U.S. Treasury clearing: A new timeline and uncertain trajectory

Share

Share

Executive Summary

Despite the longer timeline, many unanswered technology, legal and market structure questions remain. In this report, Crisil Coalition Greenwich uses both quantitative and qualitative interviews to better understand upcoming changes in the U.S. Treasury market. In particular, the nuances of the done-away model are detailed as well as a shift to a single to a multi-CCA structure. Several open advocacy points concerning market participants are also explored.

Methodology

In January and February 2025, Crisil Coalition Greenwich conducted qualitative interviews with 10 senior experts at buy-side and sell-side firms based in the United States, U.K./Europe and Asia.

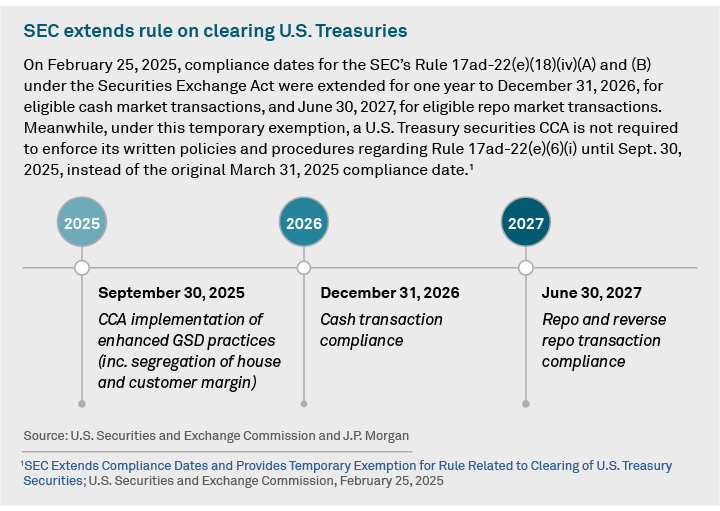

Earlier this year, the U.S. Securities and Exchange Commission (SEC) delayed implementation of its central clearing mandate of U.S. Treasury securities. The mandate will require the majority of secondary market U.S. Treasury transactions—both cash and repo—to be cleared through a covered clearing agency (CCA). Despite the longer implementation timeline, many unanswered technology, legal and market structure questions remain.

This research combines the results of quantitative and qualitative interviews to better understand market participants’ expectations for the U.S. Treasury clearing mandate. An assessment of buy-side and sell-side professionals’ views, as well as in-depth insights from senior market experts, describe the potential impact of the clearing mandate over time and what challenges still remain.

A new timeline

The new U.S. Treasury clearing rules are expected to enhance market transparency while reducing counterparty risks. Put simply, the rules and temporary exemption and timeline changes direct CCAs clearing Treasuries to establish and maintain written rules concerning practices that require all direct participants to submit cash and repo transactions for central clearing. As a result, the intermediation capacity of dealers is expected to grow.

CCAs are also tasked with monitoring activity and deciding what steps should be taken in the event there is a failure to submit trades for clearing. Further, procedures designed to calculate and collect margin on proprietary positions of direct participants also fall to the CCAs, and margin due from trades between direct and indirect participants must be separated. (This refers to Rule 17ad-22(e)(6)(i), or the so-called separation of house and customer margin).

While the timeline for implementation of the Rules has lengthened, several clarification points remain, which will ultimately shape how the Rules unfold over the next 12 months.

The “done-away” business model

One of the most salient points discussed during our interviews with industry professionals focused on the new concept of “done-away” repo business. Presently, the industry supports both done-with and done-away business models for cash trades. The Fixed Income Clearing Corporation (FICC)2 has long supported the done-with model. In the context of U.S. Treasury markets, “done with” refers to the practice of clearing trades through the same dealer that executed them, while “done away” allows market participants to use different clearing brokers for execution.

Clearing is no longer an option for selective trades where a dealer stands to gain some netting benefits to offset costs. Instead, under the new mandate, everyone must clear every repo trade. This dynamic brings with it some major challenges. For instance, each client would need a clearing arrangement with every counterparty, which is legally cumbersome. Additionally, dealers will be required to post margin for all clients. As a result, professionals at buy-side firms are expressing a preference to execute with one dealer and clear with another. Whether activity is “done with” or “done away,” the executing broker would still be eligible for balance sheet netting, as long as it has other repo activity in FICC—even if it is not the clearer. In a multi-CCA environment, netting benefits may be less efficient.

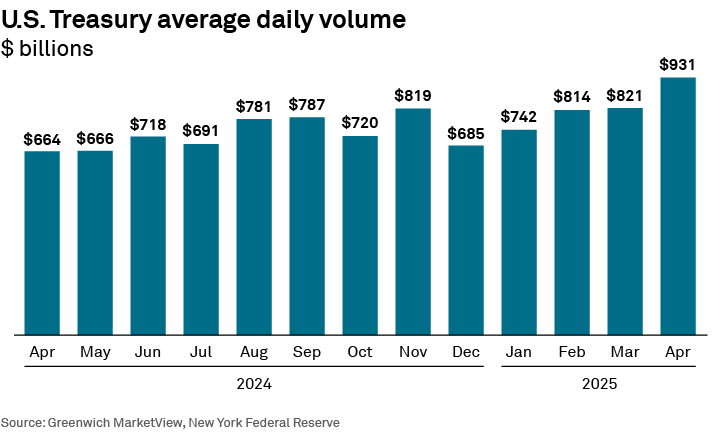

Different approaches to support done-away business are starting to emerge as a result of these frictions. Existing clearing members of FICC are currently executing done-away cash trades using the current infrastructure. In March 2025, FICC launched its enhanced Agent Clearing Service (ACS) model, which has similar characteristics to market practices supporting derivatives and swaps. Since the implementation of the enhanced service, Treasury cash activity in FICC’s Government Securities Division (GSD) has averaged around $200 billion per day, peaking on April 9 above $350 billion, when U.S. Treasury volumes reached a new one-day record. FICC successfully processed a total of $11.4 trillion in transactions at that time.

While DTCC’s ACS offers a done-away model for cash trades, the done-away structure is a new concept that doesn’t exist in the repo market today. Repo is traditionally a principal business. The idea of doing repo on a done-away basis came from the U.S. Treasury clearing requirement, even though it was available in sponsored service for years. Managers at buy-side firms are particularly focused on what new workflows are necessary as they consider optimizing margin within the cleared structure by reducing intermediaries. However, many valid concerns linger about how this will all work out. The majority of participants we spoke with compare the prescriptive nature of Dodd-Frank to the opaque guidelines of the new proposal—and stress that this divergence from clearly laid-out rules creates roadblocks along the path to compliance.

It also remains unclear how many dealers will decide to offer done-away clearing services to clients. History has shown that the largest clearing firms dominate the business regardless of product. While professionals at buy-side firms prefer choice and always need competition, it is inefficient to clear with too many clearing brokers. Further, it is not yet obvious that done-away repo clearing will generate the necessary return on capital for the largest dealers. It’s not unreasonable to think that Bank of New York, State Street and other similar banks will continue to act as the largest clearing firms in the market under the new mandatory clearing regime, with many global investment banks remaining focused on trade execution.

Competition for clearing

Despite planned initiatives being discussed for done-away business, industry professionals are quick to point out differences between derivatives and cash products that could impact clearing arrangements. For instance, swaps are contracts rather than assets and do not include a principal exchange, like repo and cash. They also don’t have the same balance sheet impact. Most notably, in contrast to the over-the-counter swaps market where trades are frequently executed on a fully disclosed basis, a substantial portion of U.S. Treasury cash and repo transactions has, for decades, been executed anonymously on interdealer broker platforms.

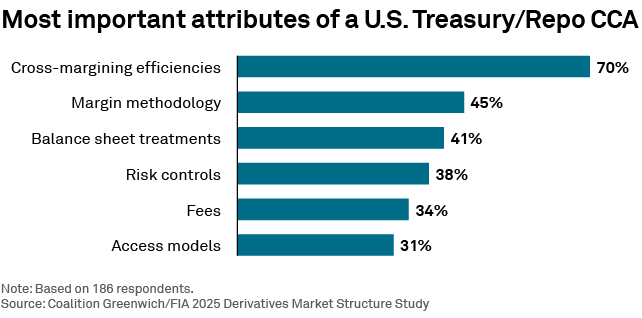

In a recent study, we found the vast majority of participants feel cross-margining is the top benefit of clearing. On a related note, margin methodology, balance sheet treatment and risk controls are also important and could potentially be a differentiator for newer CCAs. These firms may be able to capitalize on existing methodologies designed for cleared and exchange-traded markets. Finally, fees and access models are also important attributes CCAs can refine to attract new business.

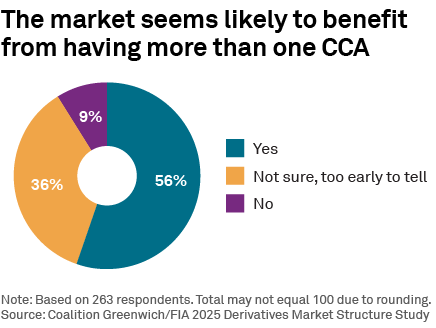

The new clearing requirements encourage new competition—a phenomenon our study participants appear to be optimistic about. The Chicago Mercantile Exchange (CME), the Intercontinental Exchange (ICE) and FICC offer or plan to offer U.S. Treasury cash and repo clearing in support of the mandate. Different approaches are being tested for clients wishing to settle trades directly with these entities, opening the door for more done-away business and a multi-CCA environment.

New beneficial relationships across CCAs are also developing. For instance, in January 2024, CME Group and FICC implemented their enhanced cross-margining arrangement, enabling capital efficiencies for clearing members that trade and clear both U.S. Treasury securities and CME Group interest-rate futures. CME Group and FICC are now working together to extend this program to end-user customers by the end of 2025, providing them access to capital efficiencies available when trading U.S. Treasury securities and CME Group interest-rate futures that have offsetting risk exposures. The changes would expand the scope and efficiency of the margin offsets that are currently available only to clearing members of CME and FICC down to end-user customers.

Eliminating bilateral agreements can open up the door for more trading. Characteristics of a swaps and futures clearing model, including the immediate novation of trades to clearing, will be the foundation of the CCA structure at the ICE and the CME. Clearing at FICC is somewhat different right now. FICC’s novation also occurs immediately upon the conditions of the novations being satisfied. However, these conditions may vary depending on the nature of the activity that has been developed over decades with FICC’s clients active in the U.S. Treasury market.

No matter the arrangement, our study participants emphasize that they want to feel confident when they trade. A multiple CCA environment could result in a competitive landscape as clearing houses try to out-innovate each other. One participant described clearing as “messy,” as CCAs and counterparties must connect via APIs and other pipes, consider credit and other limits, guarantee fund deposits, and so on. Conceptually, the market likes the idea of competition, but questions arise concerning how much competition actually makes sense. Conversely, there is an argument to be made that concentrating clearing activity in one CCA benefits market participants due to cost savings, access to liquidity and greater netting efficiency.

For instance, dealers that choose to offer done-away clearing will need to connect to each clearinghouse and probably become members, participate in the default fund, as well as optimize portfolios and collateral. This creates opportunities for FCMs, but as one industry professional puts it, “Getting there is the hard part.” Other factors, including netting and reporting, may help move the needle. Technology is set to play a key role as well—to analyze and port positions seamlessly, create margin toolkits and calculate risk analytics, while providing a safe and secure environment.

Lingering advocacy points

As market participants look to tie up loose ends ahead of the go-live dates, there are several advocacy points that currently remain open.

Credit checks

First and foremost, credit checks are a cause for concern. Typically, the FCM community wants activity and credit-limit data before they become responsible for a trade. None of the infrastructure required for pre- or post-trade credit-limit checks that FCMs need to operate exist today in repo. While there is precedent for solving this problem in the swaps market, questions remain as to how problems might surface and how such an infrastructure will evolve to remediate them.

For instance, more than 50% of repo trading is done by voice today (even if it is booked electronically). A precarious scenario could arise should a counterparty’s clearing agent lack enough credit, particularly if this was discovered after a voice trade was executed. Which party is on the hook to ensure the trade will perform and is cleared? Is a transaction void if there is a failure or does it live on in some capacity? Additionally, no one is certain who will actually run the credit checks or how quickly they will need to happen. Industry professionals agree this issue needs to be ironed out immediately or there’s a chance that done-away repo activity may be hindered. While the technology to perform these checks does exist, the industry still needs to agree on the best path forward.

Mixed tri-party baskets

Another pain point caused by opacity of the rules concerns baskets of trades that are accepted via the tri-party model involving mixed CUSIPs. For instance, both U.S. Treasury bonds and agency mortgage-backed securities (MBS) are accepted today as tri-party shells get filled, e.g., with a large transaction of overnight or term funding of collateral. As lenders send cash and borrowers send securities, the shell may be made up of 99.9% agency bonds. If a single U.S. Treasury bond falls into the shell, the entire transaction is in scope, effectively forcing MBS into clearing, despite not being covered in the mandate. Significant amounts of agency MBS, debentures and other Fed-eligible securities clear FICC; however, this point is creating a lot of uncertainty.

Inter-affiliate transactions

Market participants are seeking relief in some of the “unpopular” aspects of the mandate. The inter-affiliate carve-out is one example. In this case, eligible FICC members (e.g., banks, broker-dealers or FCMs) may take advantage of the exemption from the Treasury repo clearing requirement. However, if the exemption is used, then the affiliate’s Treasury repo needs to clear (as if it were a FICC member)—which is causing some head-scratching.

Inter-affiliate trades are purposed for liquidity management. Most in the industry feel they shouldn’t be brought into scope, given what they are used for. In this sense, hearing the rule “isn’t fit for purpose” is a common gripe. One industry professional we spoke with expressed concern as firms struggle with the SEC to establish a better understanding of the inter-affiliate carve out. (Some industry experts are suggesting the use of volume thresholds may be helpful in determining whether clearing is mandated or not.) All told, industry sentiment is clear: Moving U.S. Treasuries from one entity to another for inventory management to facilitate settlement should not fall in scope. There is a continued push to either change this language or scrap it.

International reach

The final clearing rules determine clearing requirements based primarily on the market participant type (e.g., securities dealer, hedge fund) and registration status with a CCA. As written, it appears they do not focus solely on U.S.-based firms. If no further changes or clarifications are put forward by the SEC, the rules will bring into scope a long list of internationally based firms operating in the U.S. Treasury market in the U.S. The swaps market again sets a precedent here, having defined a U.S. person to determine who was required to follow CFTC rules. There is no such distinction in this case, however, suggesting a more global mandate.

Conclusion

Changes to the U.S. Treasury and repo markets are imminent. Clearing is going to happen. Although timelines have been altered to allow the industry to prepare, several material questions remain that will influence the processes underscored by the mandate.

Defining the mechanisms and rules for done-away repo trading is critical to a successful implementation of these new rules. While an agency model has existed for cash transactions for some time, this is a brand-new initiative impacting repo markets. Lingering advocacy points have surfaced concerning exactly how done-away business will evolve and how it will be best supported by technology improvements, ensuring timely credit checks, risk management and settlement.

A new competitive landscape is also on the horizon. CME and ICE are expected to join FICC to offer clearing of cash and repo transactions, providing market participants with equal doses of choice and complexity. As this happens, market participants will closely watch developments in netting and margin—a top priority, according to our findings—to ensure efficiencies and optimized portfolios. All told, there is still a lot of work to be done.

Audrey Costabile advises on market structure and technology globally.

2FICC is a regulatory clearing agency that facilitates the settlement, confirmation, and delivery of fixed-income assets in the U.S. FICC is a subsidiary of the Depository Trust & Clearing Corporation (DTCC)

Methodology

In January and February 2025, Crisil Coalition Greenwich conducted qualitative interviews with 10 senior experts at buy-side and sell-side firms based in the U.S., U.K./Europe and Asia. The focus of these interviews uncovered opinions and details surrounding the legal, structural and uncertain elements of U.S. Treasury and repo clearing activities.