Share

Share

Executive Summary

The derivatives market is vital to the financial system. It allows market participants to manage and hedge risks, generate alpha and, more generally, helps them achieve their goals.

Methodology

This report is based on interviews conducted between February and May 2025 with 38 senior derivatives market participants in the United States, including clearing brokers, executing brokers and the buy side. The research was designed to identify key trends in margin and collateral. Questions explored the views on cross-margining, the drive to optimize collateral, and how firms will respond to new market drivers, such as U.S. Treasury and repo clearing

In recent years, the margin and collateral landscape has come back into the spotlight and is continuing to evolve. The industry most recently focused on Uncleared Margin Rules (UMR) and other such regulations. Those were mandatory, compliance-driven changes.

Today, the market-driven cost of capital is taking center stage. As funding costs increase, it heightens sensitivity around the cost of deploying collateral. Therefore, managing and mitigating collateral costs has become a strategic imperative requiring firms to evaluate their activity across all derivative types and counterparties.

Introduction

There are various factors to consider when trading derivatives: complex operational workflows, increased leverage, ability to source liquidity (depending on the instrument), as well as the cost of sourcing collateral to meet margin requirements. Neither the buy nor the sell side can solve the margin issues on their own. They are dependent on the other organizations in the workflow to provide solutions. Central counterparties (CCPs) recognize this demand and have made strides to help mitigate costs while maintaining their stringent risk-management standards. More specifically, enhancing their cross-margining capabilities to increase offsets is a major benefit to the trading desks they serve.

Margin and collateral: Managing the costs

Margin is an important consideration for traders and investors in both over-the-counter (OTC) and exchange-traded derivatives. As a risk-management function, margin helps mitigate counterparty credit risk. From an operational perspective, it requires interoperability across multiple systems as well as processing and oversight. As a cost, it is an expensive obligation that needs to be addressed.

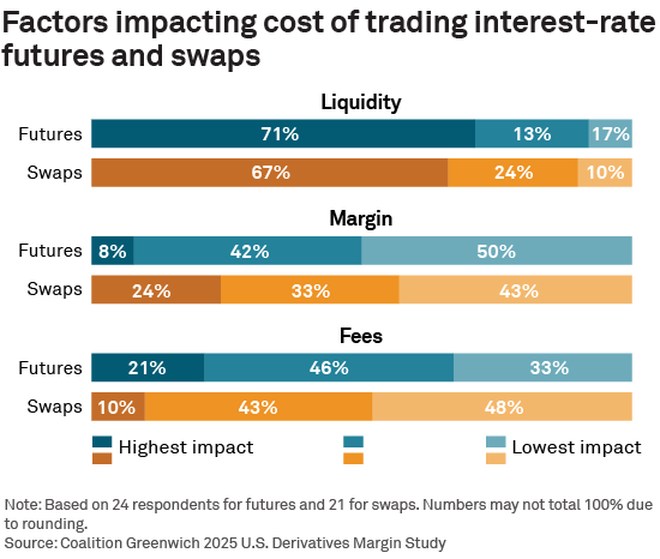

There are different considerations when evaluating which derivative instrument to trade, whether to clear it, and where to clear it. Different instruments have different counterparty credit risk, and each has its own margin and collateral regime that governs how much and what type of collateral must be exchanged. When asked to rank the impact of liquidity, margin and fees, respondents stated that liquidity costs were most impactful for both futures and swaps, but differences emerged when analyzing margin. For example, the margin period of risk (MPOR) is highest for uncleared swaps, lower for cleared swaps and lowest for futures. The resulting collateral calculations reflect this, which largely explains why swaps traders see margin as having a bigger impact on their total cost of trading than futures traders.

Derivatives desks look to manage the costs over which they have the most control. While liquidity costs can be managed to some extent via ongoing transaction cost analysis (TCA), potential margin savings present an important opportunity. The ability to lower margin costs is greatest when trading instruments with offsetting risks, assuming that the instruments are cleared and can be cross-margined in an efficient way. It is certainly a balancing act; offsets are not the sole reason to clear through a particular CCP, but our research indicates that it is becoming an increasingly important consideration.

In fact, as innovation at CCPs and futures commission merchants (FCMs) increases, the opportunity to strategically optimize margin across an entire derivatives book increases. Years of analysis by derivatives market participants have finally driven many to action, utilizing margin offsets for both cleared and OTC derivatives in ways they had not or could not in the past. This is true across instrument types, currencies and geographies. Yet despite the real savings experienced today, untapped opportunity still exists.

Strategies for mitigating collateral costs

Collateral desks can employ different strategies for helping manage margin costs. For some, that may mean using a collateral optimization algorithm when selecting collateral. This approach does not affect the amount of collateral owed; rather, it determines which collateral is cheapest to deliver to a particular counterparty. For instance, selecting cash or a particular U.S. Treasury bond based on the fund’s current holdings, interest rates and other factors will help mitigate some—but by no means all—collateral costs.

In addition, one can look to find offsetting positions and cross-margin those positions against each other. According to our research, this method holds great appeal and potential for the industry. Ninety-four percent of those with a view believe there are margin savings that can be realized between their USD interest-rate swaps and USD futures. For that 94% to be proven correct, the instruments will need to be cleared with the same FCM, either at the same CCP or at separate CCPs with a cross-margining arrangement. For some, this can be achieved through operational changes. For others, it would require changing where they clear certain activity.

For a desk with its margin and profitability always under a microscope, it is vital to realize these savings.

The changing influence of the CCP basis

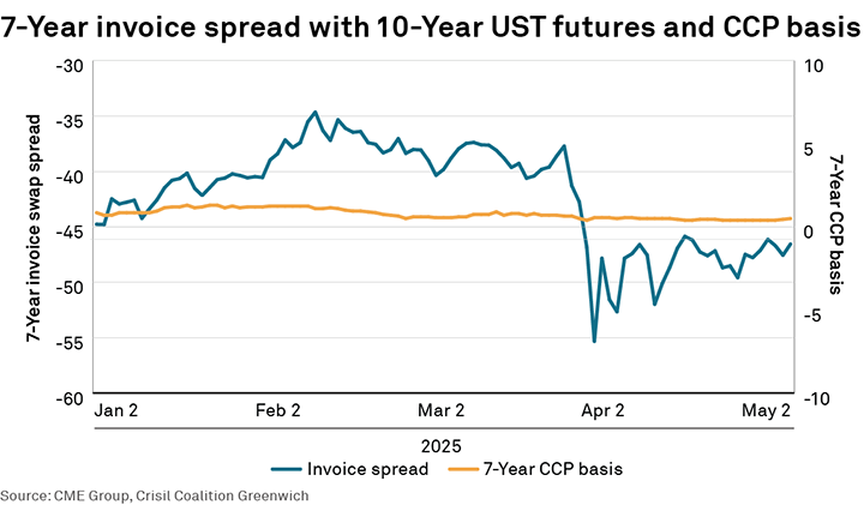

A CCP basis is the price differential between identical swaps contracts cleared at different CCPs. This basis can be impacted by differing collateral costs, positioning, and netting opportunities between the CCPs. In particular, pricing differences between USD interest-rate swap contracts cleared at LCH compared to CME Group remain a market focus. For some, the size and volatility with this basis drove participants to clear a majority of USD swaps at LCH. Recently, however, the CME Group - LCH basis has narrowed and become less volatile, which could change the equation.

The CCP basis between CME Group and LCH has been stable in recent months, despite the significant volatility in the market as evidenced by the 7-Year invoice spread (a trade involving a U.S. Treasury future and an interest-rate swap with similar risk profiles). Swap spreads moved more than 15 basis points due to the whirlwind of tariff announcements, culminating in the April 2025 Liberation Day. Yet, the basis remained relatively flat. As recently as a few years ago, this sort of market volatility would likely have affected the CCP basis. The correlation breakdown between the CCP basis and market volatility today, however, suggests that the cost of the basis may be more than offset by the savings available from cross-margining.

This new dynamic of the CCP basis may change how market participants determine where to clear. Our research confirms that derivatives market participants are willing to clear swaps and futures at a particular CCP if margin savings exceed the costs of hedging the basis. This implies that the influence of margin costs is rising, while the influence of the CCP basis is diminishing for some. Should the basis re-emerge as an important consideration, the calculation could, of course, change.

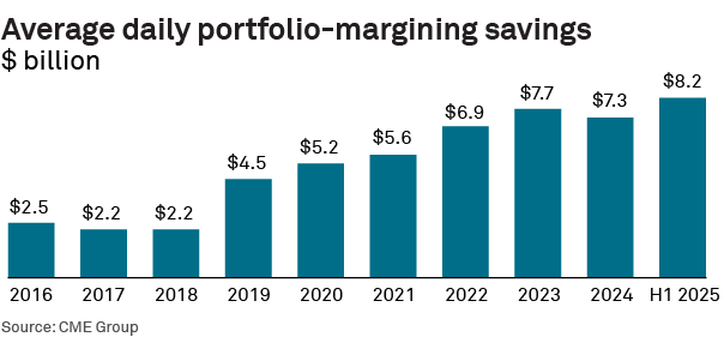

Driven by the market’s increasing desire to express views on swap spreads in a capital-efficient manner, the use of cross-margining between swaps and futures has been increasing. As demonstrated by data from CME Group in the following chart, savings from their portfolio-margining program between swaps and interest-rate futures and options on futures set a record in the first half of 2025, up approximately 12% from the daily savings realized in 2024

The $8.2 billion in average daily savings is realized across multiple currencies, but approximately 90% of these portfolio-margin savings are driven by USD swaps and USD interest-rate futures and options, confirming that these offsets are considerably greater than those available between different swap currencies. This also demonstrates participants are understanding that the amount of potential savings may be enough to overcome the impact of the CCP basis.

While an individual desk’s savings will vary based on the exact composition of its portfolio, cross-margining’s potential is notable. Not surprisingly, correlations within USD-denominated products are significantly higher and, thus, provide greater opportunities as compared with products of differing currencies. Given that U.S. interest-rate futures and USD interest-rate swaps are predominantly cleared at different CCPs, firms will need to re-evaluate where they clear these instruments in order to realize that potential.

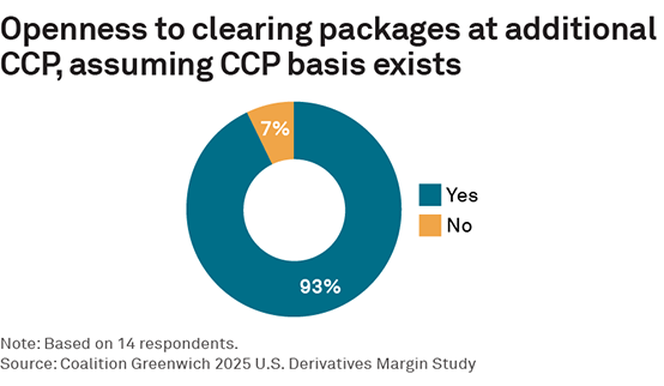

Crisil Coalition Greenwich research, along with data from the largest CCPs, shows that offset opportunities can and are being realized today. But if assets that can theoretically be offset with each other are cleared at different CCPs, there will be a ceiling on the benefit. Despite cross-margining records being set, not everyone has changed their behavior, implying there is more cross-margining growth potential. But there is an interest in making these changes.

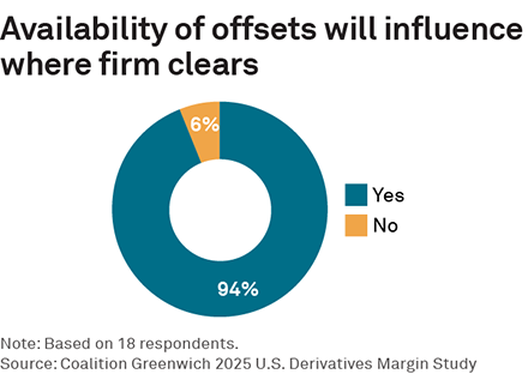

An impressive 93% of derivatives professionals are, in fact, willing to change where they clear if the margin offsets are greater than the CCP basis. This willingness is not simply a matter of onboarding a new CCP (which is not always simple). This next step will require a more systematic approach to clearinghouse selection, with traders and portfolio managers directed to instruments that will achieve their return goals while simultaneously reducing their margin costs. Competition in clearing is good, but consolidating offsetting positions into a single CCP with a single FCM often unlocks the biggest margin savings.

As clearing increases, so does the need to optimize offsets

The pace of change in derivatives clearing ebbs and flows, and is by no means static. Immediately after the financial crisis, significant changes were made that took years to implement, followed by additional years to develop strategic responses. Mandatory clearing of U.S. Treasuries and repo is now ushering in the next wave of change. Our recent research into the clearing of Treasuries and repo revealed that 70% of derivatives market participants believe the most important attribute of a U.S. Treasury and repo clearinghouse is “cross-margining efficiencies.” (For a deeper discussion, please see U.S. Treasury clearing: A new timeline and uncertain trajectory.)1

This SEC mandate may open up a new chapter in the history of cross-margining. Clearing offsetting swaps together is great, swaps and futures even better; but add in repo and cash Treasuries alongside swaps and futures, and the efficiencies are nearly impossible to ignore. Getting to this ultimate end state will likely take years, particularly given the fact that client repo and Treasury clearing remains in its infancy. But the result will be a safer, cheaper and more efficient fixed-income market.

Conclusion

Bringing as many of the products that require margin into the cross-margining equation will both help market participants manage costs and potentially reduce their margin requirements overall—and 94% of respondents are willing to make changes to go in that direction.

CCPs understand this and have responded. CME Group maintains a cross-margining agreement with DTCC’s FICC, covering cash and derivatives instruments, and they also have plans to roll out the CME Securities Clearing (CMESC) offering, which will help extend cross-margin opportunities with derivatives into the cash fixed-income market. LCH has responded by partnering with FMX to offer cross-margining between its cleared swaps and FMX’s newly launched Treasury futures.

Aligned incentives for market participants and CCPs is strong evidence that mitigating margin costs is and will remain a strategic imperative in the years ahead, as initial margin requirements are expanded to a broader universe of products.

Stephen Bruel is a Senior Analyst on the Market Structure & Technology team.

1U.S. Treasury clearing: A new timeline and uncertain trajectory