Operational Risk Consultancy

Crisil Risk Solutions reviews, recommends and designs operational risk management frameworks.

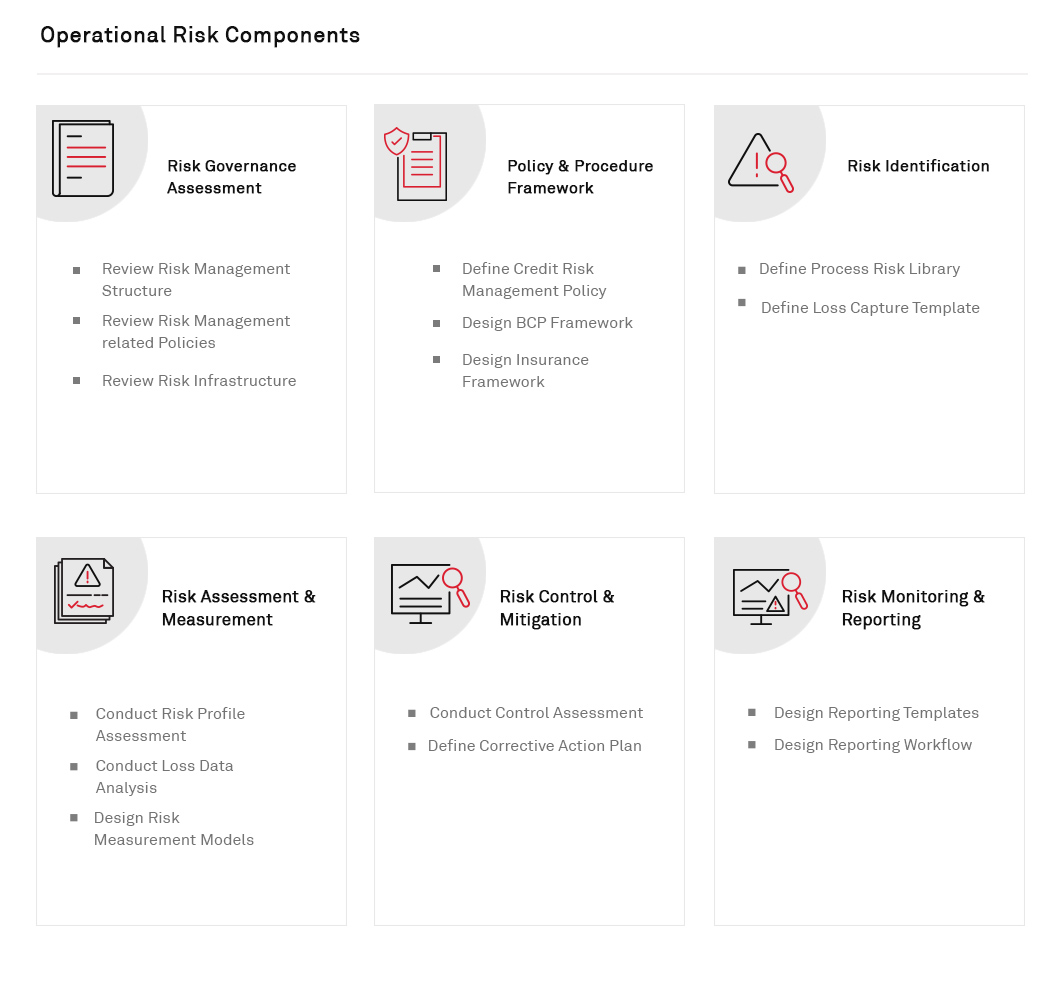

Gap Analysis

- Diagnostic review of operational risk management practices as compared to industry best practices and regulatory guidelines.

Policy & Procedure

- Analysis of key business processes, development of workflow charts, identification/grading of possible operational risk areas

- Assess and mitigate operational risk

- Design control processes to assist in risk mitigation/minimisation

Risk Control Self-Assessment (RCSA)

- Design process-risk-control library to assist risk control self-assessment (RCSA)

- Design framework and template for RCSA

Key Risk Indicators (KRI)

- Design process flow and library for key risk indicators (KRI)

- Design KRI monitoring framework

Loss Data Management (LDM)

- Design framework to measure operational risk

- Design processes to analyse operational loss databases

- Design framework for loss data management

Model Validation

- Validate bank's internal models, etc to ensure compliance with advanced measurement approach

Operational Risk Consulting develops value-at-risk (VaR) models for operational risk measurement. It entails:

- Loss data collection across Basel business lines and loss event categories

- Loss data modeling

- Conduct "goodness of fit" test to assess strength of distribution

- Conduct simulation analysis

- Estimate operational loss VaR

- Back-testing to assess operational loss of VaR as against actual loss

- Operational risk capital charge estimation

- Estimate unexpected loss

- Scale-up factor, based on results of RCSA and KRI

- Value-at-risk model validation process includes:

- Assessment of internal and external data (including proxy data elements) used in the model to ensure completeness

- Analysis of model assumptions

- Analysis of mathematical calculation and underlying risk factors

- Back-testing of existing data

- Testing VaR model based on hypothetical portfolios

- Validation of model vis-a-vis benchmark/industry standard

- Assessment of reporting to senior management as regards

- Assessment of internal and external data (including proxy data elements) used in the model to ensure completeness

- Analysis of model assumptions

- Analysis of mathematical calculation and underlying risk factors

- Back-testing of existing data

- Testing VaR model based on hypothetical portfolios

- Validation of model vis-a-vis benchmark/industry standard

- Assessment of reporting to senior management as regards