The Portfolio Margining Imperative for Interest-Rate Derivatives

Share

Share

Executive Summary

Derivatives market participants have renewed their focus on capital and margin optimization in response to the high cost of capital and a regulatory push toward central clearing. Much progress has been made via compression efforts, collateral selection algorithms and improved pre- and post-trade analytics. However, one of the biggest opportunities for margin optimization remains largely untapped. Margin sits in the clearinghouse where the trade is cleared. Separate exposures within a clearinghouse may be eligible for margin offsets, but these same exposures sitting in different clearinghouses are not. Margin offsets between U.S. dollar (USD) interest-rate futures and USD interest-rate swaps, two highly correlated products, are largely left on the table today, as CME clears nearly all U.S. Treasury (UST) and SOFR futures trades and LCH nearly all USD interest-rate swaps trades. FMX, a newly launched exchange, offers trading in UST and SOFR futures contracts with clearing at LCH. This new product offering has reinvigorated talk of portfolio margining and the potential savings available to industry participants if they clear their futures and swaps positions in one place. This research, conducted in Q3 2024, examines trends in the interestrate derivatives market, the opportunity for USD interest-rate market participants to reduce their costs through portfolio margining, and how the FMX/LCH offering aims to disrupt the competitive landscape.

Methodology

This report is based on an analysis conducted by Coalition Greenwich utilizing industry data on margin pools and interviews with market participants in the U.S. and U.K. to help determine the potential offsets enabled by this new FMX/LCH partnership. The report also utilizes data from Greenwich MarketView and data from U.S. and U.K.-based clearinghouses. The analysis examined scenarios involving trading strategies with different maturities and directions to highlight how those changes impact potential margin savings.

Executive Summary

Derivatives market participants have renewed their focus on capital and margin optimization in response to the high cost of capital and the regulatory push toward central clearing. Much progress has been made via compression efforts, collateral selection algorithms and improved pre- and post-trade analytics. However, the largest opportunity for margin optimization remains largely untapped.

Margin sits in the clearinghouse where the trade is cleared. Separate exposures within a clearinghouse may be eligible for margin offsets, but these same exposures sitting in different clearinghouses generally are not. Margin offsets between U.S. dollar (USD) interest-rate futures and USD interest-rate swaps, two highly correlated products, sit without margin offset today, as CME clears nearly all U.S. Treasury (UST) futures and SOFR futures trades and LCH clears nearly all USD interest-rate swaps trades.

FMX, a newly launched exchange, offers trading in SOFR futures and soon, UST futures, with clearing at LCH therefore providing cross-margining opportunities between USD interest-rate swaps and UST and SOFR futures. This new product offering has reinvigorated talk of portfolio margining and the potential savings available to industry participants when they clear their futures and swaps positions in one place.

This research, conducted in Q3 2024, examines trends in the interestrate derivatives market, the opportunity for USD interest-rate market participants to reduce their capital costs through portfolio margining, and how the FMX/LCH offering aims to disrupt the competitive landscape.

Introduction

“The U.S. Treasury market is the most liquid in the world.” That statement is frequently expressed across all forms of media, in academia and beyond. The popularity of the sentiment does not diminish its validity, but the story goes much deeper than those words suggest.

U.S. Treasuries are vital to the global financial system but do not stand alone. Derivatives markets tied to government bonds and other securities often play an equally important role helping market participants access the market, hedge risks or enhance returns. U.S. Treasuries are a noteworthy example of this relationship, and the role of UST futures, SOFR futures and USD interest-rate swaps is vital. The inherent leverage in these futures and swaps products only increases their utility.

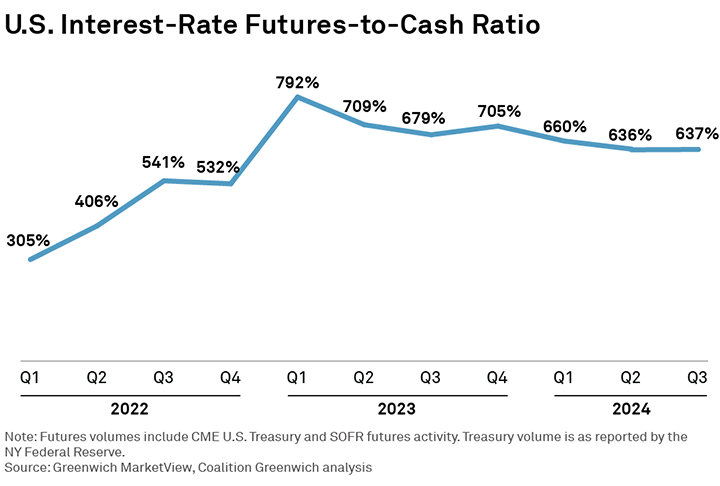

In fact, the liquidity and trading volume of UST futures alone can often match or surpass the bond market. For instance, UST futures volumes average over 80% of the volume in the underlying bond market in most quarters, and with SOFR futures volume included in the calculation, futures traded an astonishing 6 times more in 2023 than the underlying cash Treasury market.

But while the derivatives market acts as a key support to the cash market, it also introduces different challenges to participants. Due to the way derivatives trade and settle, they expose participants to more forms of risk, including counterparty credit risk. To mitigate this risk, banks must hold capital, exchange collateral with counterparties and post margin at clearinghouses for nearly all futures and most USD swaps positions.

This collateral, mostly in the form of clearinghouse margin, dramatically reduces risk in the system. This risk reduction creates direct costs for market participants, particularly when they must post collateral at different clearinghouses even when holding offsetting positions (i.e., a buy and sell of similar exposures do not cancel each other out).

Given the prevalence of market participants holding both U.S. interest-rate futures (which include both UST and SOFR futures) and USD swaps, a significant opportunity exists to reduce margin requirements (and costs) by consolidating those positions in a single clearinghouse. Netting of futures and swaps risk in a single clearinghouse would also reduce the potential for market participants being stopped out due to margin increases from volatility spikes. Not only would individual trading entities benefit, but the financial system would see an improvement in risk efficiency. Limited portfolio margining opportunities are available to market participants today (USD interest-rate futures and swaps positions are cleared separately in most instances), reducing portfolio margining efficiency and scale. As such, portfolio margining has room to grow.

Capital, clearing and collateral are all compelling derivatives market participants to be more strategic about how they optimize their margin obligations, driving changes to where they trade, and how and where they clear the instruments. The industry has not made progress in bringing swaps and futures margin pools under the same roof. But this is a vital issue—the lack of margin offsets can impact a bank’s individual capital allocation decisions, constraining capacity.

New Competition, New Focus on Margin

FMX, which already provides a platform for cash UST and FX execution, recently launched its futures exchange for SOFR futures, with UST to follow in Q1 2025. FMX will not directly clear the trades; rather, they have entered into a partnership with the London Stock Exchange Group’s LCH (which is fully licensed with the CFTC as a Derivatives Clearing Organization to clear both futures and swaps), who will clear the trades through LCH’s Listed Rates service. One rationale behind the partnership is to help resolve capital issues, a top-of-mind industry concern. According to Coalition Greenwich research, 88% of bank respondents agree that “capital efficiency through netting and margin optimization” is “very important” to how they measure their relationship with a central counterparty (CCP). Further, Bank of America research found that margin accounted for 76.7% of the cost of trading 10-year UST futures.

This move is causing the clearing battle to come front and center for the first time since the implementation of Dodd-Frank a decade ago. To succeed, especially in a space with a strong incumbent, any new exchange must build an ecosystem of banks, market makers and clearing brokers to ensure that clients can access liquidity and seamlessly process and margin trades. FMX’s 10 current partners include the largest banks and market makers, and 7 of the 8 largest futures commission merchants (FCMs). Given CME’s current market share as sole incumbent in U.S. rate futures, differentiation in margin efficiency becomes paramount for FMX or anyone hoping to compete.

Interest-rate derivatives posted margin has increased by 108% since 2017, reaching $331.8 billion as of the end of 2023.1 Fragmented margin pools have meant the benefits of portfolio margining are modest, since offsets accrue more rapidly when futures and swaps collateral are combined at scale in a single pool. The CME is the primary clearer (and exchange) of U.S. rate futures and, thus, holds a majority of that margin, with no U.S. rate futures margin held at LCH prior to the FMX launch (the FMX partnership is LCH’s first foray into U.S. rate futures). LCH, on the other hand, maintains $227 billion of swaps margin outstanding compared to $37.5 billion at the CME per their Q1 2024 IOSCO disclosures.

Portfolio margining at scale between offsetting U.S. rate futures and USD (and non-USD) swaps would free up significant capital for other uses. Both sides of this equation are working to attract the other’s open interest. CME launched client clearing of USD interest-rate swaps to support clearing mandates a decade ago. They have gained traction in Latin American currencies such as BRL and MXN, but uptake has been limited for USD swaps. LCH’s SwapClear clears the majority of global interest-rate swaps as shown by 2023 volumes: A total of $1,319 trillion of OTC swap notional was cleared at SwapClear across 27 currencies; of that, $502 trillion was based in USD. This equates to roughly 98% of USD interest-rate swap volumes cleared through LCH.2 Having launched interest-rate swap clearing for dealers in 1999, their experience gained over 25 years has allowed them to maintain the pole position as well as serving end users of derivatives.

FMX, of course, has a big hill to climb to attract futures volume from the long-running incumbent. But that said, trading UST and SOFR futures on FMX and clearing those instruments through LCH could yield significant margin benefits. As described in detail below, use of this arrangement can result in up to ~80% in potential portfolio margin savings for USD swaps and futures, and up to 50% on 13 other currency swaps. This opportunity, however, is ultimately available to whoever can bring these positions under one roof.

Increasing Margin Efficiency

Not managing margin across offsetting positions is an inefficient use of capital. Portfolio margining looks at an entire portfolio of futures and interest-rate swaps held at a CCP, nets those positions where appropriate and calculates a new margin requirement, which can result in a lower obligation.

LCH SwapClear’s approximately $227 billion pool of swaps initial margin is a large base from which to offer potential portfolio margining benefits.3 The ability to net positions and offset margin within that pool (where swap positions can offset one another) already leads to realized margin savings of $102 billion,4 according to an LCH analysis as of Q1 2024. That is significant margin relief, but the opportunity for market participants is much bigger when incorporating UST and SOFR futures. Portfolio margining at scale does not mean that capital immediately becomes abundant. But it does fundamentally reduce capital costs.

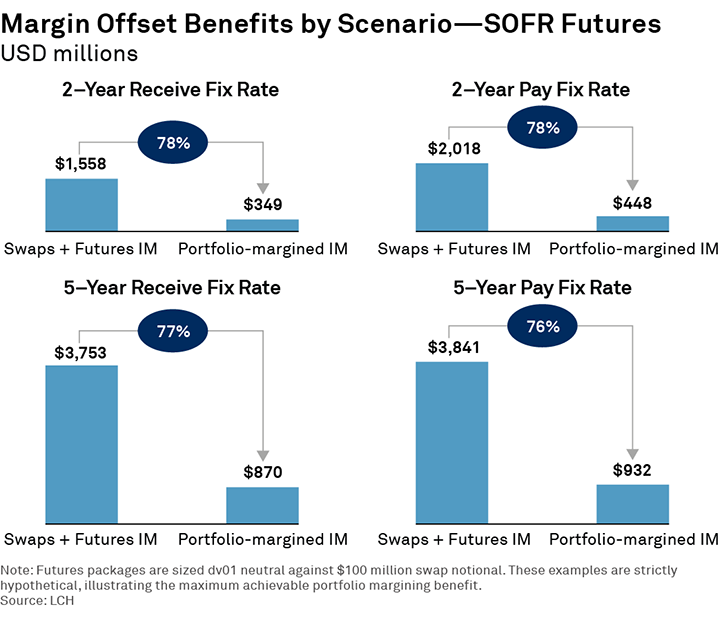

The potential industry and firm-by-firm benefits are notable. Different trading strategies implemented by different market participants will yield different results, of course. Offsets are available across a variety of strategies: For instance, the portfolio of an asset manager hedging risk and the proprietary flows of a bank with both large SOFR and UST futures positions will each benefit, though the extent will differ. The following analysis offered by LCH illustrates the maximum potential savings by scenario. While the real world is more complex, the examples provide a good base to understand the opportunity at hand.

Those that trade SOFR swaps and futures bundles can potentially realize significant margin reduction across both, up to 78% depending on the composition of the portfolio.

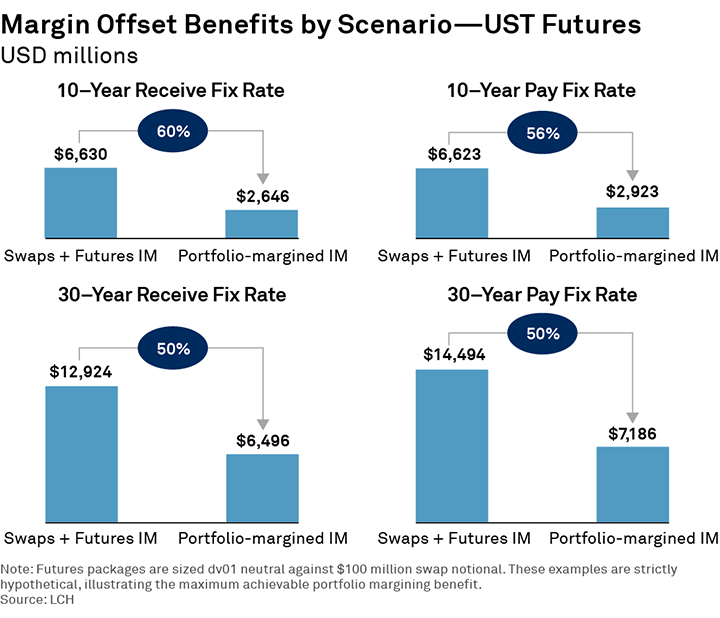

Those that trade SOFR swaps vs. UST futures will also benefit; here, the potential reduction in margin is currently in the 50–65% range across the range of UST futures contracts.

Cross-Currency Diversification Benefits

Portfolio margining is not limited to USD-denominated interest-rate derivatives. As correlations between U.S. rate futures and other swaps currencies become weaker, the offsets become lower but nonetheless are available. For instance, based on figures supplied by LCH, margin savings can reach 41% on U.S. rate futures with EUR swaps, 46% with GBP swaps, and 50% with CAD and AUD swaps. Though lower than with USD swaps, there is still a potentially material benefit to be had on 13 other currency swaps.

As the list of swaps currencies expands, the strength and stability of the correlation with U.S. rate futures contracts is harder to demonstrate and, therefore, may be ineligible for such initial margin benefits, or those benefits may be limited. As an example, Latin American currencies are not currently in scope for portfolio margining at LCH, while CME—whose cleared swap pool is primarily concentrated on these currencies—allows for benefits ranging between 4–8% vs. UST futures, according to CME data.

The Mechanics of Portfolio Margining

The mechanics and math of portfolio margining differ slightly by exchange and clearinghouse, but the principles remain largely the same. Somewhat different from CME’s vertical integration between execution and clearing, futures traded on FMX are sent to LCH for clearing. Once the positions are cleared, LCH will run a daily automated process that moves futures risk to the SwapClear OTC clearing pool for those contracts that would benefit from the efficiencies of joint margining. This all takes place behind the scenes and does not require the clearing member or client to book new trades.

Once the LCH algorithm has identified futures contracts that would be more efficient to margin jointly with swaps, it then includes those contracts in the SwapClear value-at-risk-based margin calculation to determine the total margin amount across both swaps and portfolio-margined listed contracts. The calculation has some predictability because the margin model doesn’t change based on volatility or other such factors (the margin amount may change, but the model remains consistent). The lack of predictability in margin calls has often been a source of angst for the industry, leading to unforeseen cash crunches and forced sales of assets. The greater the ability to predict a call, the greater the ability to fulfill the call with minimum impact.

Reducing margin obligations post-trade is beneficial; knowing the optimal path to maximize potential offsets before you trade will help achieve those benefits. Large entities could have a substantial number of positions spread across multiple clearing members. Regardless of the instrument type, derivatives traders therefore seek to know the margin implications of a new trade before they decide on the trade path, so they can act accordingly. Embedding tools such as LCH’s Rates Margin Calculator or CME’s Margin Calculator can help evaluate potential margin benefits through what-if analyses for incremental trades, including across swaps and futures. Reviewed pre-trade, this helps control margin costs. Approaching the margin issue from a pre-trade, trade, and post-trade perspective will provide the greatest benefits.

Conclusion

Market participants are concerned with the cost of capital, and netting and margin optimization is a key tool to alleviate that pain. USD swaps and USD interest-rate futures have been cleared separately for as long as clearing for those products has existed. Competition between exchanges and clearinghouses is good for the industry, as it encourages innovation and keeps prices low. But the current bifurcation of these two markets is requiring the industry to post tens of billions more in margin than the risk models indicate is needed.

Competition and choice are critical in financial services. But the launch of FMX and its partnership with LCH should lead market participants to refocus their efforts on margin efficiency in hopes of freeing ever-valuable capital to where it is most needed.

Stephen Bruel is a Senior Analyst on the Market Structure & Technology team covering topics including ESG, derivatives and FX.

1ISDA Margin Survey Year-End 2023

22023 CCP Volumes and Share in IRD | (clarusft.com)

3Using data provided to us by LCH, even once exclusions are taken into account, over 90% of that pool may benefit from portfolio margining depending upon trading behavior. Examples of exclusions are Inflation risk, or those swaps currencies with a lower correlation with Listed Rates futures contracts.

4$102bn saving is an aggregated service level number; this is how much more margin LCH SwapClear would have called without netting benefits.

Methodology

This report is based on an analysis conducted by Coalition Greenwich utilizing industry data on margin pools and interviews with market participants in the U.S. and U.K. to help determine the potential offsets enabled by this new FMX/LCH partnership. The report also utilizes data from Greenwich MarketView and data from U.S. and U.K.-based clearinghouses. The analysis examined scenarios involving trading strategies with different maturities and directions to highlight how those changes impact potential margin savings.