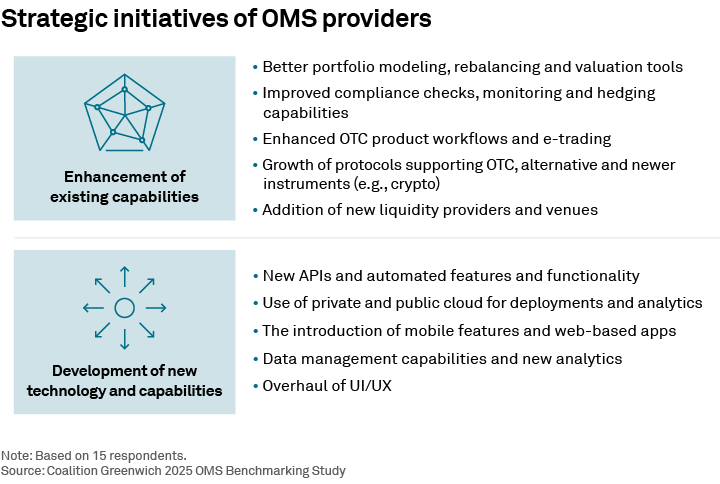

Growth and development of current offerings

Most OMS providers rely heavily on adding to existing capabilities like portfolio modeling tools, compliance and third-party connections to provide best-in-class functionality that keeps up with client needs. In many cases, OMS vendors are seeking and establishing partnerships-for instance, with data or advanced technology providers-to add necessary technology versus developing it in-house. As a result, improved integration of systems up- and downstream is still paramount and sits squarely on the priority list.

Enhancing workflow capabilities such as real-time compliance checks and other supportive capabilities are also important to OMS users. In addition, product or function-specific enrichments are evolving and include improved hedging, trading tools and portfolio management functionality.

Investment in new tools, technology and functionality

Many vendors are going beyond spot improvements and are modernizing their solutions. Advanced technology is a relatively small but growing area where R&D budget is being spent. Several OMS vendors are keen to add open APIs and automation to their platforms. More cloud-native offerings are also being created to deploy version-less updates and enable faster data crunching and output.

New ways of consuming information using mobile capabilities and the introduction of new web-based apps are on the horizon. Some vendors are also adding data management capabilities and new analytics like pre-trade TCA and liquidity tools. Meanwhile, overhauls of systems to create better UI/UX is an over-arching theme which surfaced in this study. Humans clearly remain the ultimate end-user despite the race to add more automation.

Conclusion

The evolution of the OMS is happening quickly as providers continue to add new and improved functionality to address changing needs of buy-side professionals. While vendors often build new bells and whistles on top of existing technology, shifts to more modern tech stacks that include the cloud, workflow automation and APIs are happening at a rapid pace. As a result, OMSs are becoming more front-to-back and increasingly modular to support buyside need.

PMs and traders are tasked with distilling differences between providers while weighing the adequacy of current systems. Often this can be confusing, as the lines between OMS, EMS and PMS offerings become more and more blurred. This study addresses these differences to aid in the choice of solutions to enhance and future-proof businesses by analyzing trends and other factors influencing buy-side user demand, current OMS offerings and the future state of OMS technology.

Audrey Costabile advises on market structure and technology globally.